Income Tax Slab for AY 2025-26: Old vs New Regime Guide for Indian Taxpayers

The income tax slab for AY 2025-26 matters because it decides how much tax you may need to pay on income earned during FY 2024-25. For many Indian taxpayers, the confusion is not only about the slab rate. The bigger question is whether the old tax regime or the new tax regime gives a better result after considering salary income, standard deduction, 80C investments, HRA, home loan interest, health insurance, NPS, capital gains, freelance income and other sources of income.

AY 2025-26 is especially important because many taxpayers are now used to the new tax regime being the default option, but the old regime can still be relevant where eligible deductions and exemptions are meaningful. A salaried employee with provident fund, life insurance, HRA and home loan interest may see a different outcome from a professional with business income or a first-time taxpayer with limited deductions. Similarly, a taxpayer with capital gains, foreign income, NRI status or multiple employers should not look at slab rates in isolation.

This guide explains the income tax slabs for AY 2025-26 in a practical way. You will find a side-by-side comparison of the old and new regimes, rebate rules, surcharge and cess logic, examples for different taxpayer profiles and common mistakes to avoid while filing. The goal is to help you move from “What is my slab?” to “What is my correct tax position?”

WealthSure, as a fintech-powered tax filing and advisory platform, helps taxpayers evaluate their income, deductions, documents and filing strategy before submission. You may be able to file a simple return yourself, but when income sources, deductions, capital gains, business receipts or regime selection are involved, expert review can reduce avoidable errors and improve compliance confidence. Tax rules may change by assessment year, so always verify current forms, filing utilities and instructions on the official Income Tax e-Filing portal before filing.

Quick answer: income tax slab for AY 2025-26

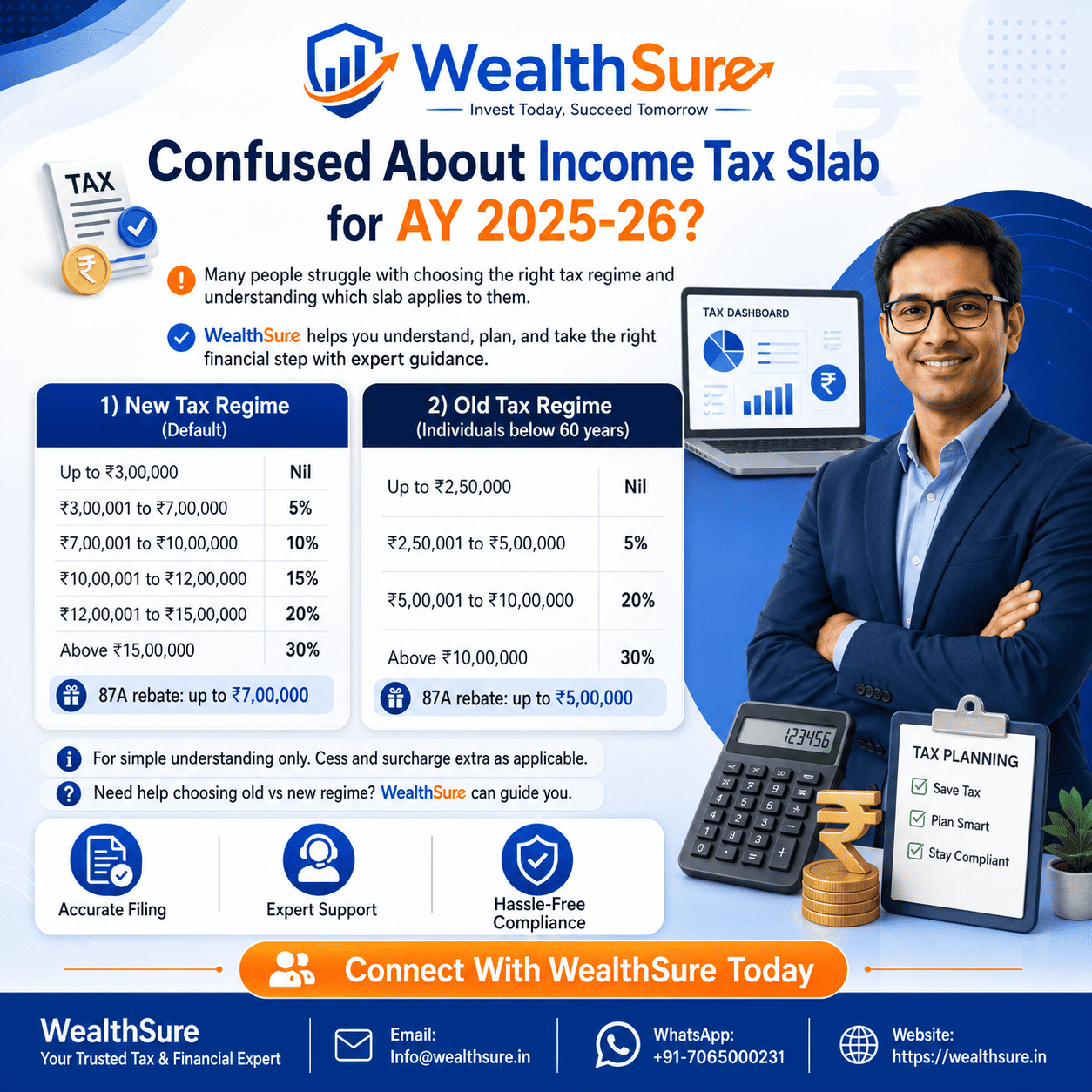

For AY 2025-26, individuals generally need to compare the old tax regime and the new tax regime. The new regime offers revised slab rates and fewer deductions, while the old regime follows higher slabs but allows several eligible deductions and exemptions. In both cases, final tax also depends on rebate, surcharge, health and education cess, residential status and specific income categories.

New tax regime slab for AY 2025-26

| Taxable Income Range | Tax Rate Under New Regime | Planning Note |

|---|---|---|

| Up to ₹3,00,000 | Nil | No tax on this slab |

| ₹3,00,001 to ₹7,00,000 | 5% | Rebate may matter for eligible resident individuals |

| ₹7,00,001 to ₹10,00,000 | 10% | Compare after standard deduction and eligible benefits |

| ₹10,00,001 to ₹12,00,000 | 15% | Useful for many middle-income taxpayers with limited deductions |

| ₹12,00,001 to ₹15,00,000 | 20% | Check salary structure and eligible deductions before deciding |

| Above ₹15,00,000 | 30% | Surcharge may apply at higher income levels |

Old tax regime slab for AY 2025-26 for individuals below 60 years

| Taxable Income Range | Tax Rate Under Old Regime | Planning Note |

|---|---|---|

| Up to ₹2,50,000 | Nil | Basic exemption for individuals below 60 years |

| ₹2,50,001 to ₹5,00,000 | 5% | Section 87A rebate may apply to eligible resident individuals |

| ₹5,00,001 to ₹10,00,000 | 20% | Deductions can significantly influence effective tax |

| Above ₹10,00,000 | 30% | Old regime may still work if deductions and exemptions are strong |

Important: Senior citizens and super senior citizens have different basic exemption limits under the old regime. Also, health and education cess at 4% applies on income tax plus surcharge, where applicable. For official updates, refer to the Income Tax Department of India.

AY 2025-26 vs FY 2024-25: why the year matters

Many taxpayers mix up assessment year and financial year. This can lead to wrong searches, wrong form selection and sometimes wrong assumptions about the applicable tax slab. AY 2025-26 is the assessment year for income earned during FY 2024-25. In simple terms, you earn income from 1 April 2024 to 31 March 2025, and the return is assessed for AY 2025-26.

When you search for the income tax slab for AY 2025-26, you are usually trying to understand the slabs applicable to FY 2024-25 income. This distinction matters because Budget changes may apply from a particular financial year and may not always apply retrospectively. While the slab table gives the rate, your return filing result depends on how income is computed and which regime is finally selected.

Old regime vs new regime: what actually changes your tax?

The old regime and new regime are not just two slab tables. They are two different approaches to taxation. The old regime allows several deductions and exemptions, but the slab rates become steeper after ₹5 lakh. The new regime has comparatively lower rates and a wider nil slab, but many popular deductions and exemptions are not available or are restricted.

This is why a taxpayer should not decide based only on the headline slab. The correct approach is to calculate taxable income under both regimes and then compare final tax payable after rebate, surcharge and cess. A salaried employee should consider salary structure, standard deduction, HRA, employer NPS, professional tax, eligible deductions and Form 16 details. A freelancer should consider business income, eligible expenses, presumptive taxation possibilities and advance tax. An investor should consider capital gains separately because some capital gains are taxed at special rates and may not simply follow the slab table.

| Decision Point | Old Tax Regime | New Tax Regime |

|---|---|---|

| Deductions | Allows many eligible deductions such as 80C, 80D and certain other claims | Most traditional deductions are not available, with limited permitted benefits |

| HRA and LTA | May be available subject to conditions and documents | Generally not available in the same way |

| Standard deduction for salaried taxpayers | Generally ₹50,000 for eligible salary or pension income | Generally ₹75,000 for eligible salary or pension income for FY 2024-25 |

| Best suited for | Taxpayers with strong eligible deductions and exemptions | Taxpayers with simple income and fewer deductions |

| Compliance need | More documents required to support claims | Simpler for many taxpayers, but income disclosure still matters |

Unsure which regime works for you? WealthSure can compare your old and new regime tax position, review your income sources and help you file accurately.

Explore personal tax planningHow Section 87A rebate affects AY 2025-26 tax slabs

Section 87A rebate is one of the biggest reasons taxpayers misread the slab table. A slab rate tells you how tax is calculated at different income levels. Rebate can reduce the final tax for eligible resident individuals if total income is within the specified limit. For AY 2025-26, the rebate threshold is generally up to ₹5 lakh under the old regime and up to ₹7 lakh under the new regime, subject to applicable rules and conditions.

This means a person may technically have tax calculated under slab rates, but the rebate may reduce the payable tax to nil if the conditions are satisfied. However, this should not be confused with the basic exemption limit. Basic exemption and rebate are different concepts. The basic exemption limit is the income level up to which no tax is charged. Rebate is relief given after tax is computed, subject to eligibility.

Surcharge and cess for AY 2025-26

For most middle-income taxpayers, surcharge may not apply. However, high-income taxpayers should consider it carefully. Surcharge is an additional charge on income tax when total income crosses specified thresholds. Health and education cess at 4% is generally applied on tax plus surcharge. The applicable surcharge rate can differ depending on income level, regime and nature of income.

High-income taxpayers should not rely only on a simple slab table because surcharge, marginal relief, special-rate income and deduction limits can change the final result. For example, a person with salary income, capital gains and dividend income may have part of the income taxed under slab rates and part under special provisions. A simplified online estimate can be helpful, but a full computation is safer when the amount is significant.

If your income is near a surcharge threshold or includes capital gains, ESOPs, foreign assets, property sale, professional receipts or business income, consider asking a tax expert before filing. This is not about over-complicating the return. It is about avoiding mismatch, underpayment, incorrect regime selection and unnecessary follow-up with the tax department.

Practical examples: how AY 2025-26 slabs work in real life

Example 1: Salaried employee with limited deductions

Situation: Riya earns salary income of ₹8.20 lakh for FY 2024-25. She has limited deductions other than standard deduction and provident fund contribution. She wants to know whether the income tax slab for AY 2025-26 makes the new regime better.

Common confusion: She compares only the 20% old regime slab with the 10% new regime slab and assumes the new regime is automatically better. That may be true in many low-deduction cases, but the right method is to compute taxable income under both regimes.

Correct approach: Riya should check Form 16, salary breakup, eligible deductions and final taxable income. Under the new regime, the higher standard deduction can help salaried taxpayers, but she still needs to disclose bank interest, previous employer income and other income. Expert review can help her avoid missing smaller taxable items that may appear in AIS later.

Example 2: High-deduction salaried taxpayer

Situation: Arjun earns ₹14 lakh and pays rent, contributes to EPF, invests in eligible 80C instruments, has medical insurance and pays home loan interest on a self-occupied property. He searches for AY 2025-26 tax slabs and initially prefers the new regime because the slab table looks cleaner.

Common confusion: He ignores the value of HRA, 80C, 80D and home loan interest. Under the old regime, these can reduce taxable income if all conditions and documentation are satisfied.

Correct approach: Arjun should prepare both calculations. If the deductions and exemptions are significant, the old regime may still be worth evaluating. WealthSure’s tax optimizer service can help compare both regimes and identify eligible deductions without making unsupported claims.

Example 3: Freelancer with professional receipts

Situation: Mehul is a freelance designer with professional receipts, TDS from clients and some business expenses. He checks the income tax slab for AY 2025-26 and thinks he can apply the same logic as a salaried employee.

Common confusion: He ignores professional income reporting, expense documentation, presumptive taxation eligibility and advance tax. Slab rates matter, but they are only the final layer after income is correctly computed.

Correct approach: Mehul should first determine gross receipts, allowable expenses, TDS, advance tax and correct return form. A freelancer may also need to consider GST records, books of account and business/professional reporting. WealthSure’s business and professional ITR filing support can help align computation with filing requirements.

Example 4: Investor with capital gains

Situation: Kavita has salary income plus capital gains from equity mutual funds and listed shares. She compares the slab table and assumes all income will be taxed in the same way.

Common confusion: Capital gains may be taxed under special provisions depending on asset type, holding period and applicable law. Not every income item simply follows the slab table.

Correct approach: Kavita should download broker and mutual fund capital gains statements, compare them with AIS, and report the correct details in the appropriate schedule. WealthSure’s capital gains tax support can help review entries before filing.

Step-by-step method to choose the right tax regime

The right tax regime is not decided by age, job title or a social media table. It is decided by your numbers. Use this practical sequence before filing your return for AY 2025-26.

- List all income sources: Salary, business income, professional income, rent, interest, dividends, capital gains and any other taxable income.

- Separate special-rate income: Check whether capital gains or other income items are taxed separately from normal slab rates.

- Prepare old regime deductions: Include eligible 80C, 80D, HRA, home loan interest, NPS and other permitted claims with documents.

- Prepare new regime calculation: Apply the new regime benefits that are actually allowed for your case.

- Check rebate eligibility: Do not confuse the rebate threshold with the basic exemption limit.

- Add cess and surcharge where applicable: This is essential for higher income levels.

- Compare final tax payable: Look at the full computation, not only the slab table.

- Review ITR form and filing rules: Business taxpayers and certain taxpayers with special income need extra care.

Common mistakes while using AY 2025-26 income tax slabs

Tax slab mistakes often look small at first, but they can cause incorrect tax payable, refund mismatch, revised return requirements or tax notices. Here are common errors to avoid.

- Using FY 2025-26 slabs for AY 2025-26: AY 2025-26 relates to FY 2024-25 income. Do not mix it with later year changes.

- Assuming rebate means no filing requirement: Rebate may reduce tax, but filing requirement depends on separate rules and facts.

- Ignoring other income: Bank interest, FD interest, dividends, rent and capital gains must be reviewed.

- Choosing the default regime without comparison: Default does not always mean best.

- Claiming old regime deductions without proof: Keep valid documents for HRA, insurance, investments and loan interest.

- Missing AIS and Form 26AS mismatch: Compare tax credits and reported income before filing.

- Applying slab rates to capital gains blindly: Some capital gains have specific tax treatment.

- Not checking advance tax: Freelancers, investors and taxpayers with non-salary income may need advance tax planning.

For return filing support, you can explore WealthSure’s expert-assisted tax filing. If you have a simple salary case and want to start quickly, you may also review WealthSure’s free income tax filing option.

Documents to keep ready before comparing tax slabs

A good tax comparison starts with the right documents. Without documents, the comparison becomes a guess. Keep these records ready before deciding your tax regime for AY 2025-26.

| Document or Record | Why It Matters | Relevant For |

|---|---|---|

| Form 16 | Shows salary, TDS, deductions considered by employer and tax regime details | Salaried taxpayers |

| AIS and Form 26AS | Helps match reported income, TDS, TCS and tax payments | All taxpayers |

| Investment proofs | Needed for old regime deduction claims | Taxpayers claiming 80C, NPS or similar deductions |

| Health insurance premium proof | Useful for eligible 80D claims under the old regime | Individuals and families |

| Rent receipts and landlord details | Needed for HRA claim where applicable | Salaried taxpayers in rented accommodation |

| Capital gains statements | Required for reporting gains from shares, mutual funds or property | Investors |

| Professional receipts and expenses | Needed to compute business or professional income | Freelancers and professionals |

If your employer has issued Form 16 and you want expert help, WealthSure lets you upload your Form 16 for guided support. For taxpayers with business or presumptive income, review whether ITR-4 presumptive income filing or detailed professional income filing is appropriate.

How AY 2025-26 slabs affect salaried taxpayers

Salaried taxpayers should not stop at the salary figure. They should check gross salary, exemptions, deductions, perquisites, Form 16, standard deduction and any income from previous employment. The new regime may be attractive for employees with limited deductions, while the old regime can be useful when HRA, 80C, 80D, NPS and home loan benefits are substantial.

Salary restructuring can also matter. For example, a taxpayer may need to evaluate employer NPS contribution, reimbursements, allowances and benefits that are structured differently under the two regimes. However, restructuring should always be practical and compliant. It should not be done only for a theoretical tax result. WealthSure’s salary restructuring for tax saving service can help employees understand possibilities without making aggressive or unsupported claims.

How AY 2025-26 slabs affect freelancers and professionals

Freelancers, consultants, doctors, designers, software professionals, creators and independent professionals often search for tax slab rates but overlook income computation. Unlike a salaried employee, they may need to determine gross receipts, eligible expenses, TDS, advance tax, GST records, books of account and the correct ITR form. Slab rates apply after income is computed correctly.

For many professionals, advance tax is another important area. If tax liability after TDS is significant, advance tax rules may apply. Missing advance tax can create interest liability. WealthSure’s advance tax calculation support can help freelancers and professionals estimate periodic tax outflow more accurately.

How AY 2025-26 slabs affect NRIs and foreign income cases

NRIs and returning Indians should not use a slab table without checking residential status and income scope. The taxability of Indian income, foreign income, foreign assets and DTAA relief depends on facts. A person who worked abroad for part of the year may have a different tax position from someone who remained resident in India throughout the year.

Before applying the income tax slab for AY 2025-26, an NRI taxpayer should review residential status, Indian salary or business income, rent from Indian property, capital gains from Indian assets, TDS, DTAA eligibility and reporting obligations. WealthSure offers NRI tax filing service, residential status determination and DTAA advisory support for such cases.

Where to verify official tax information

Tax content should always be checked against official sources before filing. The Income Tax e-Filing portal is the official platform for return filing, forms, utilities, e-verification and taxpayer services. The Income Tax Department of India website provides tax information, acts, rules, circulars and taxpayer resources.

For investment and capital market related regulatory awareness, taxpayers may refer to the Securities and Exchange Board of India. For banking and financial system information, the Reserve Bank of India is an important official source. Broader government services can also be accessed through the National Portal of India.

AY 2025-26 tax planning checklist

Use this checklist before you file your return or finalise your tax regime selection.

- Confirm that you are using the correct assessment year: AY 2025-26 for FY 2024-25 income.

- Prepare both old and new regime computations.

- Review Form 16, AIS, TIS and Form 26AS before filing.

- Include interest income, dividend income, rent and capital gains where applicable.

- Keep documents for deductions claimed under the old regime.

- Check whether rebate under Section 87A applies to your case.

- Check surcharge and cess if income is high.

- Verify bank account details for refund processing.

- Choose the correct ITR form based on income type.

- E-verify the return within the applicable timeline after filing.

Want a safer tax filing experience? WealthSure can help with regime comparison, document review, ITR form selection, AIS/Form 26AS checks and accurate filing support.

Explore assisted filing supportFAQs on income tax slab for AY 2025-26

1. What is the income tax slab for AY 2025-26 under the new tax regime?

For AY 2025-26, the new tax regime generally uses progressive slab rates for individual taxpayers. The broad slab structure is nil tax up to ₹3 lakh, 5% from ₹3 lakh to ₹7 lakh, 10% from ₹7 lakh to ₹10 lakh, 15% from ₹10 lakh to ₹12 lakh, 20% from ₹12 lakh to ₹15 lakh and 30% above ₹15 lakh. Health and education cess at 4% is generally added on income tax plus surcharge, where applicable. The new regime is the default regime for eligible taxpayers, so it may automatically apply unless the taxpayer opts for the old regime as per applicable rules.

However, the slab table is only the starting point. Your final tax depends on total income, permitted deductions, standard deduction, rebate eligibility, surcharge, residential status and special income such as capital gains. For example, an employee with salary income may benefit from the standard deduction, while an investor may also need to report capital gains separately. WealthSure can help you compare calculations before filing so that you do not choose a regime based only on a headline slab table.

2. What is the old tax regime slab for AY 2025-26?

For individuals below 60 years of age, the old tax regime for AY 2025-26 generally has nil tax up to ₹2.5 lakh, 5% from ₹2.5 lakh to ₹5 lakh, 20% from ₹5 lakh to ₹10 lakh and 30% above ₹10 lakh. Senior citizens and super senior citizens have higher basic exemption limits under the old regime. The old regime also allows several eligible deductions and exemptions, such as certain deductions under Chapter VI-A, HRA where conditions are satisfied, home loan interest in eligible cases and other claims subject to law and documentation.

The old regime can be useful for taxpayers who have meaningful deductions and exemptions. For example, a salaried employee paying rent, contributing to provident fund, paying life insurance premium and having health insurance may need to compare the old regime carefully. But deductions should never be claimed casually. You should retain proofs and check whether each claim is valid for the relevant assessment year. WealthSure’s personal tax planning support can help you evaluate whether the old regime still makes sense for your facts.

3. Is the new tax regime the default regime for AY 2025-26?

Yes, the new tax regime is generally the default regime for eligible individual taxpayers for AY 2025-26. This means the return filing flow and tax computation may proceed under the new regime unless the taxpayer chooses the old regime according to the applicable process. This default status does not mean the new regime is always better. It simply means taxpayers should actively compare both options before filing if they have deductions or exemptions that may be valuable under the old regime.

For salaried taxpayers, the employer’s TDS regime selection during the year may not always be the final answer for return filing. A taxpayer should review the final return computation before submission. For business or professional income taxpayers, regime switching can involve additional rules and restrictions, so the choice should be made carefully. If you are not sure whether you can choose or switch regimes in your case, expert guidance is useful. WealthSure can review your income type, return form and regime choice before filing to reduce avoidable errors.

4. Which is better for AY 2025-26: old tax regime or new tax regime?

There is no single answer that works for everyone. The new regime may be better for taxpayers with fewer deductions, simple salary income and limited tax-saving investments. The old regime may be better for taxpayers with significant eligible deductions and exemptions such as 80C investments, HRA, health insurance premium, home loan interest and certain other permitted claims. The right choice depends on final tax payable, not only on the slab rate.

A practical method is to calculate taxable income under both regimes. Under the old regime, list every eligible deduction and exemption with supporting documents. Under the new regime, apply the allowed benefits and revised slab rates. Then compare final tax after rebate, surcharge and cess. This comparison is especially important for taxpayers earning between ₹7 lakh and ₹20 lakh because deductions can change the outcome materially. WealthSure’s tax optimizer and personal tax planning services can help you compare both regimes in a structured way without overclaiming or missing taxable income.

5. Does Section 87A rebate apply to income tax slab for AY 2025-26?

Section 87A rebate may apply to eligible resident individuals if their total income is within the prescribed limit. For AY 2025-26, the broad understanding is that rebate may reduce tax for eligible resident individuals with total income up to ₹5 lakh under the old regime and up to ₹7 lakh under the new regime, subject to applicable conditions. This is why some taxpayers see nil final tax even though a slab rate technically applies to a portion of income.

It is important to understand that rebate is not the same as exemption. The slab table computes tax first, and rebate may reduce eligible tax after that. Also, the taxpayer’s residential status, income level and nature of income can affect the final position. Rebate may not solve filing obligations, and it does not mean income can be ignored. If your income is near the rebate threshold, review salary, interest, dividend and capital gains carefully. Even a small additional income item can affect the final computation. WealthSure can help review such cases before submission.

6. How does standard deduction work for AY 2025-26?

Standard deduction is a deduction available to eligible salaried taxpayers and pensioners. For FY 2024-25 relevant to AY 2025-26, the standard deduction under the new regime is generally ₹75,000 for eligible salary or pension income, while the old regime generally provides ₹50,000. This difference can make the new regime more attractive for many salaried taxpayers with limited deductions. However, standard deduction alone should not decide the regime.

A salaried taxpayer should check Form 16, salary breakup, other income, deductions, employer NPS contribution and regime-specific rules. For someone with high HRA and other eligible old regime deductions, the old regime may still need to be compared. For someone with low deductions and straightforward salary income, the new regime may produce a simpler result. Do not assume the employer’s payroll calculation is enough for final ITR filing. Before filing, compare the full computation and check AIS and Form 26AS for additional income or TDS details. WealthSure can assist with Form 16-based review and return filing.

7. Do senior citizens have different income tax slabs for AY 2025-26?

Under the old tax regime, senior citizens and super senior citizens generally have higher basic exemption limits compared with individuals below 60 years. A senior citizen, usually aged 60 years or more but below 80 years, has a higher basic exemption limit under the old regime. A super senior citizen, usually aged 80 years or more, has an even higher basic exemption limit under the old regime. However, the new tax regime slabs are generally uniform for individuals, subject to applicable provisions.

Senior citizens should not evaluate slab rates alone. Interest income, pension income, medical insurance, deductions, TDS, Form 26AS, bank deposits and eligible reliefs can all affect the final tax position. Retirees should also consider cash flow, documentation and whether the old regime deductions are actually available in their case. If there are capital gains, rental income or foreign pension issues, the computation can become more detailed. WealthSure can help senior taxpayers and families compare both regimes and file with proper documentation.

8. Are capital gains taxed according to the AY 2025-26 slab?

Not always. Some capital gains are taxed at special rates depending on the asset type, holding period and applicable provisions. For example, equity shares, equity mutual funds, debt funds, property, unlisted shares and foreign assets may have different tax treatment. Normal slab rates are relevant for ordinary income, but capital gains require separate classification and reporting. This is why investors should not apply the income tax slab for AY 2025-26 mechanically to all gains.

If you sold shares, mutual funds, property or other capital assets during FY 2024-25, download capital gains statements and compare them with AIS. Also check whether the gain is short-term or long-term, whether indexation rules apply where relevant, and whether special schedules are required in the ITR. Reporting errors can lead to mismatch or notice risk. WealthSure’s capital gains tax support can help investors review transactions, classify gains and file the correct return more confidently.

9. Can freelancers use the same income tax slab for AY 2025-26?

Freelancers and professionals may be taxed using the applicable slab rates after their income is correctly computed. However, their calculation is not as simple as reading the slab table. A freelancer must first determine professional receipts, eligible business expenses, TDS deducted by clients, advance tax paid and the applicable return form. Some professionals may evaluate presumptive taxation if eligible, while others may need detailed books and expense reporting.

The new versus old regime comparison can also work differently for freelancers because salary-related benefits, employer deductions and certain exemptions may not apply in the same way. If a freelancer has irregular income, multiple clients, foreign receipts, GST registration or capital gains, the computation should be reviewed carefully. Slab rates tell you the tax rate after taxable income is determined; they do not decide what your taxable income is. WealthSure’s professional income filing support can help freelancers calculate income, reconcile TDS, consider advance tax and file the correct ITR.

10. How can WealthSure help with AY 2025-26 tax slab and ITR filing?

WealthSure can help taxpayers move beyond a basic slab-table understanding and build a more accurate tax filing approach. The process may include reviewing salary details, Form 16, AIS, Form 26AS, deductions, capital gains, business or professional income, NRI status and return form selection. The aim is to help you file accurately, choose the right regime where applicable and avoid common errors such as missing income, unsupported deductions, incorrect tax credits or failure to e-verify.

For simple cases, self-service filing may be enough if the taxpayer understands the data and documents. For complex cases, expert-assisted support is safer. This includes salaried taxpayers with multiple employers, freelancers, investors with capital gains, NRIs, taxpayers with notices, and anyone uncertain about old versus new regime comparison. WealthSure offers tax filing, personal tax planning, revised or updated return filing, notice response, capital gains tax support and NRI tax filing services. The advice is tailored to your facts and does not rely on generic assumptions or guaranteed outcomes.

Conclusion: use AY 2025-26 slabs as a planning tool, not just a rate chart

The income tax slab for AY 2025-26 helps you understand the rate at which your income may be taxed, but it does not answer every filing question. The final tax result depends on the tax regime you choose, your income sources, deduction eligibility, documentation, rebate, surcharge, cess and the correct reporting of special income such as capital gains or professional receipts.

Self-service tools may be enough if your income is simple, documents are clear and you understand the return filing process. Expert-assisted support becomes more valuable when you have multiple employers, deductions, capital gains, freelance income, NRI status, business income, advance tax, notice history or uncertainty about old versus new regime. Proactive tax planning also connects with long-term financial growth because tax efficiency, compliance and investment decisions often work together.

Ready to file with confidence? Compare your tax regime, review documents and complete your AY 2025-26 ITR with WealthSure’s guided tax support.

Start Income Tax Return filing onlineAt WealthSure, we don’t just file taxes — we simplify your financial journey and help you build long-term wealth with confidence.