Income Tax Calculator FY 2024-25: Old vs New Regime Guide for Indian Taxpayers

Updated on 8 June 2026 • 18 min read • WealthSure

If you are searching for an income tax calculator fy 2024 25, you are probably trying to answer a very practical question: “How much tax do I really need to pay for income earned between 1 April 2024 and 31 March 2025?” For many Indian taxpayers, the answer is not as simple as applying one slab rate to annual income. Your final tax estimate depends on salary structure, deductions, exemptions, old or new tax regime selection, standard deduction, HRA, home loan interest, NPS, capital gains, freelance income, interest income, surcharge, health and education cess, and tax already deducted during the year.

Manual tax calculation often becomes confusing because Indian taxpayers think in monthly salary, annual CTC, tax deducted every month, investment proofs, rent receipts and refund expectations. The calculator, however, works best when you enter the correct taxable components in the correct order. A salaried employee with ₹12 lakh CTC, HRA and 80C investments may get a different answer from a freelancer with the same gross receipts. An investor with capital gains may need separate calculation for special-rate income. A high-income taxpayer may also need to check surcharge and marginal relief. This is why a calculator should be used as a planning tool, not as a blind substitute for tax review.

For FY 2024-25, the old tax regime and the new tax regime can produce very different results. The new regime is often simpler, while the old regime can still be useful for taxpayers with meaningful deductions or exemptions. The right choice depends on the actual numbers, not social media shortcuts or one-line advice. A good income tax calculator helps you estimate both options before filing your return or making year-end tax planning decisions.

At WealthSure, we see many taxpayers use a tax calculator only after TDS has already been deducted, after investment declaration windows have closed, or when they receive a refund or demand surprise during return filing. A better approach is to use the calculator early, compare regimes, check deductions, review tax credits, and then file accurately through self-service or expert-assisted tax filing where needed. If your income includes capital gains, foreign income, freelance receipts, NRI taxation, business income, stock trading, notice history or multiple employers, the calculator can show the direction, but expert review can help prevent expensive mistakes.

Important: This guide explains the logic of using an income tax calculator for FY 2024-25. Tax laws, portal utilities, forms and interpretations may change. Always cross-check the latest rules on the official Income Tax e-Filing portal and the Income Tax Department website before filing or paying tax.

What does an income tax calculator FY 2024-25 actually do?

An income tax calculator estimates the tax payable for a given financial year by applying the relevant slab rates, deductions, exemptions, rebate, cess and sometimes surcharge. For FY 2024-25, it helps you estimate liability for income earned during the year ending 31 March 2025, which generally connects to Assessment Year 2025-26 return filing.

In simple terms, the calculator takes your income and asks: what portion is taxable, which regime are you choosing, what deductions are allowed, whether any rebate applies, and whether additional cess or surcharge should be added. The result can help you plan TDS, decide whether to pay advance tax, evaluate tax-saving investments and understand whether a refund or additional tax payable may arise during ITR filing.

However, a calculator is only as reliable as the information entered into it. If you enter CTC instead of taxable salary, ignore employer contribution details, miss bank interest, forget capital gains, claim old-regime deductions under the new regime, or skip surcharge, the output may be misleading. That is why high-value tax planning combines calculator estimates with document review.

Estimate tax payable

Understand approximate tax under the chosen regime after deductions, rebate, cess and tax credits where supported.

Compare regimes

Check whether the old or new tax regime is more suitable based on actual eligible deductions and income mix.

Plan cash flow

Identify whether TDS is enough, whether advance tax may be needed, or whether self-assessment tax may arise later.

FY 2024-25 and AY 2025-26: do not confuse the two

One of the most common mistakes while using an income tax calculator is choosing the wrong year. FY 2024-25 means the financial year in which income is earned, from 1 April 2024 to 31 March 2025. AY 2025-26 means the assessment year in which that income is reported and assessed through income tax return filing.

If you use a calculator meant for a different financial year, your estimate may be wrong because slab rates, rebates, standard deduction, surcharge rules or regime provisions may differ. This matters particularly when budgets change tax rules. Always select the correct year in the calculator before comparing tax liability.

| Term | Meaning | Why it matters in a calculator |

|---|---|---|

| Financial Year 2024-25 | Income earned between 1 April 2024 and 31 March 2025 | The calculator applies the tax rules relevant to this income year. |

| Assessment Year 2025-26 | The year in which FY 2024-25 income is reported | ITR forms and filing utilities correspond to this assessment year. |

| Old tax regime | Regime allowing several deductions and exemptions subject to rules | Useful when eligible deductions materially reduce taxable income. |

| New tax regime | Default simplified regime with different slabs and fewer deductions | Useful for many taxpayers with fewer deductions or simpler salary structures. |

Before filing your return, you can also review official tax tools such as the government’s income tax calculator. For personalised tax planning, WealthSure can help you compare estimates with actual documents through personal tax planning.

Inputs required before using an income tax calculator for FY 2024-25

Tax calculation is not just about annual income. The calculator needs clean inputs. If you enter incomplete or inaccurate numbers, the final estimate may look neat but still be wrong. Collect the following details before you start.

1. Salary and employment income

Use taxable salary details, not just CTC. CTC may include employer PF contribution, gratuity cost, insurance benefits, variable pay assumptions and non-taxable components. Your taxable salary should be cross-checked with Form 16, payslips and employer tax statements.

2. Income from other sources

Many taxpayers forget savings bank interest, fixed deposit interest, recurring deposit interest, dividend income or family pension. These items may appear small monthly but can affect taxable income and the old-vs-new regime comparison.

3. House property details

If you receive rent or claim home loan interest, enter house property income correctly. Old regime treatment can differ from the new regime, and loss set-off rules should not be casually assumed.

4. Capital gains and market income

If you sold shares, mutual funds, property, bonds, ESOPs or foreign assets, a simple salary calculator may not be sufficient. Capital gains can have special tax rates, indexation or reporting schedules depending on the asset and period. WealthSure’s capital gains tax support can help when the calculation is not straightforward.

5. Deductions and exemptions

For the old regime, collect proofs for Section 80C investments, 80D health insurance, HRA, home loan interest, NPS and other eligible deductions. For the new regime, do not assume every old-regime deduction will be allowed. A well-designed calculator keeps regime-specific inputs separate.

6. Tax already paid

Keep TDS, TCS, advance tax and self-assessment tax details ready. These do not reduce total tax liability directly; they reduce the balance payable after tax is computed. Before filing, match tax credits with Form 26AS and portal records on the official e-filing portal.

Calculator caution: Do not use the calculator result as a refund promise. Refunds depend on final return filing, tax credit matching, verification, processing by the Income Tax Department and absence of unresolved mismatch.

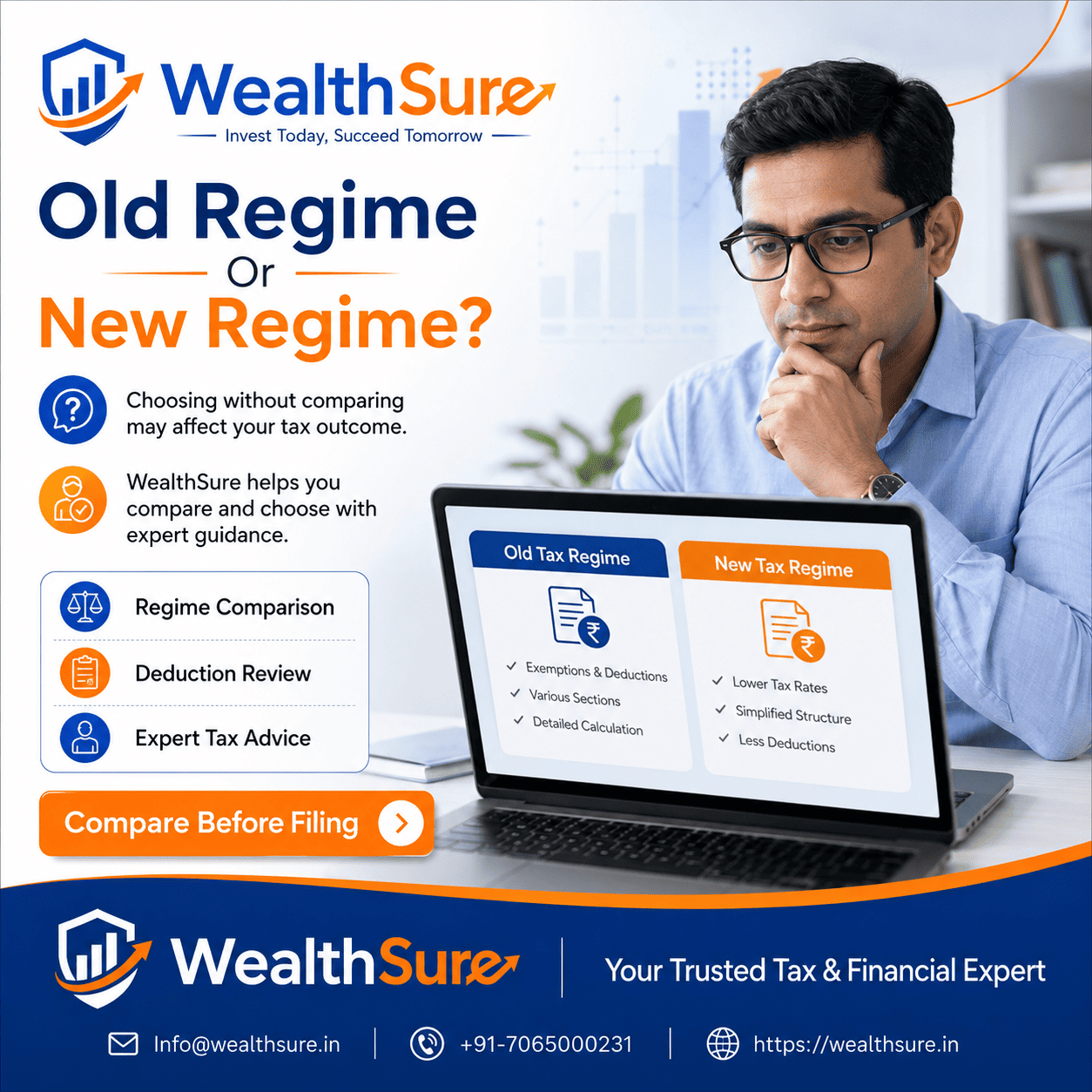

Old tax regime vs new tax regime for FY 2024-25

The main reason people search for an income tax calculator fy 2024 25 is to compare the old and new tax regimes. The old regime may benefit taxpayers with eligible deductions and exemptions. The new regime may benefit taxpayers who have fewer deductions or prefer simpler calculation. Neither is universally better.

For FY 2024-25, taxpayers should compare both regimes using actual eligible numbers. A salaried employee with high HRA and 80C investments may still find the old regime useful. Another employee with low deductions may pay less under the new regime. A freelancer may need to consider professional expenses and presumptive taxation. A senior citizen may need age-based slab and interest income considerations.

| Comparison point | Old tax regime | New tax regime | Calculator note |

|---|---|---|---|

| Deductions | Allows many eligible deductions such as 80C, 80D and certain other benefits. | Allows fewer deductions, subject to applicable law. | Enter deductions separately for each regime. |

| Exemptions | HRA, LTA and other eligible exemptions may be relevant. | Many exemptions may not be available. | Do not carry old-regime exemptions into new-regime calculation. |

| Default position | May need to be chosen where permitted. | Generally the default regime for many taxpayers. | Check whether regime switching rules apply to you. |

| Best suited for | Taxpayers with meaningful documented deductions. | Taxpayers with simple income and fewer deductions. | Use actual numbers rather than assumptions. |

| Planning style | Documentation-heavy and deduction-focused. | Simpler but less deduction-led. | Calculator should not replace proof collection. |

The Income Tax Department provides information about tax rates and official utilities on its tax rates page. You should always verify the latest rates before making a final filing decision, especially when using third-party tools.

Not sure which regime is better? WealthSure can review your income, deductions, salary structure and tax credits before filing.

Explore tax optimizer supportHow the FY 2024-25 income tax calculation usually flows

A tax calculator should not jump directly from gross income to tax payable. A practical calculation follows a sequence. Understanding this sequence helps you identify whether the calculator is asking the right questions.

Step 1: Add income under each head

Start with salary, house property, business or professional income, capital gains and income from other sources. This is important because different types of income may have different tax treatment.

Step 2: Apply eligible exemptions

In the old regime, eligible salary exemptions such as HRA may reduce taxable salary. In the new regime, exemptions are restricted. If the calculator does not ask your regime before applying exemptions, be careful.

Step 3: Reduce eligible deductions

Deductions such as 80C, 80D, eligible NPS contributions and others may reduce taxable income in the old regime. Under the new regime, allowed deductions differ. A calculator should not apply the same deduction list to both regimes without distinction.

Step 4: Apply tax slabs and special rates

After arriving at taxable income, the calculator applies slab rates. Some income, such as certain capital gains, may be taxed at special rates instead of normal slab rates. This is where basic calculators can become less reliable for investors.

Step 5: Apply rebate, surcharge and cess

Eligible resident individuals may get rebate subject to conditions. High-income taxpayers may need surcharge. Health and education cess is added to tax as applicable. Forgetting this step can create underestimation.

Step 6: Adjust tax already paid

After computing total tax liability, subtract TDS, TCS, advance tax and self-assessment tax already paid. This shows whether additional tax may be payable or whether a refund claim may arise after filing and processing.

Practical examples: how taxpayers use an income tax calculator FY 2024-25

Examples make calculator logic easier to understand. The numbers below are simplified for learning. Actual tax may differ based on salary components, deductions, special income, state-specific professional tax, employer reporting and changes in law.

Example 1: Salaried employee comparing old and new regime

Situation: Rohan earns a taxable salary of ₹10,50,000 for FY 2024-25. He has Section 80C investments of ₹1,50,000, health insurance premium of ₹25,000 and pays rent eligible for HRA exemption under the old regime.

Common confusion: He assumes the new regime must be better because it has simplified slabs. However, he does not first quantify his old-regime exemptions and deductions.

Correct approach: Rohan should enter salary, HRA exemption, 80C, 80D and any other eligible deductions into the old-regime calculation. Then he should separately calculate tax under the new regime without forcing old-regime deductions. The better regime is the one with lower final tax after legitimate deductions, rebate rules, cess and tax credits.

How expert guidance helps: WealthSure can review his salary structure, rent proof, deductions and Form 16 before ITR filing. This reduces the risk of choosing the wrong regime or claiming unsupported deductions.

Example 2: Freelancer estimating advance tax and ITR impact

Situation: Meera is a freelance designer with ₹14 lakh gross receipts, TDS deducted by clients and business expenses for software, internet, coworking and professional tools.

Common confusion: She uses a simple salary calculator and enters gross receipts as salary income. The calculator output does not consider professional expenses, presumptive taxation options, advance tax or business/profession reporting.

Correct approach: Meera should identify whether she is using presumptive taxation or actual profit calculation. She should account for TDS, eligible expenses, GST records if applicable and advance tax obligations. A generic income tax calculator may only provide an approximate direction.

How expert guidance helps: WealthSure’s business and professional ITR filing support can help her classify income correctly, review deductions and avoid underpayment or mismatch issues.

Example 3: Investor with salary plus capital gains

Situation: Arjun earns salary income and also sold equity mutual funds during FY 2024-25. His broker statement shows short-term and long-term capital gains.

Common confusion: He enters only salary in the calculator and assumes TDS from salary covers his full tax liability. He forgets that capital gains may need separate reporting and may not be fully covered by employer TDS.

Correct approach: Arjun should use a calculator that allows capital gains inputs or separately calculate capital gains tax based on asset type, holding period and applicable rules. He should also compare AIS and broker statements before filing.

How expert guidance helps: WealthSure can help with ITR filing for salaried taxpayers with capital gains and review whether additional tax is payable before filing.

Example 4: NRI with Indian income

Situation: Kavita lives outside India but has Indian bank interest, rent from a property in India and TDS deducted during the year.

Common confusion: She uses a calculator meant for resident salaried individuals and ignores residential status. This can produce an inaccurate estimate and incomplete reporting.

Correct approach: She should first determine residential status and then calculate tax on income taxable in India, considering TDS and applicable reporting. If DTAA relief is relevant, she should not assume the calculator automatically handles it.

How expert guidance helps: WealthSure’s NRI tax filing service can help review residential status, Indian income, tax credits and disclosure requirements.

Common mistakes while using an income tax calculator for FY 2024-25

A calculator can simplify tax planning, but it cannot protect you from wrong inputs. Here are mistakes taxpayers should avoid.

- Using CTC as taxable income: CTC is not always taxable salary. Use taxable salary after checking salary slips and Form 16.

- Selecting the wrong year: FY 2024-25 calculations should not be mixed with FY 2025-26 or later rules.

- Ignoring non-salary income: Interest, dividends, rent and capital gains can change tax liability.

- Claiming deductions in the wrong regime: Many old-regime deductions may not apply in the new regime.

- Skipping cess and surcharge: Final tax is not just slab tax.

- Assuming TDS equals final tax: TDS is tax paid, not total tax payable.

- Forgetting advance tax: Freelancers, investors and taxpayers with large non-salary income may need to plan advance tax.

- Not matching AIS and Form 26AS: Calculator estimates should be reconciled with official records before ITR filing.

- Assuming refund is guaranteed: Refunds depend on correct filing, verification and processing.

Planning tip: Use an income tax calculator at least three times: at the start of the year for planning, mid-year after salary or income changes, and before ITR filing to compare with final documents.

Income tax calculator checklist for FY 2024-25

Use this checklist before relying on any tax estimate.

| Checklist item | Why it matters | Action before filing |

|---|---|---|

| Correct financial year selected | Prevents using wrong slab and rebate assumptions. | Select FY 2024-25 / AY 2025-26 where applicable. |

| Salary entered correctly | CTC and taxable salary are not the same. | Use Form 16, payslips and employer computation. |

| All income sources included | Missing income can lead to mismatch or demand. | Add interest, dividend, rent, capital gains and freelance receipts. |

| Regime-specific deductions checked | Wrong deductions can distort comparison. | Separate old-regime and new-regime entries. |

| Tax credits matched | Refund or payable amount depends on TDS and tax paid. | Review Form 26AS, AIS and challans. |

| Cess and surcharge included | Final payable tax may be higher than slab tax. | Check full computation, especially for high income. |

| Return verification planned | Filing is incomplete without verification. | Complete e-verification within the applicable timeline. |

When should you use expert help instead of relying only on a calculator?

Self-service calculators are useful for straightforward planning. They are especially helpful for salaried taxpayers with simple income and clean deductions. But some cases require more than a calculator because the issue is not just arithmetic; it is classification, documentation and compliance.

Consider expert help if you have income from multiple employers, capital gains, F&O trading, freelance or professional receipts, foreign income, NRI status, house property loss, high-value transactions, notice history, large refund claims or confusion about old versus new regime. You should also take support if the calculator result differs sharply from Form 16 or the income tax portal records.

WealthSure offers ask a tax expert support, advance tax calculation support, investment-linked tax planning and revised or updated return filing for taxpayers who need more personalised review.

Use the calculator, then file with confidence. WealthSure can help you compare regimes, validate deductions, match tax credits and complete Income Tax Return filing online accurately.

Start ITR filing supportDocuments to keep beside you before calculation

Tax calculators work best when they are fed with documents, not guesses. Before you calculate, keep these records ready:

- Form 16 from employer, if salaried.

- Salary slips and bonus details.

- Rent receipts and landlord PAN details where applicable.

- Home loan interest certificate.

- Section 80C investment proofs such as ELSS, PPF, life insurance premium or tuition fee records.

- Health insurance premium receipts for 80D planning.

- NPS contribution records.

- Bank interest certificates and fixed deposit interest statements.

- Capital gains statements from broker, mutual fund platform or registrar.

- Form 26AS, AIS and TIS data from the income tax portal.

- Advance tax and self-assessment tax challans.

If you want a simpler assisted flow, salaried taxpayers may use WealthSure’s upload your Form 16 option, while users with basic income may explore free income tax filing where suitable.

Using the calculator for proactive tax planning, not only ITR filing

The biggest benefit of an income tax calculator is not just knowing a payable number. It helps you make better decisions during the year. For example, if you calculate tax in April or May, you can plan salary declarations, insurance, NPS, home loan documentation and investment allocation more calmly. If you calculate in January or February, you can identify whether additional tax-saving action is still possible. If you calculate just before filing, you can verify whether your Form 16 and portal data are consistent.

Tax planning should not mean buying random products only to reduce tax. It should connect with your broader financial goals. An ELSS investment, NPS contribution, health insurance policy, home loan decision or retirement contribution should fit your risk profile, liquidity needs, time horizon and family responsibilities. The calculator shows tax impact; financial planning decides whether the action is suitable.

This is where WealthSure’s wider financial ecosystem can help. Depending on your needs, you can explore tax saving suggestions, goal-based investing support or retirement planning support. Market-linked investments carry risk, and tax benefits depend on eligibility, documentation and applicable law.

The Reserve Bank of India also promotes financial education and disciplined money management through its financial education initiatives. Tax planning works best when it is part of a wider financial plan that includes emergency funds, insurance, debt control, goal planning and investment discipline.

FAQs on income tax calculator FY 2024-25

1. What is an income tax calculator FY 2024-25?

An income tax calculator FY 2024-25 is a tool that helps Indian taxpayers estimate tax payable for income earned between 1 April 2024 and 31 March 2025. This income generally relates to Assessment Year 2025-26 for return filing. The calculator usually asks for annual income, deductions, exemptions, regime preference, tax already paid and sometimes age category or residential status. It then applies the relevant tax slab logic, rebate rules, health and education cess and surcharge where applicable.

The calculator is helpful because it converts scattered financial information into an estimated tax number. It can guide salary planning, advance tax decisions, old-vs-new regime comparison and ITR readiness. However, it is not a final assessment by the Income Tax Department. If inputs are wrong, the output will also be wrong. For example, using CTC instead of taxable salary, ignoring bank interest or entering old-regime deductions under the new regime can distort the estimate. Use it as a planning aid, then verify with documents and official portal records before filing.

2. Is FY 2024-25 the same as AY 2025-26?

No. FY 2024-25 and AY 2025-26 are connected but not the same. FY 2024-25 is the financial year in which you earn income, running from 1 April 2024 to 31 March 2025. AY 2025-26 is the assessment year in which that income is reported through your income tax return. When using an income tax calculator, you should choose the financial year for which the income was earned, not just the year in which you are filing.

This distinction matters because tax slabs, deductions, rebates and return forms can vary by year. If you accidentally use a calculator meant for a later year, the tax estimate may be inaccurate. This is especially important in years where budget changes modify new-regime slabs, standard deduction or rebate rules. Before making payment or filing decisions, confirm the correct financial year, assessment year and official tax rates on the Income Tax Department website or e-filing portal.

3. How does the calculator compare old and new tax regimes?

A good calculator compares the old and new tax regimes by first calculating taxable income separately under each regime. In the old regime, it considers eligible deductions and exemptions such as 80C, 80D, HRA, home loan interest and other permitted benefits. In the new regime, it applies the simplified slab structure and only those deductions or benefits that are permitted under the applicable rules for the year. The final comparison should include tax, rebate, cess and surcharge where applicable.

The comparison is useful because the better regime depends on facts. A salaried employee with strong HRA benefit, 80C investments, health insurance and home loan interest may find the old regime attractive. Another taxpayer with limited deductions may find the new regime more efficient. The calculator should not simply assume one regime is better. It should produce two estimates and let you evaluate the result with documentation. If the difference is small or your income is complex, expert review is safer before filing.

4. Which details should salaried employees enter in a FY 2024-25 tax calculator?

Salaried employees should enter taxable salary details rather than only CTC. CTC may include non-cash benefits, employer contributions, gratuity cost and components that are not directly taxable in the same way as monthly salary. Start with Form 16, salary slips, bonus details, allowances, perquisites, professional tax where applicable, HRA details and deductions declared to the employer. Also include income outside salary, such as bank interest, fixed deposit interest, dividend income, rent or capital gains.

For old-regime calculation, keep evidence for Section 80C, 80D, HRA, home loan interest, NPS and other eligible items. For new-regime calculation, ensure that only permitted benefits are considered. Salaried employees who changed jobs during the year should include income from both employers. If previous employer income is missed, the calculator may understate tax and the return may later show additional payable tax. WealthSure can help review Form 16, compare regimes and complete filing accurately.

5. Can freelancers and professionals rely on a simple income tax calculator?

Freelancers and professionals can use a simple income tax calculator for a broad estimate, but they should not rely on it blindly. Their tax calculation may involve gross receipts, business or professional expenses, TDS deducted by clients, presumptive taxation, GST records, advance tax and sometimes tax audit considerations. A calculator designed only for salaried employees may not correctly handle professional income and expense treatment.

For example, a consultant with ₹18 lakh receipts may need to decide whether actual expense-based reporting or presumptive taxation is suitable, subject to eligibility. The calculator also needs tax already deducted by clients and any advance tax paid. If professional income is entered as salary, the estimate may be misleading and the ITR form selection may also become incorrect. Freelancers should maintain invoices, bank statements, expense proof and TDS certificates. Expert guidance is useful when receipts are high, expenses are substantial, income is irregular or there is confusion about the correct ITR form.

6. Does the income tax calculator include Section 87A rebate?

Many income tax calculators include Section 87A rebate, but you should check how the calculator applies it. Rebate is different from deduction. A deduction reduces taxable income, while rebate reduces tax payable after tax is calculated, subject to eligibility conditions. For FY 2024-25, taxpayers commonly compare rebate impact under the old and new regimes, especially where taxable income is near the prescribed threshold.

The rebate rules depend on residential status, taxable income, selected regime and law applicable for the year. A calculator should apply rebate only where conditions are satisfied. It should not show a rebate for every taxpayer automatically. It should also not confuse rebate with refund. A refund arises only when tax paid through TDS, TCS, advance tax or self-assessment tax exceeds final tax liability and the return is processed accordingly. If your income is close to rebate thresholds, verify the calculation carefully before deciding regime or tax payment.

7. Why does my calculator estimate differ from Form 16?

Your calculator estimate may differ from Form 16 for several reasons. You may have entered CTC instead of taxable salary, missed exempt allowances, used a different tax regime, ignored previous employer income, entered different deductions, or excluded income that your employer did not consider. Form 16 reflects salary and TDS information reported by the employer, but your final ITR may also include bank interest, dividends, rent, capital gains, freelance income and other taxable items.

Another reason is timing. Employers calculate TDS based on declarations and proofs submitted during the year. If you later make investments, fail to submit proof, change jobs or earn additional income, your final tax liability can change. Calculator results may also differ if they include cess, surcharge or rebate differently. Before filing, reconcile Form 16 with AIS, Form 26AS and your own records. If the difference is material, do not ignore it. A review by a tax expert can help identify whether the calculator, Form 16 input or income reporting is incomplete.

8. Does a calculator show whether I will get a refund?

An income tax calculator can show an estimated refund direction if it allows you to enter TDS, TCS, advance tax and self-assessment tax already paid. If tax paid is higher than estimated final liability, the calculator may indicate a possible refund. However, this is not a guarantee. Refunds are subject to accurate return filing, e-verification, successful processing by the Income Tax Department, bank account validation and absence of unresolved mismatches.

Taxpayers often assume that a calculator refund estimate means the refund will definitely be credited. That is not correct. If AIS shows additional income, Form 26AS tax credit differs, bank account validation fails or the return contains reporting errors, the refund may be delayed, adjusted or questioned. Use the refund estimate as a signal, then verify tax credits and income records before filing. If the refund claim is large compared with your income and TDS pattern, expert review is advisable to reduce avoidable notice or processing issues.

9. Should I use the official Income Tax Department calculator or a fintech calculator?

The official Income Tax Department calculator is useful because it comes from a government source and can help taxpayers verify basic calculations. A fintech calculator may offer a more user-friendly experience, better explanations, regime comparison, planning prompts, deduction guidance or integration with filing support. The best approach is often to use a calculator for planning and then cross-check important assumptions with official sources and your own documents.

No calculator should replace careful review of income, deductions, exemptions, tax credits and ITR reporting. A calculator may not fully handle complex capital gains, foreign income, DTAA relief, business income, tax audit, past losses, special-rate income or notice history. WealthSure’s value is not just calculation; it is helping users interpret results, validate documents, compare regimes and file correctly. Use tools for speed, but use expert support when facts are complex or tax risk is meaningful.

10. How can WealthSure help after I calculate my FY 2024-25 tax?

After using an income tax calculator FY 2024-25, WealthSure can help you move from estimate to action. This may include reviewing your old-vs-new regime comparison, checking deduction proof, matching tax credits, identifying missing income, calculating advance tax, preparing your ITR, responding to mismatch concerns or planning investments for future years. The right support depends on your profile, such as salaried employee, freelancer, investor, NRI, professional or business owner.

For simple cases, a self-service filing route may be enough. For complex cases, expert-assisted support is safer. WealthSure can support salaried taxpayers with Form 16, investors with capital gains, freelancers with professional income, NRIs with Indian income, and taxpayers who need revised returns or notice response. The goal is not just to reduce tax mechanically, but to file accurately, plan lawfully and build better long-term financial habits. Tax savings, refunds and investment outcomes depend on eligibility, documentation, market risk and applicable law.

Conclusion: use the calculator as a planning tool, not a shortcut

An income tax calculator fy 2024 25 can save time, reduce confusion and help you compare old and new tax regimes before filing. It is especially useful when you want to understand tax payable, refund direction, TDS shortfall, advance tax requirement or the value of deductions. But the calculator is only the first step. The quality of the result depends on the quality of your inputs.

If your income is simple, your documents are clean and your tax credits match, a self-service calculator and guided filing flow may be enough. But if your case includes multiple employers, capital gains, freelance income, NRI status, business income, foreign income, high-value transactions, old notices or large refund claims, expert-assisted review can help you avoid mistakes. Proactive tax planning also connects with bigger financial goals such as insurance, emergency fund planning, investment discipline, retirement and wealth creation.

Ready to move from estimate to accurate filing? WealthSure can help you compare regimes, calculate tax, review documents and file your ITR with confidence.

Ask a WealthSure tax expertAt WealthSure, we don’t just file taxes — we simplify your financial journey and help you build long-term wealth with confidence.