WealthSure Income Tax Slab Article: Old vs New Regime Guide

This WealthSure income tax slab article explains how Indian taxpayers can understand slab rates, compare the old and new tax regimes, use rebate rules correctly and plan ITR filing without relying on confusing headlines.

Key Takeaways

- Income tax slabs are progressive; only the income falling in a slab is taxed at that slab rate, not your full income.

- The new tax regime is generally the default regime, but eligible taxpayers can compare and choose the old regime where deductions make it better.

- FY 2024-25 and FY 2025-26 have different new-regime slab structures, so taxpayers must check the correct assessment year before planning.

- Section 87A rebate is not the same as a slab; rebate eligibility depends on residential status, income type, tax regime and year-specific rules.

- Senior citizens may have age-based benefits under the old regime, while the new regime has its own structure under Section 115BAC.

- Capital gains, freelance income and foreign income can change the calculation, even when salary income looks simple.

- WealthSure can help with regime comparison, ITR filing and tax planning when the slab table alone is not enough.

What This Page Covers

- Income tax slabs for FY 2024-25 and FY 2025-26 in practical Indian context.

- How to compare the old tax regime and the new tax regime before filing ITR.

- How Section 87A rebate and standard deduction affect tax liability.

- How senior citizens, freelancers, investors and NRIs should read slab tables.

- Common mistakes taxpayers make while choosing a tax regime.

- Practical examples for salary, freelance income, capital gains and mixed income.

- When WealthSure’s assisted filing or personal tax planning support can help.

WealthSure income tax slab article is a useful search when you want a clear, practical explanation of income tax slabs, old regime vs new regime, FY 2024-25 and FY 2025-26 slab rates, Section 87A rebate, standard deduction and tax planning in India. Most taxpayers do not search for slab rates only to read a table. They search because they want to know how much tax they may pay, whether the new regime is better, whether deductions still matter, and how to avoid a wrong choice before employer declaration or ITR filing.

The confusion is understandable. A headline may say “no tax up to ₹12 lakh”, another page may show ₹3 lakh as the nil slab, and a salary calculator may show a different number after standard deduction. The missing link is that slab rate, rebate, deduction, cess and regime choice are different parts of the calculation. A slab tells you the rate for a range of income. A rebate reduces tax payable if eligibility conditions are met. A deduction reduces taxable income if the law allows it. The final tax amount depends on all of these pieces together.

For Indian taxpayers, the stakes are practical. A salaried person may have to choose a regime with the employer early in the year. A freelancer may need to estimate advance tax. An investor may need to include capital gains that are taxed at special rates. A senior citizen may need to check age-based limits. An NRI may need to review Indian income, TDS and residential status before assuming that the same slab logic applies. A small mismatch between the assessment year, income type and regime can lead to incorrect tax calculation or unnecessary follow-up work during filing.

This guide explains the income tax slab system in plain language and connects it with real filing decisions. It uses official tax-rate context from the Income Tax e-Filing portal, the Income Tax Department tax rates page and the official old regime vs new regime tax calculator. WealthSure can help when you need expert-assisted comparison, ITR filing support, capital gains reporting or personal tax planning based on your documents rather than generic slab charts.

Quick Answer: WealthSure Income Tax Slab Article

An income tax slab article explains how your taxable income is divided into different ranges and taxed at different rates. In India, individuals generally compare the old tax regime and the new tax regime before filing, because the regime you choose can change your final tax liability.

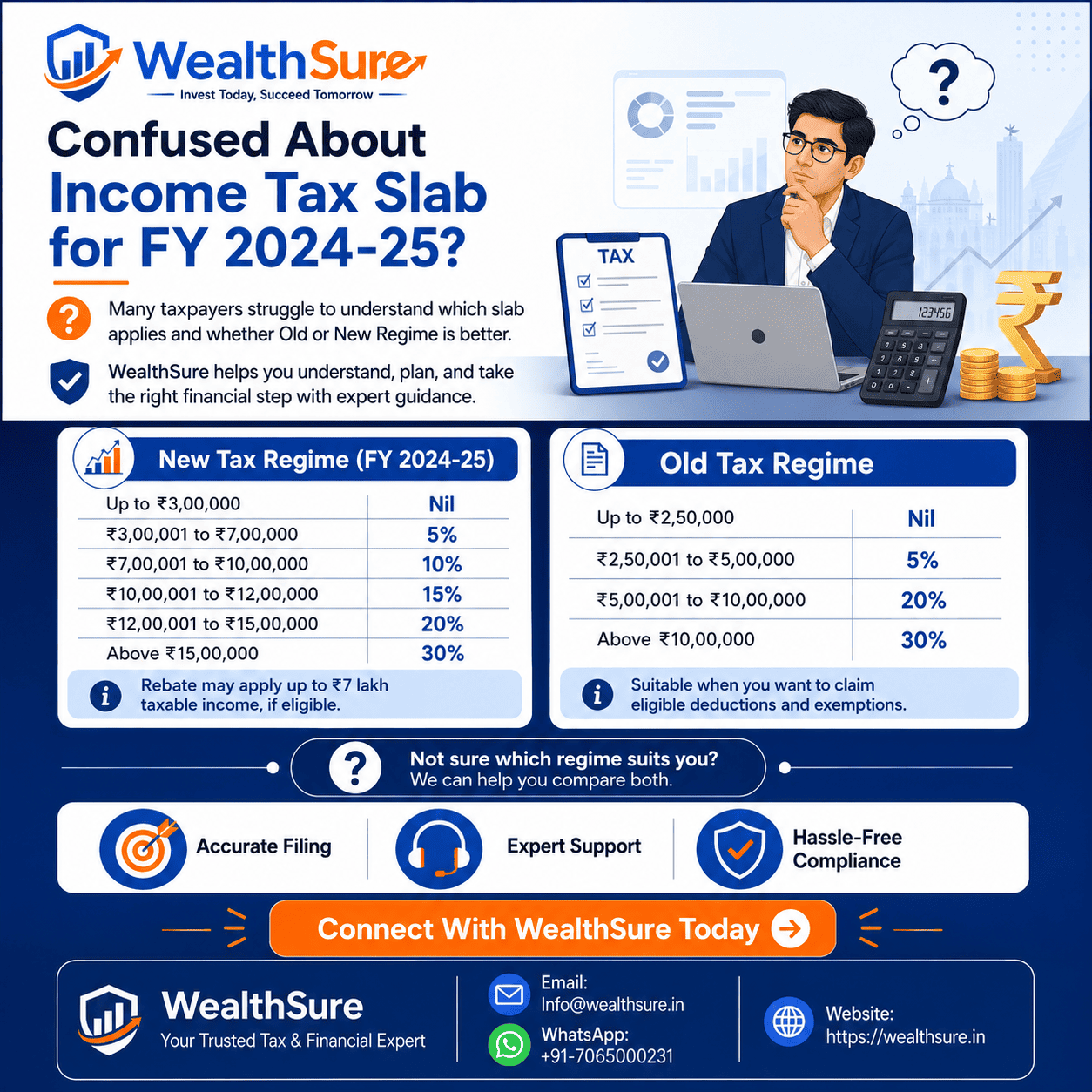

For FY 2024-25, relevant to AY 2025-26, the new regime generally had nil tax up to ₹3 lakh and progressive rates from 5% to 30%. For FY 2025-26, relevant to AY 2026-27, the new regime generally starts with nil tax up to ₹4 lakh and then uses 5%, 10%, 15%, 20%, 25% and 30% bands for higher income levels.

The old regime may still be useful if you have strong eligible deductions and exemptions such as Section 80C investments, HRA, home loan interest, health insurance deduction or other permitted benefits. The new regime may be simpler where deductions are limited, but the correct answer depends on your numbers.

The safest way to use an income tax slab table is to check the financial year, assessment year, income type, residential status, deductions, rebate eligibility and special-rate income. After that, compare both regimes before employer declaration, advance tax payment or ITR filing.

Methodology and Official Sources

This article is based on practical tax-regime comparison for Indian taxpayers who want to understand slab rates before filing ITR or planning tax. It uses official Income Tax Department rate pages, the e-Filing portal and the old-regime-versus-new-regime calculator as primary context. Tax rules, surcharge, cess, rebate eligibility and portal screens may change, so taxpayers should always verify the assessment year before acting.

Important official sources include the Income Tax e-Filing portal, the CBDT Income Tax Department tax rates page, the official tax calculator, the Ministry of Finance announcement on new-regime relief and SEBI where investment and capital-market context is relevant.

The purpose is to make slab tables understandable for human readers and extractable for search and AI answer systems. WealthSure can assist with interpretation, filing and compliance support where a taxpayer’s real income profile is more complex than a basic table.

WealthSure Income Tax Slab Article: Latest Slab Rates to Know

The latest slab rates should always be read with the correct financial year and assessment year. FY 2024-25 usually maps to AY 2025-26, while FY 2025-26 maps to AY 2026-27. Mixing these two years is one of the most common reasons taxpayers get confused while comparing old and new regimes.

The following table gives a reader-friendly view of the individual slab structure commonly relevant for salaried and non-business taxpayers. It is not a substitute for a full tax computation because surcharge, cess, rebate, special-rate income and deductions can change the final amount.

| Financial year | Assessment year | Regime | Key slab structure | Best read with |

|---|---|---|---|---|

| FY 2024-25 | AY 2025-26 | New regime | Nil up to ₹3 lakh; then 5%, 10%, 15%, 20% and 30% bands | Standard deduction, rebate, cess and special-rate income |

| FY 2025-26 | AY 2026-27 | New regime | Nil up to ₹4 lakh; then 5%, 10%, 15%, 20%, 25% and 30% bands | Section 87A rebate, salary deduction and total income type |

| FY 2024-25 and FY 2025-26 | Relevant AY | Old regime | Age-based basic exemption and older progressive rates with deductions | 80C, HRA, home loan interest, 80D and other eligible deductions |

| Any year | Relevant AY | Special-rate income | Capital gains and certain income may not follow normal slab rates | Asset type, holding period, TDS, AIS and documentation |

For a simple salary case, slab comparison may be enough to estimate tax. For a mixed-income case, the taxpayer should go further and check TDS, capital gains, bank interest, deductions and rebate eligibility before finalizing ITR.

Old Tax Regime vs New Tax Regime: Which One Should You Choose?

The right regime is the one that produces a lower lawful tax liability after considering income, deductions, exemptions and rebate eligibility. The new regime is simpler and often attractive when deductions are limited. The old regime can still be useful when your eligible deductions are significant and properly documented.

Under the old regime, taxpayers may be able to claim deductions and exemptions such as Section 80C investments, HRA, certain home loan benefits, health insurance deduction and other items if conditions are met. Under the new regime, the slab rates are generally lower or more spread out, but several traditional deductions are unavailable or restricted. This is why the old-vs-new decision cannot be answered from salary alone.

| Factor | Old tax regime | New tax regime | Practical takeaway |

|---|---|---|---|

| Deductions | Allows many eligible deductions and exemptions | Allows fewer deductions, with some specific allowances | Old regime may suit taxpayers with strong documentation |

| Slab rates | Older progressive slabs | More slab bands and generally simplified calculation | New regime may suit taxpayers with limited deductions |

| Employer declaration | Requires deduction proofs for payroll benefits | Often simpler for salary TDS planning | Choose after comparing, not by habit |

| Senior citizens | Age-based basic exemption limits may matter | Common new-regime structure under Section 115BAC | Retirees should compare carefully |

| Filing decision | May require more paperwork | May be easier, but not always cheaper | Use the official calculator or expert support |

If you need help comparing both regimes before filing, WealthSure’s personal tax planning service and ITR filing support can help you review income, deductions and tax payable using your actual documents.

Why Income Tax Slab Articles Often Show Different Numbers

Different slab articles show different numbers because they may refer to different financial years, assessment years, regimes, taxpayer age groups or rebate assumptions. A page about FY 2024-25 may show a nil slab up to ₹3 lakh under the new regime, while a page about FY 2025-26 may show nil up to ₹4 lakh. Both can be correct for their respective years.

Another source of confusion is the phrase “tax-free income.” A basic exemption slab, a standard deduction and a rebate are not the same thing. For example, a salaried taxpayer may see zero tax at a higher income level because standard deduction and rebate work together. But another taxpayer with special-rate capital gains may not get the same result even if total income appears similar.

A practical rule is to verify four items before trusting any slab table: the financial year, the assessment year, the tax regime and the taxpayer profile. For official confirmation, use the Income Tax Department’s tax-rate page and calculator, then apply the result to your own income details.

Section 87A Rebate, Standard Deduction and Slab Rates Explained

Section 87A rebate reduces tax payable for eligible resident individuals, while the standard deduction reduces salary or pension income before tax is calculated. Slab rates tell you how income is taxed; rebate and deduction decide whether the final tax becomes lower or even nil in qualifying cases.

The percentage applied to a defined band of taxable income. Slabs are progressive and apply portion by portion.

A deduction available from salary or pension income where applicable. It reduces taxable income before tax is computed.

A tax rebate available to eligible resident individuals within specified income limits and regime rules.

An additional levy calculated on tax and surcharge where applicable. It affects the final amount payable.

Many taxpayers make the mistake of treating rebate as a universal exemption. It is not universal. It depends on residential status, income limit, tax regime and nature of income. If you have income taxed at special rates, such as certain capital gains, you should calculate carefully rather than relying on a salary-only example.

Key Tax Terms Explained Before You Use a Slab Table

Understanding basic tax terms helps prevent wrong slab selection and wrong regime comparison. These definitions are especially useful for first-time filers, salaried employees, freelancers and families helping senior citizens file returns.

Financial Year

The financial year is the period in which income is earned. For example, income earned between 1 April 2025 and 31 March 2026 belongs to FY 2025-26.

Assessment Year

The assessment year is the year immediately after the financial year, when income is assessed and ITR is filed. FY 2025-26 generally maps to AY 2026-27.

Taxable Income

Taxable income is the income on which tax is calculated after applying eligible deductions, exemptions, set-offs and adjustments. It is not always the same as gross salary or total bank credits.

New Tax Regime under Section 115BAC

The new tax regime is a concessional tax framework with its own slab structure and fewer deductions than the old regime. It is generally the default regime, but eligible taxpayers should still compare both options.

Old Tax Regime

The old tax regime uses older slab rates and allows many deductions and exemptions if the taxpayer satisfies conditions and has documents to support the claim.

Form 16, AIS and Form 26AS

Form 16 shows salary and TDS details, while AIS and Form 26AS help taxpayers verify TDS, interest, securities transactions and other reported information before filing. A slab calculation is incomplete if reported income is not reconciled.

Step-by-Step Guide to Use Income Tax Slabs for Tax Planning

The best way to use an income tax slab table is to calculate both regimes using the same income data and then choose the legally available option with lower tax. Do not decide based only on one deduction, one headline or one calculator result without checking documents.

Step 1: Identify the correct year. Confirm whether you are planning for FY 2024-25, FY 2025-26 or another year. The assessment year and slab rates must match.

Step 2: List all income sources. Include salary, pension, interest, rent, professional income, business income, capital gains, foreign income and any other taxable income.

Step 3: Separate normal income and special-rate income. Some capital gains or other incomes may not follow normal slab rates. This step matters for rebate and final tax payable.

Step 4: Calculate old-regime deductions. Add only eligible and documented deductions such as Section 80C, eligible HRA, 80D, home loan interest and other permitted items.

Step 5: Calculate new-regime tax. Apply the new slab structure for the correct year, then check standard deduction, rebate, surcharge and cess where applicable.

Step 6: Compare final tax payable. Compare the total tax after rebate, surcharge and cess, not just the base slab calculation.

Step 7: Align filing and payment. If tax remains payable, plan advance tax or self-assessment tax. For filing support, WealthSure’s advance tax calculation and assisted ITR filing starter plan can help simple taxpayers move from estimate to filing.

Practical Examples: How Real Taxpayers Should Use Slab Rates

Income tax slabs become easier to understand when they are applied to real taxpayer situations. The examples below show why the best tax regime depends on income mix, documentation and the assessment year.

Example 1: Salaried employee comparing old and new regime

Neha earns salary income and has Form 16, employee provident fund contribution and health insurance premium. She sees that the new tax regime has lower slab rates and assumes it is automatically better. The common mistake is ignoring eligible old-regime deductions such as Section 80C and 80D. The correct approach is to compute both regimes with the same salary, deduction documents and TDS details. If the difference is small, she should also consider ease of documentation and employer declaration timelines. WealthSure can help her compare regimes and file accurately through Form 16 upload support.

Example 2: Freelancer estimating advance tax

Rahul is a freelance designer earning from Indian and foreign clients. He reads the slab table and calculates tax on gross receipts, which overstates income because business expenses are not considered. The correct method is to calculate professional income after eligible expenses or evaluate presumptive taxation where applicable. He should also track TDS, foreign receipts, invoices and advance tax dates. For freelancers, slab planning is not only about rates; it is about clean records, correct income classification and timely tax payment. WealthSure’s business and professional income filing support can help where income records are complex.

Example 3: Investor with salary and capital gains

Amit earns salary and sells equity mutual funds during the year. He assumes that the Section 87A rebate will remove his entire tax because his salary is within the headline limit. The mistake is ignoring capital gains that may be taxed at special rates and may affect rebate treatment. The correct approach is to calculate salary income under the chosen regime and compute capital gains separately according to asset type and holding period. He should reconcile broker reports with AIS and Form 26AS before filing. WealthSure’s capital gains tax review can help investors avoid under-reporting or wrong tax assumptions.

Example 4: Senior citizen with pension and bank interest

Mrs. Kapoor receives pension and bank interest. Her family looks at a generic slab table for individuals below 60 years and misses age-specific old-regime treatment. The correct approach is to check her age, residential status, pension details, bank TDS, Form 16A and eligible deductions. The old regime may be useful for some senior citizens, while the new regime may work for others. A comparison should be based on actual documents rather than a generic tax chart. WealthSure’s Ask Our Tax Expert service can be useful when family members are unsure about senior citizen filing.

Income Tax Slab Checklist Before You File ITR

Before using an income tax slab chart for filing, verify the items below. This checklist can prevent common mistakes around assessment year, income classification, deductions and rebate assumptions.

- Confirm the correct financial year and assessment year.

- Check whether the slab table is for the old regime or the new regime.

- Separate salary, interest, rent, business income, professional income and capital gains.

- Reconcile Form 16, Form 16A, AIS and Form 26AS before filing.

- Use only eligible and documented deductions under the old regime.

- Check whether Section 87A rebate applies to your residential status and income type.

- Do not ignore surcharge and health and education cess if your income crosses relevant levels.

- Compare both regimes using final tax payable, not only slab rates.

- Pay advance tax or self-assessment tax where required before filing.

- Keep computation, challans and supporting documents safely after filing.

Common Mistakes to Avoid While Reading Income Tax Slabs

The biggest mistake is reading slab rates as if they alone decide tax payable. In reality, the final amount depends on deductions, rebate, cess, surcharge, special-rate income and proper reporting.

| Mistake | Why it misleads | Better approach |

|---|---|---|

| Using the wrong assessment year | Slab rates and rebate limits may differ by year | Match FY and AY before calculating tax |

| Assuming the highest slab applies to all income | India uses progressive slabs for normal income | Apply each rate only to that income portion |

| Ignoring deductions in the old regime | Old regime may become better with strong deductions | Compare documented deductions before choosing |

| Treating rebate as a slab | Rebate has eligibility conditions | Check residential status, income limit and income type |

| Ignoring capital gains | Special rates may apply separately | Review capital gains report, AIS and broker statements |

| Filing without reconciling TDS | Mismatch may delay processing or trigger clarification | Check Form 16, AIS and Form 26AS |

How WealthSure Can Help With Income Tax Slab Planning

WealthSure helps Indian taxpayers move from generic slab charts to accurate tax decisions based on real documents. If your case is simple, a self-service tax calculator and clear Form 16 may be enough. If you have multiple incomes, capital gains, freelance receipts, foreign income, senior citizen concerns or uncertainty about regime choice, expert-assisted review can reduce avoidable mistakes.

WealthSure can assist with old-vs-new regime comparison, free income tax filing for eligible simple cases, assisted ITR filing, tax optimizer review, capital gains reporting and advance tax planning. The focus is practical: correct income disclosure, lawful deduction use, clean documentation and confident filing.

Summary: WealthSure Income Tax Slab Article

This WealthSure income tax slab article explains how Indian taxpayers should read slab rates, compare the old and new tax regimes, understand rebate rules and avoid common filing mistakes. Income tax slabs are progressive, which means each rate applies only to the income falling within that slab band.

For FY 2024-25 and FY 2025-26, taxpayers should check the correct assessment year before using any slab table. The new tax regime has changed slab structures across years, while the old regime remains relevant for eligible taxpayers with strong deductions and exemptions.

Section 87A rebate, standard deduction, surcharge, cess and special-rate income can all affect final tax payable. A taxpayer with only salary may have a simpler calculation, while a freelancer, investor, NRI or senior citizen may need deeper review. WealthSure can help connect slab understanding with accurate ITR filing and practical tax planning.

FAQs on WealthSure Income Tax Slab Article

What is the WealthSure income tax slab article about?

This WealthSure income tax slab article explains how Indian taxpayers should read income tax slabs, compare the old and new tax regimes, understand rebate rules and avoid common planning mistakes. It is written for salaried individuals, freelancers, investors, senior citizens and families who want a practical explanation before filing their income tax return. The article covers FY 2024-25 and FY 2025-26 context, tax slab rates, standard deduction, Section 87A rebate, examples and checklist-style decision points. It also explains why a low slab rate alone should not decide your regime choice. The correct approach is to compare taxable income, eligible deductions, exemptions, special-rate income, surcharge, cess and documentation before filing.

Which income tax regime is default for individual taxpayers?

The new tax regime under Section 115BAC is generally the default regime for many individual taxpayers, while the old regime can still be chosen if it is more beneficial and the taxpayer is eligible to opt for it. The practical meaning is simple: do not assume that last year’s choice will automatically remain best for the current year. A salaried person with limited deductions may find the new regime easier, while someone with HRA, home loan interest, Section 80C investments or other eligible deductions may still need a comparison. Before filing, taxpayers should verify the applicable assessment year, income sources and available deductions. WealthSure’s assisted filing support can help compare both regimes before the return is submitted.

What are the new tax regime slabs for FY 2025-26?

For FY 2025-26, relevant to AY 2026-27, the new tax regime slabs for individuals generally start with nil tax up to ₹4 lakh, followed by progressive rates of 5%, 10%, 15%, 20%, 25% and 30% across higher income bands. The exact calculation also depends on rebate eligibility, standard deduction for salary or pension where applicable, surcharge, health and education cess, and whether any income is taxed at special rates. A common mistake is to read “no tax up to ₹12 lakh” as a slab, when it is actually connected to rebate rules for eligible resident individuals under the new regime. Taxpayers with capital gains or other special income should check the calculation carefully before assuming zero tax.

How is the old tax regime different from the new tax regime?

The old tax regime has fewer slab bands but allows several deductions and exemptions, while the new tax regime generally offers lower slab rates with fewer deductions. Under the old regime, taxpayers may claim eligible deductions such as Section 80C, certain HRA benefits, home loan interest and other permitted items, subject to conditions. Under the new regime, the calculation is usually simpler, but many deductions are restricted. The best choice depends on your actual numbers, not on a generic rule. For example, two people with the same salary may choose different regimes because one has rent, housing loan interest and tax-saving investments while the other does not. A regime comparison should be done before ITR filing or employer declaration.

Can salaried individuals have zero tax up to ₹12.75 lakh?

Eligible salaried individuals may have zero tax on income up to ₹12.75 lakh under the new tax regime in FY 2025-26 because the standard deduction can reduce salary income and the Section 87A rebate may apply up to the relevant limit. However, this is not the same as saying every income up to ₹12.75 lakh is automatically tax-free in every situation. Special-rate income, capital gains, non-resident status, surcharge situations, or ineligible income types can change the result. Taxpayers should calculate tax after considering salary, other income, deductions, rebate eligibility and cess. If the return includes capital gains, foreign income or professional income, expert review may be safer than relying only on a headline.

Do senior citizens get different income tax slabs?

Senior citizens and super senior citizens may get different basic exemption limits under the old tax regime, while the new tax regime uses its own slab structure under Section 115BAC. A resident senior citizen who is 60 years or more but below 80 years, and a resident super senior citizen who is 80 years or more, should check age-specific rules before comparing regimes. The new regime may still be attractive for some retirees, but the old regime can matter where eligible deductions, interest income treatment and documentation are relevant. Pensioners should also consider standard deduction eligibility, bank interest, Form 16, Form 16A and TDS reflected in Form 26AS or AIS before filing.

Should I choose the old regime if I have Section 80C investments?

Section 80C investments alone do not automatically make the old regime better. The decision depends on the total value of eligible deductions and exemptions compared with the lower slab rates available under the new regime. A taxpayer with Section 80C, HRA, home loan interest, health insurance deduction and other eligible benefits may find the old regime useful. Another taxpayer with only a small deduction may still pay less under the new regime. The correct approach is to calculate tax under both regimes for the same assessment year and then choose the option that is legally available and financially better. WealthSure’s tax planning support can help document this comparison clearly.

How should freelancers and professionals read income tax slabs?

Freelancers and professionals should read income tax slabs after estimating net taxable income, not gross receipts. Business or professional receipts may be reduced by allowable expenses, depreciation where applicable and other eligible adjustments before taxable income is computed. Some professionals may also evaluate presumptive taxation if eligible. After taxable income is determined, the relevant slab regime can be compared. A common mistake is to look only at bank credits and assume the same amount is taxable income. Freelancers should also track advance tax, TDS, GST implications where applicable, invoices, expense proofs and AIS entries. Assisted filing can be helpful when income comes from multiple clients, platforms or foreign sources.

How do capital gains affect income tax slab calculations?

Capital gains can affect your tax calculation because some gains are taxed at special rates instead of normal slab rates. Salary, interest or business income may be taxed according to slab rates, but short-term and long-term capital gains may follow separate rules depending on the asset, holding period and transaction type. This can also affect rebate assumptions under the new regime. Investors should not rely only on a salary-based slab table if they sold shares, mutual funds, property or foreign assets during the year. They should reconcile broker statements, capital gains reports, AIS, Form 26AS and bank entries before filing. WealthSure can help with capital gains tax review where the calculation is not straightforward.

When should I take expert help for income tax slab planning?

Expert help is useful when your tax situation has more than one income source, high deductions, capital gains, foreign income, NRI status, business receipts, notice history or uncertainty about regime selection. Self-service may be enough for simple salary income where Form 16, AIS and deduction documents match cleanly. But when a small error can change tax liability, interest, refund processing or compliance records, guided review is often worth considering. Income tax slab planning is not only about reading a table. It is about applying the right assessment year, choosing the correct regime, reporting all income, claiming only eligible deductions and keeping documents ready. WealthSure can assist with ITR filing, advance tax review, capital gains reporting and personal tax planning.

Conclusion: Use Income Tax Slabs as a Planning Tool, Not a Shortcut

Income tax slab rates help you estimate tax, but they do not complete your tax planning by themselves. The correct tax outcome depends on financial year, assessment year, tax regime, deductions, standard deduction, rebate eligibility, capital gains, cess, surcharge and proper reporting of income.

Self-service may be enough if your income is simple, your Form 16 matches AIS and you have no capital gains or complex deductions. Expert-assisted support becomes useful when you are unsure about old vs new regime, have freelance income, sold investments, receive foreign income, are an NRI, care for a senior citizen taxpayer or need a clean computation before filing.

At WealthSure, we don’t just file taxes — we simplify your financial journey and help you build long-term wealth with confidence.