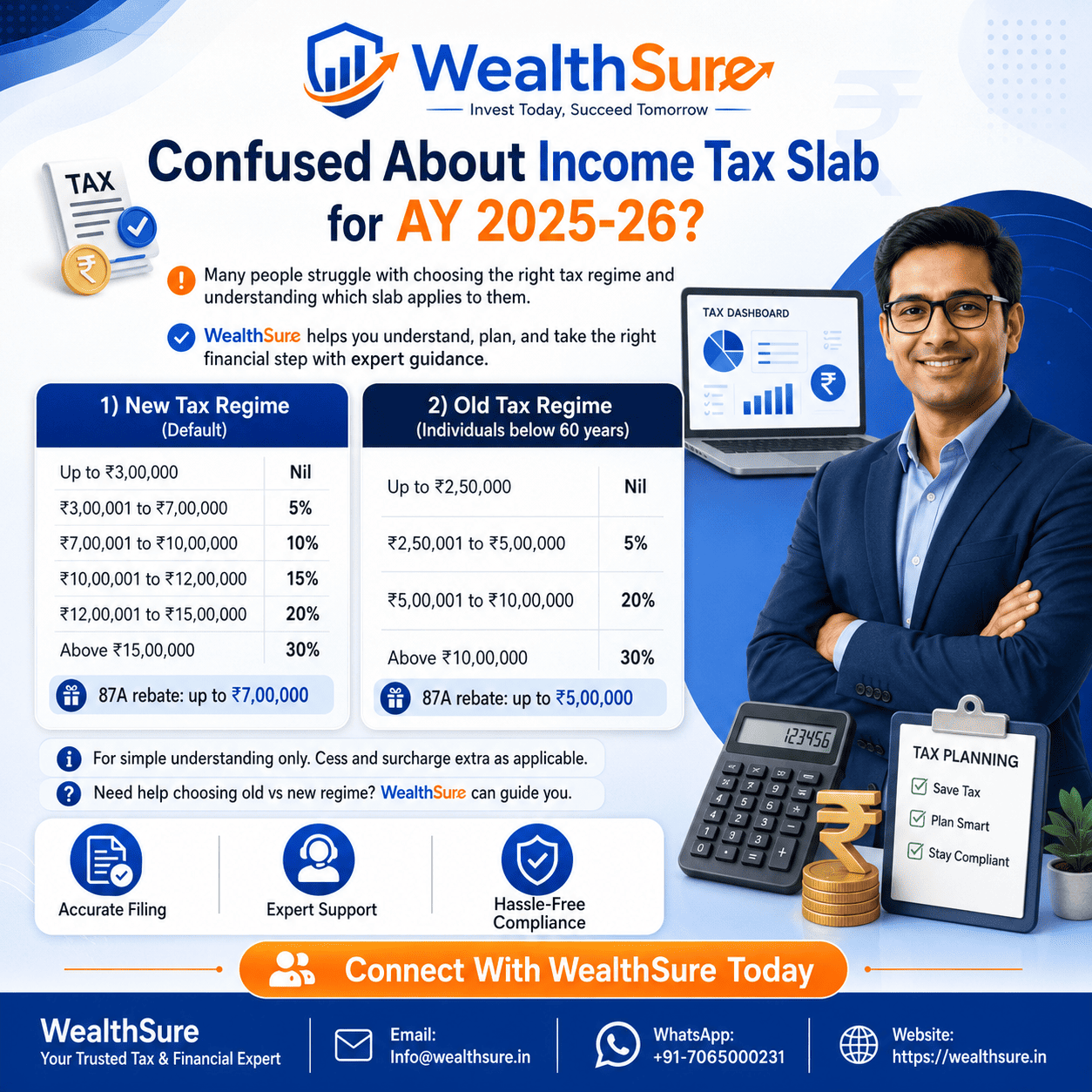

WealthSure Income Tax Return Last Date: ITR Due Date, Late Filing and Expert Help

The WealthSure income tax return last date guide explains the ITR filing deadline, belated return options, late filing fee, document readiness, tax payment checks and verification steps Indian taxpayers should understand before submitting their return.

Key Takeaways

- The income tax return last date depends on taxpayer category, assessment year and audit requirement. Do not assume one date applies to every taxpayer.

- For many individual non-audit taxpayers, the normal ITR due date is commonly 31 July of the assessment year, but official extensions or category-specific deadlines must be checked.

- For AY 2026-27, the official e-Filing portal has enabled ITR-1, ITR-2 and ITR-4 utilities, so eligible taxpayers should prepare documents early instead of waiting for the deadline.

- Late filing may attract fee, interest and restrictions on certain loss carry-forwards. A belated return is useful but not equal to an on-time return.

- Balance tax should be paid before filing. Self-assessment tax challan, AIS, TIS and Form 26AS should be checked to avoid mismatches.

- E-verification is essential after filing. Uploading the ITR alone is not enough if verification is pending.

- WealthSure can help with due-date review, document checks, tax computation, filing and post-filing support when the return is complex or the deadline is close.

What This Page Covers

- What readers usually mean when they search for the WealthSure income tax return last date.

- How ITR due dates work for salaried individuals, freelancers, professionals, investors, NRIs and business owners.

- How to check the correct assessment year, financial year, tax payment category and return-filing status.

- What to do before the deadline: documents, AIS, TIS, Form 26AS, self-assessment tax and e-verification.

- What happens if the ITR due date is missed and how a belated return works.

- Practical examples showing common deadline mistakes and better compliance choices.

- Where WealthSure’s expert-assisted ITR filing support can help without replacing official portal verification.

WealthSure income tax return last date is usually searched by taxpayers who want a clear answer before filing: What is the ITR filing due date, what happens if the return is filed late, can I file a belated income tax return after the due date with WealthSure, and what documents are required before the last date? The answer depends on your assessment year, income type, audit requirement, tax payment status and whether the government has announced any extension for the relevant year.

For most individual taxpayers, the deadline question is not only about a calendar date. It is about avoiding last-minute errors: selecting the wrong assessment year, missing interest income, ignoring AIS or Form 26AS, forgetting self-assessment tax, entering the wrong bank account, or filing the return but not e-verifying it. A return that is prepared early gives you time to correct TDS mismatch, collect capital gains statements, compare old and new tax regime outcomes, and pay any balance tax before submission.

This guide is written for Indian salaried professionals, first-time filers, freelancers, investors, NRIs, small business owners and families who want a practical, customer-focused explanation. It covers the income tax return due date, late filing fees, belated return, revised return, updated return context, documents required, payment proof, and post-filing verification. It also explains when self-service filing may be enough and when assisted filing becomes safer.

WealthSure can help users with ITR filing services, document review, balance tax calculation, deadline planning and expert-assisted filing. The aim is not to create panic around the last date. The aim is to help you file accurately, on time where possible, and with enough documentation to handle future questions from the Income Tax Department.

Quick Answer: WealthSure Income Tax Return Last Date

The WealthSure income tax return last date guide helps you identify the official ITR due date that applies to your tax profile. WealthSure does not create the statutory deadline; the due date comes from the Income-tax Act, CBDT notifications and the Income Tax e-Filing portal. For many non-audit individual taxpayers, the normal return filing due date is commonly 31 July of the assessment year, while audit cases and certain business or professional taxpayers may have later due dates.

For AY 2026-27, the official Income Tax e-Filing portal has enabled ITR utilities for common forms such as ITR-1, ITR-2 and ITR-4. Eligible taxpayers should not wait for the last week. Check your Form 16, AIS, TIS, Form 26AS, bank interest, capital gains, deductions and any self-assessment tax requirement before filing.

If you miss the original due date, a belated return may still be possible within the statutory time limit. However, late filing may involve a fee, interest, restrictions on certain losses and reduced flexibility. WealthSure can help you decide whether to file a normal return, belated return, revised return or updated return based on facts.

Methodology and Official Sources

This article is based on practical ITR filing workflow for Indian taxpayers, official due-date concepts under the Income-tax framework, and the current public filing environment visible on the official Income Tax e-Filing portal. It also refers to the Income Tax Department’s public guidance on return of income, belated returns and official taxpayer resources.

Tax rules, filing utilities, portal screens, payment categories and government extensions may change by assessment year. Users should always confirm the latest official deadline from the Income Tax Department, CBDT circulars and the e-Filing portal before taking action. If the deadline is close or your income profile is complex, WealthSure can assist with interpretation, filing, tax computation and compliance support.

Useful official and regulatory sources include the Income Tax e-Filing portal, the Income Tax Department website, SEBI for investor-market context, and India.gov.in for government-service navigation.

What Does Income Tax Return Last Date Mean?

The income tax return last date is the statutory deadline by which a taxpayer should file the return for a particular assessment year. It is linked to the income earned during the financial year and is not the same as the date on which tax was deducted from salary or the date on which you downloaded Form 16.

For example, income earned from 1 April 2025 to 31 March 2026 belongs to Financial Year 2025-26 and is generally reported in Assessment Year 2026-27. The due date for filing depends on whether you are a non-audit individual, a business owner requiring audit, a company, a partner in a firm, or a taxpayer with special reporting obligations.

The last date matters because it affects late filing fee, interest, certain loss carry-forwards, speed of refund processing and the overall compliance trail. Filing before the due date gives more flexibility to correct errors through a revised return within the allowed time, while late filing narrows your options.

Income Tax Return Due Date: Who Should Check Which Deadline?

The correct ITR filing deadline depends on your taxpayer category. The table below is a practical guide, but the latest official notification should always be checked for the relevant assessment year.

| Taxpayer type | Typical due-date concern | What to check before filing |

|---|---|---|

| Salaried individual without audit | Usually the normal individual ITR due date applies | Form 16, AIS, TIS, Form 26AS, bank interest, deductions and regime selection |

| Freelancer or professional | May be normal due date or audit due date depending on receipts and rules | Invoices, expenses, TDS, advance tax, books, presumptive taxation and audit applicability |

| Investor with capital gains | Deadline may be normal, but computation can take time | Broker statement, STCG, LTCG, dividend, losses, AIS matching and tax payment |

| NRI taxpayer | Deadline depends on income profile and reporting obligations | Residential status, Indian income, TDS, DTAA, bank account and foreign asset rules if applicable |

| Business owner or audited case | Audit and return due dates may differ from non-audit taxpayers | Books, tax audit, GST data, TDS, loans, depreciation, advance tax and challans |

| Taxpayer filing after original due date | Belated return window and late fee must be checked | Late fee, interest, tax payment, loss restrictions and e-verification |

Many filing mistakes happen because taxpayers focus only on the public headline date. The better approach is to identify your category first, then confirm the assessment year and latest official due-date update.

What Should You Do Before the Income Tax Return Last Date?

Before the last date, you should complete document collection, tax credit matching, tax regime comparison, balance tax payment and e-filing preparation. Filing in the final hours can lead to wrong entries, missed income and verification delays.

Documents and details to keep ready

- PAN, Aadhaar and mobile number linked for OTP-based actions.

- Form 16 from current and previous employers, where applicable.

- AIS, TIS and Form 26AS for TDS, TCS, interest, dividend, securities and high-value information.

- Bank interest certificates, fixed deposit interest, savings account interest and any other income details.

- Capital gains statements from brokers, mutual fund platforms and other investment records.

- Home loan interest certificate, rent receipts, donation receipts, insurance and eligible deduction proofs where relevant.

- Advance tax and self-assessment tax challans, if any.

- Foreign income, NRI income or foreign asset details where applicable.

If your return is simple, you may file through free income tax filing or self-service support. If your income includes capital gains, freelance receipts, business income or NRI income, expert-assisted review can reduce avoidable errors.

Do You Need to Pay Tax Before Filing the Return?

You need to pay tax before filing if your final liability is higher than your available tax credits. This usually happens when salary TDS is short, interest income was not fully taxed, capital gains tax is payable, advance tax was missed, or freelance and business income was earned without adequate TDS.

Taxpayers often confuse ITR filing with tax payment. Filing the return reports income, deductions, taxes and refund or payable amount. Tax payment clears the liability. If the return shows tax payable, you should generally pay self-assessment tax, enter or validate challan details and then submit the return.

| Payment type | When it usually applies | Common taxpayer example |

|---|---|---|

| Advance tax | Paid during the financial year when estimated tax liability crosses the prescribed threshold | Freelancer, business owner or investor with significant taxable income not fully covered by TDS |

| Self-assessment tax | Paid after year-end but before filing ITR when final tax payable remains | Salaried employee with bank interest or capital gains not fully covered by TDS |

| Regular assessment tax | Paid after the department raises a demand during assessment or processing | Taxpayer receiving a demand due to mismatch or short payment |

For tax payment support before filing, WealthSure’s advance tax calculation and filing assistance can help users compute the payable amount and reduce mismatch risk.

What Happens If You Miss the ITR Filing Due Date?

If you miss the original ITR filing due date, you may still be able to file a belated return within the allowed time limit. However, late filing can create financial and compliance consequences.

A belated return helps you report income, claim eligible tax credit and complete filing after the original due date. But it may come with a late fee under section 234F, interest if tax was unpaid, and restrictions on carrying forward some losses. The exact outcome depends on income, tax payable, filing date, return type and applicable law.

For AY 2026-27, official Income Tax Department guidance explains that the last date for belated return is 31 December 2026 unless assessment is completed earlier. Taxpayers should not treat this as a reason to delay intentionally. Filing on time gives better flexibility, especially when corrections are needed later.

Best for clean compliance, quicker correction options and avoiding late filing fee where applicable.

Useful when the due date is missed, but late fee, interest and some restrictions may apply.

Assessment Year vs Financial Year: What Should You Select?

You should select the assessment year that corresponds to the financial year in which income was earned. A wrong assessment year can lead to incorrect filing, payment mismatch and avoidable follow-up work.

The financial year is the period in which you earn income. The assessment year is the next year in which that income is reported and assessed. For income earned during FY 2025-26, the corresponding assessment year is AY 2026-27. When paying self-assessment tax or filing ITR, this selection must match.

| Income earned during | Financial year | Assessment year for ITR |

|---|---|---|

| 1 April 2024 to 31 March 2025 | FY 2024-25 | AY 2025-26 |

| 1 April 2025 to 31 March 2026 | FY 2025-26 | AY 2026-27 |

| 1 April 2026 to 31 March 2027 | FY 2026-27 | AY 2027-28 |

This is one of the most common mistakes in last-minute filing. If you paid tax under the wrong assessment year, professional review may be needed to understand correction or refund options.

How to Verify Tax Payment, TDS and ITR Filing Status

You should verify tax payment and tax credits before and after filing to ensure the return matches official records. This reduces the chance of mismatch notices, processing delays and incorrect refund expectations.

After paying tax, download the challan or payment receipt and check whether it reflects in tax payment history, AIS or Form 26AS when updated. After filing, download the ITR acknowledgement and complete e-verification. Keep all proofs together with your computation and supporting documents.

If your money was deducted but the challan was not generated, do not immediately make a duplicate payment without checking bank status, payment history and official guidance. WealthSure’s Ask Our Tax Expert support can help you understand the next step based on evidence.

Common Mistakes to Avoid Near the Income Tax Return Last Date

The most common deadline mistakes happen when taxpayers rush the return without matching documents and tax credits. A few careful checks can prevent many post-filing problems.

| Mistake | Why it creates a problem | Better approach |

|---|---|---|

| Choosing the wrong assessment year | Tax payment and return may not match the income period | Map financial year to assessment year before payment or filing |

| Ignoring AIS and Form 26AS | Reported income may differ from your return | Compare salary, interest, dividends, securities and TDS entries |

| Filing without paying balance tax | Return may show tax payable or trigger demand | Pay self-assessment tax and verify challan details |

| Missing capital gains or dividend income | Broker and depository data may be reported to the department | Use capital gains statements and reconcile with AIS |

| Forgetting e-verification | Uploaded return may remain incomplete | E-verify immediately and save acknowledgement |

| Assuming refund is guaranteed | Refund depends on processing and correct reporting | File accurately and track official processing status |

Practical Examples: Deadline Questions Indian Taxpayers Actually Face

Real tax filing decisions are rarely about one date only. They involve documents, income sources, TDS, tax payments and verification. These examples show how to think before the last date.

Example 1: Salaried employee paying self-assessment tax before filing ITR

Neha works in Pune and has Form 16 from her employer. She assumes TDS covers everything, but her AIS shows savings interest, fixed deposit interest and dividend income. Her common mistake would be filing the return without checking whether additional tax is payable. The correct approach is to include all income, compute final tax, pay self-assessment tax if needed, verify the challan and then file. WealthSure can help by reviewing Form 16, AIS, interest income and regime selection before submission.

Example 2: Freelancer paying advance tax to reduce interest

Aman is a freelance designer receiving payments from Indian and overseas clients. TDS is deducted on some invoices, but not all receipts. He waits until the ITR last date and then discovers interest liability because advance tax was not paid properly. The better approach is to estimate income during the year, pay advance tax where required, maintain invoices and expenses, and file with a clean computation. WealthSure’s assisted filing and business and professional income filing support can help freelancers avoid last-minute confusion.

Example 3: Investor with capital gains before the due date

Rakesh sold equity shares, mutual funds and some debt investments during the year. His broker statement has short-term and long-term capital gains, but AIS also shows dividend income. The common mistake is copying only one statement and ignoring the tax treatment of different assets. The correct approach is to reconcile broker reports, AIS, exemptions, losses and tax payment before filing. WealthSure’s ITR-2 capital gains filing support can help investors prepare a more accurate return.

Example 4: NRI taxpayer checking Indian income and due date

Priya lives in Dubai but earns rent from property in India and has NRO bank interest. She thinks she does not need to file because she is outside India. The correct approach is to check residential status, Indian taxable income, TDS, DTAA position if relevant and refund eligibility. If filing is required or useful, she should prepare documents before the due date. WealthSure’s NRI income tax filing service can help with Indian-source income and documentation.

Income Tax Return Last Date Checklist

Use this checklist at least a few days before the filing deadline. It helps you avoid rushing the return and missing important compliance steps.

- Confirm the correct assessment year for the income you are filing.

- Check whether you are a non-audit or audit taxpayer.

- Download Form 16, AIS, TIS and Form 26AS.

- Collect bank interest, dividend, rent, capital gains and freelance income details.

- Compare old and new tax regime only where both are legally available and relevant.

- Compute final tax liability and pay self-assessment tax if required.

- Check challan details after payment and preserve the receipt.

- File the ITR using the correct form and income heads.

- E-verify the return and save the acknowledgement.

- Track processing, refund or demand status on the official portal.

How WealthSure Can Help Before the ITR Filing Deadline

WealthSure can help when the last date is close, documents are scattered, tax credits do not match, or your income is more complex than a simple salary return. The support can include due-date review, document checklist, income classification, tax regime comparison, self-assessment tax calculation, ITR preparation, e-verification guidance and post-filing support.

For simple cases, self-service filing may be enough. For capital gains, freelance income, NRI income, multiple employers, house property, business income, notices or TDS mismatches, assisted filing can be more practical. WealthSure’s role is to make the process clearer and more documented, not to promise guaranteed refunds or guaranteed tax savings.

Summary: WealthSure Income Tax Return Last Date

The WealthSure income tax return last date guide explains how Indian taxpayers should identify the correct ITR filing deadline, prepare documents, pay balance tax and complete e-verification. The official deadline depends on assessment year, taxpayer category, income sources and audit requirement.

For many non-audit individual taxpayers, the normal ITR due date is commonly 31 July of the assessment year, but official updates and category-specific timelines must be checked. If the original due date is missed, a belated return may still be possible within the statutory window, though late fee, interest and restrictions may apply.

The safest approach is to prepare early: collect Form 16, AIS, TIS, Form 26AS, capital gains statements, interest details, deduction proofs and challans. WealthSure can support taxpayers with expert-assisted ITR filing, due-date interpretation, self-assessment tax computation and post-filing checks.

FAQs on WealthSure Income Tax Return Last Date

What is the WealthSure income tax return last date for Indian taxpayers?

The WealthSure income tax return last date guide helps Indian taxpayers understand the official ITR due date that applies to their case. The due date is not created by WealthSure; it is determined under income-tax law and notified through the Income Tax Department or CBDT. For many individual taxpayers without audit requirements, the normal due date is commonly 31 July of the assessment year, while audit cases and special cases may have different timelines. Taxpayers should check the assessment year, income type, audit requirement and latest official updates before filing. WealthSure can help interpret the applicable date and prepare the return accurately.

What happens if I file my income tax return after the due date?

If you file after the due date, the return is generally treated as a belated return, subject to the time limit and conditions under the Income-tax Act. A late filing fee under section 234F may apply, and interest may also apply if tax remains unpaid. Some losses may not be carried forward when the original due date is missed, except where law allows it. A belated return can still be useful because it helps complete compliance, claim eligible refund subject to processing, and avoid leaving income undisclosed. WealthSure can help review your documents before belated filing.

Can I file a belated income tax return with WealthSure?

Yes, WealthSure can assist with belated income tax return filing where the statutory time limit is still open. For AY 2026-27, the Income Tax Department explains that the last date for a belated return is 31 December 2026 unless the assessment is completed earlier. The taxpayer still needs to disclose income correctly, pay any balance tax and interest, and complete e-verification. Belated filing is not the same as filing on time because some benefits may be restricted. Expert review is useful when salary, capital gains, business income, foreign income or TDS mismatch is involved.

Which documents should I keep ready before the ITR filing due date?

Before the ITR filing due date, keep PAN, Aadhaar, bank details, Form 16, salary slips, interest certificates, home loan statements, rent details if relevant, capital gains reports, AIS, TIS and Form 26AS ready. Freelancers and professionals should also keep invoices, expense records, GST or TDS details where applicable, and advance tax challans. Investors should collect broker capital gains statements and dividend details. Document readiness reduces errors and makes filing faster. WealthSure can help organize documents, identify missing information and prepare the return based on the right income heads and tax regime.

How do I know whether I should file before 31 July or a later due date?

Your due date depends on your taxpayer category and whether audit or special reporting rules apply. Many salaried individuals and non-audit taxpayers generally follow the normal individual due date, while business owners, professionals requiring audit, companies and some specified taxpayers may have different deadlines. The safest approach is to identify your assessment year, income sources and audit requirement before assuming a date. If you have business turnover, professional receipts, capital gains, foreign assets, partnership income or complex income, expert review is safer. WealthSure can help confirm the applicable deadline before filing.

Do I need to pay tax before filing my income tax return?

Yes, if your final tax liability is higher than TDS, TCS, advance tax and eligible credits, you should pay the balance as self-assessment tax before filing your ITR. Filing without clearing payable tax can create processing issues, interest and demand notices. The challan details should be checked in the tax payment history, AIS or Form 26AS when available. You should choose the correct assessment year and payment category while paying tax. WealthSure can assist with tax computation, self-assessment tax calculation and matching tax credits before filing.

Can WealthSure help if my AIS, Form 26AS or TDS details do not match?

Yes, WealthSure can help review AIS, TIS, Form 26AS and TDS information before return filing. Mismatches may happen because an employer, bank, broker or deductor has reported data differently or late. A mismatch should not be ignored because the Income Tax Department may compare your ITR with reported information. The correct approach is to verify the source, collect proof, report income accurately and use the feedback or correction process where applicable. Expert support is helpful when the mismatch involves capital gains, foreign income, multiple employers, interest income or business receipts.

What should I do if I missed the income tax return last date but have a refund?

If you missed the original due date and have a refund, check whether the belated return window is still open for the relevant assessment year. A belated return may still allow you to report income and claim a refund, but refund processing is subject to Income Tax Department verification and applicable law. You should not file casually only because a refund is expected; all income and deductions must be supported by documents. If the belated window is closed, updated return rules may need to be reviewed, but updated returns do not operate like normal refund claims. WealthSure can help assess the available option.

Is e-verification required after filing before the last date?

Yes, filing is not fully complete until the ITR is verified within the prescribed timeline. E-verification can generally be completed using Aadhaar OTP, net banking, bank account validation, demat account validation or other available methods on the official e-Filing portal. If verification is delayed or missed, the return may not be treated as validly filed. Taxpayers should download the acknowledgement and keep proof of submission and verification. WealthSure can guide users through the filing and verification workflow so the return does not remain incomplete after upload.

When should I use WealthSure expert-assisted ITR filing instead of self-filing?

Self-filing may be enough for a simple salary return with clean Form 16, matched AIS and no special income. Expert-assisted filing is safer when you have capital gains, F&O or crypto reporting, freelance income, business income, NRI status, foreign assets, multiple employers, house property income, notice history, high-value transactions or TDS mismatches. It is also useful when the filing deadline is close and you want document review before submission. WealthSure’s role is to help you file accurately, pay any balance tax correctly, verify the return and maintain compliance records without overpromising refunds or tax savings.

Conclusion: File Before the Last Date With Better Preparation

The income tax return last date matters because it is connected with accurate filing, timely tax payment, e-verification, refund processing and future compliance records. A taxpayer who prepares early can check the correct assessment year, match AIS and Form 26AS, collect documents, compute tax and avoid rushed mistakes.

Self-service may be enough for a straightforward salary return with clean tax credits. Expert-assisted support is safer when the return involves capital gains, freelance income, business income, NRI status, tax payment confusion, TDS mismatch or belated filing. WealthSure can help you turn a deadline-driven task into a documented and more confident filing process.

At WealthSure, we don’t just file taxes — we simplify your financial journey and help you build long-term wealth with confidence.