Income Tax Return Adjustment WealthSure for Indian Taxpayers

Income tax return adjustment can affect your refund, tax payable, challan matching, outstanding demand response and ITR filing accuracy. This WealthSure guide explains what to check, when to correct records and when expert support may be useful.

Key Takeaways

- Income tax return adjustment means tax credits, payments, refunds or outstanding demands are matched while your ITR is filed or processed.

- A refund may be reduced if an earlier outstanding demand is adjusted, but you should verify the demand year, amount and reason before accepting it.

- Wrong assessment year, incorrect challan category and missing tax credit are common reasons for ITR adjustment confusion.

- Form 26AS, AIS, TIS, challan receipts and the ITR intimation should be checked together before deciding the next step.

- Some cases need a revised return, some need rectification and some need demand response; the correct route depends on the stage and issue.

- Self-service may be enough for simple matching issues, but expert support is safer for older demands, capital gains, NRI income or large adjustments.

- WealthSure can help with review, filing, correction and compliance support without promising guaranteed refunds or outcomes.

What This Page Covers

- What income tax return adjustment means for Indian taxpayers.

- Why refund adjustment, outstanding demand and challan mismatch happen.

- How to check Form 26AS, AIS, TIS, challan details and tax payment history.

- How assessment year and financial year selection affects tax credit matching.

- When to use revised return, rectification request or demand response.

- Practical examples for salaried employees, freelancers, investors, NRIs and business owners.

- When WealthSure’s income tax experts can help with filing and compliance support.

Income tax return adjustment WealthSure is usually searched by taxpayers who have filed or are preparing to file an income tax return and suddenly see a mismatch, reduced refund, outstanding demand, tax credit difference, challan issue or adjustment message on the Income Tax e-Filing portal. The problem is practical: you may have paid tax, your employer may have deducted TDS, your broker may have reported capital gains, or your refund may be expected, but the final ITR computation or department intimation shows something different.

For AY 2026-27 and other assessment years, this confusion often starts with a simple question: “Why is my income tax return showing adjustment?” In many cases, the answer is not one single mistake. It may involve self-assessment tax adjustment, advance tax credit, TDS mismatch, AIS and Form 26AS difference, an old outstanding demand, a refund adjusted against earlier dues, or a challan paid under the wrong assessment year. Because the tax portal, bank payment systems and tax information statements work together, one incorrect entry can create a visible mismatch during filing or processing.

This guide explains income tax return adjustment in plain language for Indian taxpayers. It covers refund adjustment, outstanding demand under the income tax system, self-assessment tax and advance tax matching, challan verification, Form 26AS, AIS, TIS, payment receipts, ITR intimation and the decision between revised return, rectification request and demand response. It is written for salaried professionals, freelancers, investors, NRIs, small business owners and first-time filers who want a correct next step instead of guessing.

WealthSure’s role is to help taxpayers move from confusion to clean compliance. In simple cases, you may only need to verify records and wait for payment reflection. In complex cases involving older demands, capital gains, foreign income, NRI status, business income or multiple challans, expert-assisted review can prevent wrong filing decisions. WealthSure can support accurate ITR filing, revised or updated return review, income tax notice response and expert tax consultation where the adjustment requires careful interpretation.

Quick Answer: Income Tax Return Adjustment WealthSure

Income tax return adjustment means your tax return, tax payments, TDS/TCS credits, refund claim or outstanding demand is being matched by the tax system. The adjustment may reduce tax payable, reduce a refund, show an additional amount due, or set off one year’s refund against another year’s demand.

The first step is to compare your ITR computation with Form 26AS, AIS, TIS, challan receipts and the official intimation. Do not assume the portal is wrong or correct without checking the source of mismatch. A small assessment-year error, incorrect challan type or missing TDS credit can change the result.

If the adjustment is because of self-assessment tax or advance tax paid for the same assessment year, check whether the challan details are correctly entered and reflected. If the adjustment is because of an outstanding demand, review the demand year and reason before accepting or disputing it.

WealthSure can help you identify whether the correct next step is filing accurately, revising the return, making a rectification request, responding to demand or seeking expert review for a complex adjustment.

Methodology and Official Sources

This article is based on practical income-tax filing workflow for Indian taxpayers, especially situations where tax payments, refunds, challans, Form 26AS, AIS, TIS and income tax return processing do not match cleanly. The goal is to help readers understand the adjustment before taking action.

For actual filing, payment, demand response, rectification and refund status, taxpayers should use the official Income Tax e-Filing portal. For broader tax information, readers may refer to the Income Tax Department. Investors dealing with capital gains may also refer to SEBI for market-regulation context, and bank/payment-related context can be cross-checked through the Reserve Bank of India.

Portal screens, payment modes, processing timelines and tax rules may change by assessment year. WealthSure can assist with interpretation, document matching, filing and compliance support, but final tax treatment depends on your facts, income, tax regime, documents and applicable law.

What Is Income Tax Return Adjustment?

Income tax return adjustment is the process of matching your declared tax liability with available tax credits, payments, refunds or outstanding dues. In simple words, the system checks what you owe, what you already paid, what was deducted from your income and whether any earlier demand needs attention.

An adjustment can be helpful when your self-assessment tax, advance tax or TDS is correctly matched and reduces your final tax payable. It can also be concerning when your refund is reduced or adjusted against an old demand. The same word “adjustment” can therefore mean different things depending on context.

| Adjustment type | What it usually means | What to check first |

|---|---|---|

| Tax credit adjustment | TDS, TCS, advance tax or self-assessment tax is matched against tax payable | Form 26AS, AIS, TIS and challan details |

| Refund adjustment | Refund for one year may be reduced or set off against an older demand | Demand details, intimation and response history |

| Challan adjustment | A tax payment is being linked to the return | CIN, BSR code, challan serial number, PAN and assessment year |

| Processing adjustment | Return processing has changed tax payable or refund | Intimation, computation, deductions, rebate and income matching |

| Correction adjustment | A revised return or rectification may be required | Filing date, processing status and type of error |

The important point is not to react only to the final refund or demand amount. The better approach is to understand which record caused the adjustment and whether it is factually correct.

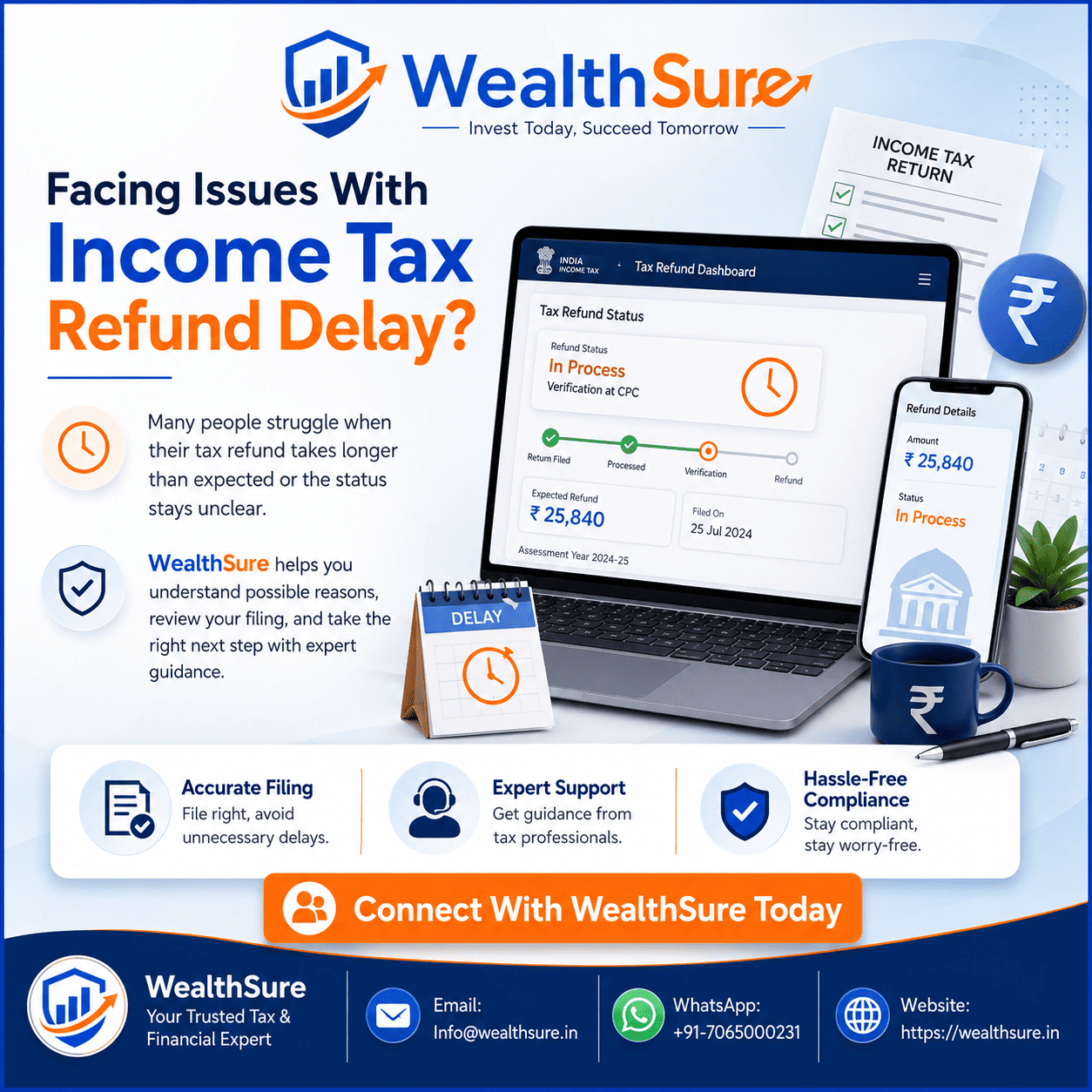

Why Refund Adjustment and Outstanding Demand Happen

Refund adjustment usually happens when the tax system finds an outstanding demand and proposes or processes a set-off against your current refund. This does not automatically mean the demand is correct, and it also does not automatically mean you should ignore it.

Many taxpayers discover this only after expecting a refund. They may see a lower refund, a notice, an intimation, or a demand entry for an earlier year. The right response depends on whether the old demand is valid, already paid, duplicated, wrongly calculated or caused by a mismatch.

| Reason | Typical taxpayer confusion | Practical next step |

|---|---|---|

| Old demand pending | “Why did my current refund reduce?” | Check demand year, section, amount and intimation |

| Tax paid but not matched | “I already paid this tax.” | Verify challan and payment reflection |

| TDS credit mismatch | “My Form 16 shows TDS but portal differs.” | Compare Form 16, Form 26AS, AIS and employer reporting |

| Wrong assessment year | “Payment made but not seen in this return.” | Check AY selected in challan |

| Incorrect income or deduction | “Portal changed my refund.” | Compare ITR computation with intimation |

When the amount is small and the reason is clear, you may be able to correct or respond yourself. When the demand is old, unexplained or linked to multiple years, a professional review is safer than clicking acceptance without understanding the effect.

Types of Tax Payments and Credits That May Be Adjusted

Different tax credits are adjusted differently, so you should identify the exact credit or payment before taking action. Taxpayers often use the word “adjustment” for every mismatch, but the compliance route changes depending on the item involved.

Advance Tax

Advance tax is tax paid during the financial year when your total tax liability crosses the applicable threshold after considering TDS and other credits. Freelancers, professionals, business owners and investors with capital gains often need to review advance tax. WealthSure’s advance tax calculation support can help taxpayers estimate liability before it becomes an ITR mismatch.

Self-Assessment Tax

Self-assessment tax is usually paid after the financial year ends but before filing the return, when final tax payable remains after TDS, TCS and advance tax credits. If the challan is not entered correctly or does not reflect properly, the return may show tax payable even though the money has been paid.

TDS and TCS Credit

TDS and TCS credits should generally reflect through Form 26AS and AIS. If employer, bank, tenant, buyer, broker or other deductor reporting is delayed or incorrect, your ITR credit may differ from expectation. A careful comparison is necessary before claiming or correcting.

Outstanding Demand

An outstanding demand is a tax amount shown as payable by the department for an earlier year. It may be valid or may need response. If ignored, it can affect refunds. If incorrectly accepted, it may close your chance to explain the mismatch properly.

Assessment Year vs Financial Year: What to Select

The assessment year is the year after the financial year, and selecting it correctly is essential for tax payment matching. For example, income earned during FY 2025-26 is generally reported in AY 2026-27.

A wrong assessment year is one of the most common reasons taxpayers search for income tax return adjustment help. If you pay self-assessment tax for the wrong AY, the return for the correct AY may still show tax payable. If you file using a payment that belongs to another AY, the return may process with a mismatch.

| Income period | Return assessment year | Common mistake |

|---|---|---|

| 1 April 2025 to 31 March 2026 | AY 2026-27 | Selecting AY 2025-26 while paying tax |

| 1 April 2024 to 31 March 2025 | AY 2025-26 | Using the current calendar year instead of assessment year |

| Old demand from earlier year | Demand year shown on portal | Assuming it belongs to the current return |

Before paying or filing, write down the income period, assessment year, payment type and PAN. This simple habit prevents many adjustment issues.

Details to Check Before Accepting an Adjustment

Before accepting, disputing or correcting an income tax adjustment, check all tax records together. Looking at only one record can mislead you because AIS, Form 26AS, TIS, challans and ITR computation serve different purposes.

- ITR computation: Check total income, deductions, tax regime, surcharge, cess, rebate, interest and final refund or payable amount.

- Form 26AS: Check TDS, TCS, advance tax, self-assessment tax and demand/refund-related entries where applicable.

- AIS and TIS: Check income information, reported transactions, TDS, interest, dividends, securities transactions and other data used for tax matching.

- Challan receipt: Check CIN, BSR code, challan serial number, payment date, amount, PAN, AY and payment category.

- Intimation: Compare income as returned, income as computed, tax credit allowed, interest and refund/demand result.

- Demand record: Check the year, section, amount, source and any prior response.

If your records are not aligned, avoid filing or responding in a hurry. A wrong response may create more follow-up work than a careful review at the start.

Step-by-Step Guide to Handle Income Tax Return Adjustment

The safest workflow is to identify the reason first, then choose the correction route. Do not jump directly to revised return, rectification or demand acceptance without understanding the mismatch.

Step 1: Download or view the relevant record

Start with the ITR computation, challan receipt, Form 26AS, AIS, TIS and the intimation or demand entry. Save copies because portal data may update later.

Step 2: Identify the adjustment type

Decide whether the issue is tax credit, refund adjustment, challan mismatch, outstanding demand, income mismatch or processing difference. This classification determines the next step.

Step 3: Match the assessment year and PAN

Check whether the challan or tax credit belongs to the same PAN and assessment year as the return. A correct amount with a wrong AY can still create mismatch.

Step 4: Compare income and tax computation

Review salary, interest, dividends, capital gains, business income, deductions, rebate and tax regime. Many adjustments come from income being reported in AIS but missed in the return.

Step 5: Decide the remedy

If the return has a mistake and the timeline permits, a revised return may help. If processing has an apparent error, rectification may be relevant. If there is a demand, a demand response may be required. If a notice is involved, use the response route mentioned in the notice.

Step 6: Keep proof and verify closure

After correction or response, keep the acknowledgement and later verify whether the refund, demand or tax credit status has changed. Do not rely only on an email or SMS; check official records.

Payment Modes and Challan Details That Affect Adjustment

Payment mode matters less than correct tax identification details, but payment records must be preserved. Whether you pay through net banking, debit card, payment gateway or authorised bank route, the challan details must be correctly available for tax credit matching.

After payment, check the challan receipt and note the challan identification information. If money is deducted but the challan is not generated, do not immediately make repeated payments without checking bank status and tax payment history. Duplicate payments can create later refund or correction work.

| Field | Why it matters | Common error |

|---|---|---|

| PAN | Links payment to taxpayer | Payment made under wrong PAN |

| Assessment year | Links payment to correct return year | AY selected as financial year |

| Payment type | Identifies advance tax, self-assessment tax or other payment | Wrong category selected |

| Amount | Matches tax payable and interest | Interest or fee not included |

| CIN/BSR/serial number | Supports verification and correction | Receipt not saved |

For taxpayers who are unsure about payment category or assessment year, a short expert review before payment is often better than a correction exercise after filing.

Common Mistakes to Avoid in Income Tax Return Adjustment

Most adjustment problems become difficult because taxpayers act before matching documents. The following mistakes are common and preventable.

| Mistake | Why it creates a problem | Better approach |

|---|---|---|

| Accepting demand without review | A wrong demand may be treated as settled or admitted | Check year, reason and supporting records |

| Ignoring refund adjustment notice | Refund may be reduced or delayed | Respond within the available portal process where applicable |

| Selecting wrong AY in challan | Tax payment may not match the return | Confirm financial year and assessment year before payment |

| Filing before challan reflection | Return may show unpaid tax or interest | Check payment history and keep receipt |

| Claiming credit not visible in records | Processing mismatch may arise | Compare Form 16, Form 26AS, AIS and TIS |

| Using revised return for every issue | Some issues require rectification or demand response | Select remedy based on processing stage |

Practical Examples: How Income Tax Return Adjustment Works

Real-life adjustment cases are easier to understand through examples. The following situations reflect common Indian taxpayer problems without assuming any guaranteed outcome.

Example 1: Salaried employee paying self-assessment tax before filing ITR

Neha receives Form 16 but also has bank interest and dividend income. Her tax calculation shows extra tax payable, so she pays self-assessment tax before filing. The mistake happens when she enters the wrong assessment year in the challan. Her return still shows tax payable because the payment is not linked to the correct AY. The correct approach is to verify challan details, payment history and Form 26AS/AIS before filing. Expert guidance can help decide whether correction or careful filing notes are needed.

Example 2: Freelancer paying advance tax to avoid interest

Aman is a freelance designer with income from Indian and overseas clients. He pays some tax during the year but does not classify records properly. While filing, his advance tax credit does not match his calculation. The mistake is relying only on bank debit entries instead of challan records. The correct approach is to compile invoices, expenses, advance tax challans and AIS data. WealthSure can support freelancers through business and professional income filing where tax credits and income reporting require careful matching.

Example 3: Investor with capital gains and refund adjustment

Rohit sells listed shares and mutual funds and expects a refund because TDS was deducted elsewhere. During processing, his refund is reduced due to an older outstanding demand. The mistake would be to assume the demand is automatically correct. The correct approach is to check the old demand, capital gains statement, tax computation and intimation. Where capital gains tax is involved, WealthSure’s capital gains tax review can help verify reporting and tax computation.

Example 4: NRI with Indian income and old demand

Priya, an NRI, has Indian rental income and TDS deducted by the tenant. She expects a refund, but the portal shows an adjustment against a previous demand. The mistake is treating the issue as only a refund delay. NRI cases may involve residential status, TDS rate, DTAA documentation and prior-year filings. The correct approach is to review residential status, Indian income, Form 26AS, AIS and demand records together. WealthSure’s NRI income tax filing support can help when cross-border facts complicate the adjustment.

Example 5: Money deducted but challan not generated

Vikram pays tax online and the money is deducted from his bank account, but he cannot immediately download the challan. The mistake is making a second payment without checking status. The correct approach is to check the official tax payment history, bank transaction status and payment confirmation before repeating payment. If the challan remains unavailable, records should be preserved and the proper correction/support route should be followed.

Income Tax Return Adjustment Checklist

Use this checklist before filing, revising, responding or accepting any adjustment. It is especially useful for AY 2026-27 ITR filing and older demand review.

- Confirm the financial year and assessment year.

- Download Form 26AS, AIS and TIS before finalising the return.

- Match Form 16, bank interest, dividend, capital gains and business income with reported data.

- Verify all challans: PAN, AY, payment type, amount, CIN, BSR code and date.

- Compare filed computation with department intimation before responding.

- Check whether the issue requires revised return, rectification, demand response or expert review.

- Keep receipts, acknowledgements, statements and portal response proof.

- Do not accept old demand or refund adjustment without understanding the reason.

- For complex income, use expert-assisted filing rather than last-minute guesswork.

How WealthSure Can Help with Income Tax Return Adjustment

WealthSure helps taxpayers understand the reason behind an income tax return adjustment and choose the right compliance action. The goal is not to promise a refund, remove every demand or guarantee a result. The goal is to help you read the records correctly, file accurately and respond with proper documentation.

WealthSure can assist with ITR filing services, revised and updated return filing, income tax notice drafting and responses, advance tax calculation and expert review through Ask Our Tax Expert. For salaried users, investors, freelancers, NRIs and business owners, the right service depends on the mismatch and the documents available.

Summary: Income Tax Return Adjustment WealthSure

Income tax return adjustment means your ITR, tax payments, TDS/TCS credits, refund or outstanding demand is being matched during filing or processing. It can be a normal tax-credit adjustment, a refund set-off against older demand, a challan mismatch, or a processing difference.

The correct first step is to compare ITR computation with Form 26AS, AIS, TIS, challan receipts, tax payment history and intimation records. Do not rely only on expected refund or bank debit entries. Check PAN, assessment year, payment category, tax amount and demand year.

For simple mismatches, self-verification may be enough. For older demands, large adjustments, capital gains, NRI income, business income or unclear notices, expert support can help decide whether to revise the return, file rectification, respond to demand or correct payment records.

FAQs on Income Tax Return Adjustment

What does income tax return adjustment mean in India?

Income tax return adjustment means a tax amount, refund, challan, TDS credit or outstanding demand is matched or set off while processing your income tax return. It may happen because you paid self-assessment tax, because advance tax or TDS is being matched with your ITR, or because the Income Tax Department proposes to adjust a refund against an earlier demand. The practical issue is that taxpayers often see a different refund or tax payable amount after processing than what they expected while filing. The right approach is to compare your ITR computation with AIS, TIS, Form 26AS, challan details and the intimation issued by the department before assuming an error.

Why was my income tax refund adjusted against an outstanding demand?

Your refund may be adjusted if the Income Tax Department records an outstanding demand from an earlier assessment year and processes your current refund against it after the applicable intimation process. This can happen because of an old mismatch, unpaid self-assessment tax, incorrect TDS credit, an earlier return processing difference or a demand that was not properly responded to. Before accepting the adjustment, check the demand year, section, amount, interest and whether the demand actually belongs to you. If the demand is incorrect, you may need to respond on the e-Filing portal and keep supporting records ready.

How can I check whether my ITR adjustment is correct?

You can check whether your ITR adjustment is correct by comparing five records: the filed ITR computation, Form 26AS, AIS, TIS, challan payment details and the income tax intimation. Look for differences in tax paid, TDS credit, advance tax, self-assessment tax, interest, late fee, rebate, deductions or capital gains. If the mismatch is due to a wrong assessment year, wrong challan category or missing credit, correction may be required before or after filing depending on the stage. If the issue is an outstanding demand, review the demand details and respond through the official portal.

Can WealthSure help with income tax return adjustment?

Yes, WealthSure can help Indian taxpayers understand income tax return adjustment, verify tax credits, review outstanding demand, identify challan or assessment-year errors and decide whether a revised return, rectification request or demand response is appropriate. WealthSure’s role is not to promise a refund or guaranteed outcome. The focus is to check documents, match official records, prepare the right response and reduce avoidable filing mistakes. Expert help is especially useful when the adjustment involves older years, capital gains, NRI income, business income, foreign income, multiple challans or a notice from the department.

What is the difference between self-assessment tax adjustment and refund adjustment?

Self-assessment tax adjustment generally means the tax you paid before filing the return is matched against your final tax liability in the ITR. Refund adjustment usually means the refund determined for one year is reduced or set off against an outstanding demand from another year. Both involve tax matching, but the direction is different. In self-assessment tax adjustment, your payment should reduce tax payable for the same assessment year. In refund adjustment, the department may use a refund to settle an earlier demand. The documents to check are also different: challan details for self-assessment tax and demand/intimation records for refund adjustment.

What should I do if my challan is not showing in Form 26AS or AIS?

If your challan is not showing in Form 26AS or AIS, first verify the CIN, BSR code, challan serial number, amount, payment date, PAN and assessment year. Sometimes there is a timing delay between payment and reflection in tax records. If the details are correct but the credit still does not appear, check the tax payment history on the official e-Filing portal and preserve the payment receipt. If the assessment year or payment type was selected incorrectly, a correction route may be needed. Do not file blindly by assuming the payment will match later; mismatched challans can create tax payable, interest or processing differences.

Which assessment year should I select for an income tax payment or adjustment?

The assessment year is the year immediately after the financial year in which income is earned. For example, income earned during financial year 2025-26 is generally assessed in AY 2026-27. A wrong assessment year is one of the most common reasons for tax credit mismatch and income tax return adjustment confusion. Before paying self-assessment tax or advance tax, confirm the income year, return year, payment category and PAN. If tax is paid under the wrong assessment year, the payment may not automatically match the return you are filing, and professional review may be required to decide the correct correction path.

Can I revise my return if tax credit or adjustment details are wrong?

A revised return may be possible if the original return was filed within the permitted timeline and the mistake relates to reporting, income, deductions, tax credit or computation. However, not every adjustment issue is solved by revising the return. If the return was processed and the error is in processing, a rectification request may be more suitable. If the issue is an outstanding demand, you may need to respond to the demand instead. The right route depends on the assessment year, filing status, processing stage, nature of mismatch and documents available.

What records should I keep for an income tax return adjustment case?

Keep the filed ITR acknowledgement, computation, Form 16, Form 26AS, AIS, TIS, challan receipts, bank statements showing payment, capital gains statements, demand notices, intimation orders and any portal response acknowledgements. These records help prove whether a tax credit, refund claim or outstanding demand is correct. For salaried taxpayers, Form 16 and AIS comparison is important. For freelancers and investors, payment receipts, broker statements and advance tax records matter. For NRIs, residential status and Indian income records are also useful. Clean documentation makes it easier to respond accurately and avoid repeated portal mismatches.

When should I ask an expert before accepting an income tax adjustment?

You should ask an expert before accepting an income tax adjustment when the amount is significant, the demand belongs to an older year, the reason is unclear, the challan does not match, the issue involves capital gains or foreign income, or you are unsure whether to revise, rectify or respond to demand. Self-service may be enough for a simple visible challan delay or a small calculation difference that you can clearly verify. Expert support is safer when the adjustment can affect refund, interest, penalties, future compliance history or multiple years of tax records. WealthSure can review documents and guide the next step without hard-selling unnecessary services.

Conclusion: Handle Income Tax Return Adjustment with Records, Not Guesswork

Income tax return adjustment matters because it can change your refund, tax payable, demand status and compliance history. The main problem is usually not the word “adjustment” itself, but the reason behind it: tax credit mismatch, wrong assessment year, challan error, outstanding demand, processing difference or incomplete income reporting.

Self-service may be enough when the mismatch is small, recent and clearly supported by documents. Expert-assisted support becomes safer when the adjustment involves older years, a large refund, unexplained demand, capital gains, business income, NRI taxation, foreign income, multiple challans or a notice response. Correct filing, proper verification and timely response are more useful than last-minute assumptions.

At WealthSure, we don’t just file taxes — we simplify your financial journey and help you build long-term wealth with confidence.