Income Tax Slab for AY 2026-27: Old vs New Regime Guide

The income tax slab for AY 2026-27 is one of the most important tax-planning references for Indian taxpayers because it affects salary planning, tax regime selection, ITR filing, take-home income, advance tax and year-end financial decisions. AY 2026-27 relates to income earned during FY 2025-26, and your final tax depends on whether you use the new tax regime or the old tax regime.

Most taxpayers do not search for tax slabs only to see a table. They want to know how much tax they may pay, whether income up to ₹12 lakh is really tax-free, whether ₹12.75 lakh salary can result in nil tax, how Section 87A rebate works, and whether deductions under the old regime are still useful. This guide answers those questions in a practical and compliance-focused way.

At WealthSure, we believe tax planning should not be limited to last-minute return filing. A good tax decision should help you stay compliant, avoid unnecessary tax outflow, plan investments intelligently and reduce the risk of incorrect claims or notices. This article is designed for salaried individuals, first-time filers, freelancers, consultants, investors, senior citizens, NRIs, business owners and professionals who want clarity before filing their ITR for AY 2026-27.

Tax rules, return utilities and filing requirements may change. Always verify the latest information on the official Income Tax Department e-Filing portal before filing. If your case includes capital gains, business income, professional receipts, crypto, foreign income, NRI taxation, high-value transactions or tax notices, consider expert support before final submission.

Table of Contents

- Quick answer: income tax slab for AY 2026-27

- AY 2026-27 vs FY 2025-26

- New tax regime slab for AY 2026-27

- Old tax regime slab for AY 2026-27

- Senior citizen and super senior citizen slabs

- Section 87A rebate for AY 2026-27

- Standard deduction and salary impact

- Old vs new tax regime: which one should you choose?

- Tax calculation examples

- Surcharge, cess and marginal relief

- How slabs affect different taxpayer profiles

- Common tax slab mistakes to avoid

- AY 2026-27 tax planning checklist

- FAQs on income tax slab for AY 2026-27

Quick Answer: Income Tax Slab for AY 2026-27

For AY 2026-27, individuals generally compare the new tax regime under Section 115BAC with the old tax regime. The new tax regime is the default regime and offers lower slab rates, broader slabs and a higher rebate threshold. The old regime allows several deductions and exemptions but has higher slab rates in many cases.

| Regime | Best Understood As | Key Benefit | Key Limitation |

|---|---|---|---|

| New Tax Regime | Lower-rate, simplified regime | Wider slabs and rebate-linked nil tax up to eligible taxable income of ₹12 lakh | Most old-regime deductions and exemptions are not available |

| Old Tax Regime | Deduction-led regime | Useful if you claim substantial deductions and exemptions | Higher slab rates and more documentation |

Important: A slab rate applies only to the income falling within that slab. Your entire income is not taxed at the highest slab rate. This is why slab-based tax must be calculated layer by layer.

AY 2026-27 vs FY 2025-26: What Is the Difference?

Financial Year 2025-26 is the year in which you earn income. It runs from 1 April 2025 to 31 March 2026. Assessment Year 2026-27 is the year in which that income is assessed and the income tax return is filed.

| Term | Period | Meaning |

|---|---|---|

| FY 2025-26 | 1 April 2025 to 31 March 2026 | The year in which income is earned |

| AY 2026-27 | 1 April 2026 to 31 March 2027 | The year in which income is assessed and return is filed |

This distinction is important because taxpayers often use “FY 2025-26 tax slab” and “AY 2026-27 tax slab” interchangeably. They are connected, but the return for income earned in FY 2025-26 is filed for AY 2026-27.

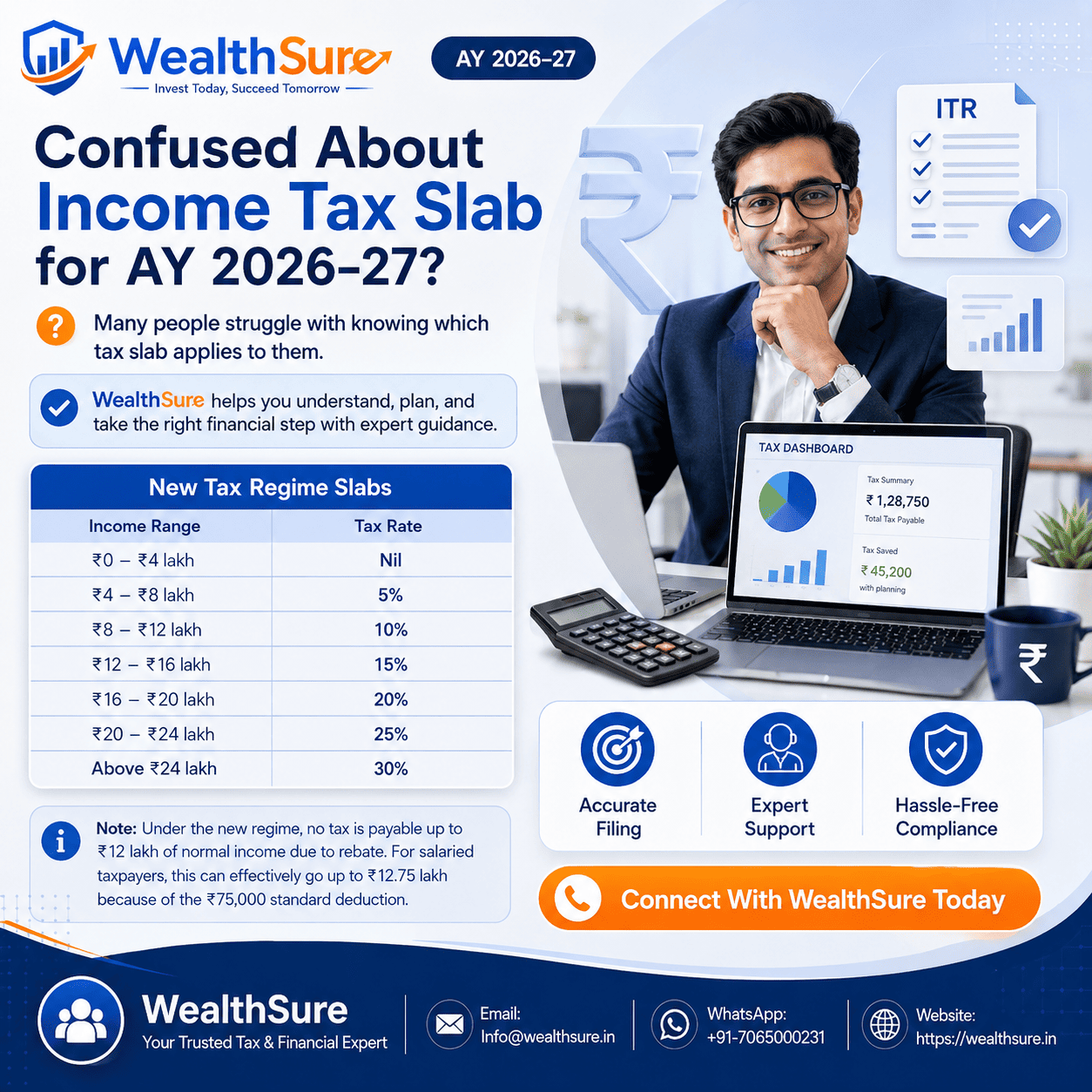

New Tax Regime Slab for AY 2026-27

The new tax regime is the default option for eligible taxpayers. It is designed to simplify taxation with wider slabs and fewer deductions. For AY 2026-27, the new tax regime slabs are:

| Taxable Income Slab | Income Tax Rate | Tax Calculation Logic |

|---|---|---|

| Up to ₹4,00,000 | Nil | No tax on this income layer |

| ₹4,00,001 to ₹8,00,000 | 5% | 5% on income above ₹4,00,000 |

| ₹8,00,001 to ₹12,00,000 | 10% | ₹20,000 plus 10% on income above ₹8,00,000 |

| ₹12,00,001 to ₹16,00,000 | 15% | ₹60,000 plus 15% on income above ₹12,00,000 |

| ₹16,00,001 to ₹20,00,000 | 20% | ₹1,20,000 plus 20% on income above ₹16,00,000 |

| ₹20,00,001 to ₹24,00,000 | 25% | ₹2,00,000 plus 25% on income above ₹20,00,000 |

| Above ₹24,00,000 | 30% | ₹3,00,000 plus 30% on income above ₹24,00,000 |

Visual Snapshot: New Regime Slab Flow

The new regime may be suitable for taxpayers who do not claim many deductions, prefer a simpler tax calculation, or do not want to make investments only for tax-saving purposes. However, it is not automatically best for everyone.

Old Tax Regime Slab for AY 2026-27

The old tax regime continues to be relevant because it allows several deductions and exemptions. If you have eligible HRA, Section 80C investments, health insurance premium, home loan interest, NPS contributions or other deductions, you should compare both regimes.

| Taxable Income Slab | Income Tax Rate | Tax Calculation Logic |

|---|---|---|

| Up to ₹2,50,000 | Nil | No tax on this income layer |

| ₹2,50,001 to ₹5,00,000 | 5% | 5% on income above ₹2,50,000 |

| ₹5,00,001 to ₹10,00,000 | 20% | ₹12,500 plus 20% on income above ₹5,00,000 |

| Above ₹10,00,000 | 30% | ₹1,12,500 plus 30% on income above ₹10,00,000 |

Useful When Simplicity Matters

The new regime may work well if your deductions are limited and you want a cleaner tax calculation with lower slab rates.

Useful When Deductions Are Strong

The old regime may work better if your eligible deductions and exemptions reduce taxable income enough to offset higher slab rates.

Senior Citizen and Super Senior Citizen Slabs

Under the old regime, resident senior citizens and super senior citizens get higher basic exemption limits. Under the new regime, the slab structure is generally uniform for individuals, subject to applicable rules.

Old Regime Slab for Resident Senior Citizens

| Taxable Income Slab | Income Tax Rate |

|---|---|

| Up to ₹3,00,000 | Nil |

| ₹3,00,001 to ₹5,00,000 | 5% on income above ₹3,00,000 |

| ₹5,00,001 to ₹10,00,000 | ₹10,000 plus 20% on income above ₹5,00,000 |

| Above ₹10,00,000 | ₹1,10,000 plus 30% on income above ₹10,00,000 |

Old Regime Slab for Resident Super Senior Citizens

| Taxable Income Slab | Income Tax Rate |

|---|---|

| Up to ₹5,00,000 | Nil |

| ₹5,00,001 to ₹10,00,000 | 20% on income above ₹5,00,000 |

| Above ₹10,00,000 | ₹1,00,000 plus 30% on income above ₹10,00,000 |

NRI note: Non-resident taxpayers should review residential status, DTAA, TDS, capital gains and eligibility conditions carefully. Old-regime age-based benefits may not apply in the same way to non-residents.

Section 87A Rebate for AY 2026-27

Section 87A rebate is a key reason why the new regime is attractive for many middle-income taxpayers. But rebate is often misunderstood. A slab is not the same as rebate. The slab calculates tax; the rebate reduces eligible tax payable after calculation, subject to conditions.

| Regime | Rebate Limit | Broad Condition | Practical Meaning |

|---|---|---|---|

| New Tax Regime | Up to ₹60,000 | Taxable income up to ₹12,00,000, subject to conditions | Can result in nil tax for eligible taxpayers up to the threshold |

| Old Tax Regime | Up to ₹12,500 | Taxable income up to ₹5,00,000, subject to conditions | Can result in nil tax for eligible taxpayers up to the threshold |

The ₹12 lakh discussion should be handled carefully. It generally refers to eligible taxable income under the new regime. It does not automatically mean that every type of income up to ₹12 lakh is tax-free in every situation. Special-rate income, such as certain capital gains, may require separate treatment.

Standard Deduction and Salary Impact

For eligible salaried taxpayers and pensioners, standard deduction can reduce taxable salary income. Under the new regime, a salaried taxpayer with gross salary up to ₹12.75 lakh may reach taxable income of ₹12 lakh after the ₹75,000 standard deduction and may then qualify for rebate, subject to conditions.

| Particulars | Amount | Tax Impact |

|---|---|---|

| Gross salary | ₹12,75,000 | Salary before standard deduction |

| Less: Standard deduction | ₹75,000 | Reduces taxable salary income |

| Taxable income | ₹12,00,000 | May be eligible for Section 87A rebate |

| Possible final tax | Nil | Subject to income composition and eligibility conditions |

Confused between gross salary, taxable income and rebate? WealthSure can help compare both regimes, review Form 16, estimate tax payable and file your ITR accurately.

Ask a WealthSure tax expertOld vs New Tax Regime for AY 2026-27: Which One Should You Choose?

The better regime depends on your numbers. A taxpayer with limited deductions may benefit from the new regime. A taxpayer with high HRA, home loan interest, Section 80C investments, NPS and health insurance may still need to compare the old regime carefully.

| Situation | Regime That May Need Closer Review | Reason |

|---|---|---|

| Simple salary and limited deductions | New regime | Lower rates and rebate may be beneficial |

| High HRA and Section 80C investments | Old regime | Deductions may reduce taxable income significantly |

| Home loan interest benefit | Old regime | Old-regime house property benefits may matter |

| Freelance or professional income | Both regimes | Expense claims, presumptive taxation and advance tax must be reviewed |

| Capital gains or ESOPs | Both regimes | Special-rate income can change the expected outcome |

| NRI income in India | Both regimes with expert review | Residential status, DTAA and TDS may affect final tax |

Decision-tree approach

Add income from salary, business, profession, house property, capital gains and other sources.

List old-regime deductions and exemptions with valid proof.

Calculate tax under both regimes, including rebate, cess, surcharge and special-rate income.

Choose the option that is tax-efficient, compliant and supported by documentation.

Business and professional income note: Taxpayers with business or professional income should carefully review regime-switching rules and Form 10-IEA requirements. Do not treat regime selection casually if you have business or professional receipts.

Tax Calculation Examples for AY 2026-27

Example 1: Salaried taxpayer with ₹12.75 lakh gross salary under new regime

| Particulars | Amount | Explanation |

|---|---|---|

| Gross salary | ₹12,75,000 | Salary before standard deduction |

| Standard deduction | ₹75,000 | Available to eligible salaried taxpayers |

| Taxable income | ₹12,00,000 | Falls within rebate-linked threshold |

| Tax before rebate | ₹60,000 | Calculated using new-regime slabs |

| Section 87A rebate | Up to ₹60,000 | May reduce eligible tax to nil |

Example 2: Taxable income of ₹15 lakh under new regime

| Income Layer | Rate | Tax |

|---|---|---|

| Up to ₹4,00,000 | Nil | ₹0 |

| ₹4,00,001 to ₹8,00,000 | 5% | ₹20,000 |

| ₹8,00,001 to ₹12,00,000 | 10% | ₹40,000 |

| ₹12,00,001 to ₹15,00,000 | 15% | ₹45,000 |

| Total tax before cess | - | ₹1,05,000 |

| Health and education cess | 4% | ₹4,200 |

| Approximate tax payable | - | ₹1,09,200 |

This example shows why crossing the ₹12 lakh threshold does not mean the entire income is taxed at 15%. Only the relevant income layer is taxed at the applicable slab rate.

Example 3: Old regime may still work for a deduction-heavy taxpayer

Suppose a taxpayer has gross income of ₹14 lakh and strong old-regime deductions such as Section 80C, HRA, health insurance and home loan interest. The old regime may deserve serious comparison if these deductions materially reduce taxable income. But if deductions are limited, the new regime may be simpler and more efficient.

Surcharge, Cess and Marginal Relief

Income tax slabs are only the base calculation. Depending on income level, taxpayers may also need to consider surcharge and health & education cess.

Health and education cess

Health and education cess is charged at 4% on income tax plus surcharge, where applicable. Even if the slab calculation is correct, missing cess can make the final tax number wrong.

Surcharge for high-income taxpayers

| Income Level | New Regime Surcharge | Old Regime Surcharge |

|---|---|---|

| Up to ₹50 lakh | Nil | Nil |

| Above ₹50 lakh to ₹1 crore | 10% | 10% |

| Above ₹1 crore to ₹2 crore | 15% | 15% |

| Above ₹2 crore to ₹5 crore | 25% | 25% |

| Above ₹5 crore | 25% | 37% |

Marginal relief may apply in eligible cases so that crossing a threshold does not create an excessive tax jump. High-income taxpayers, founders, senior executives, professionals and investors should calculate this carefully.

High income, bonus, ESOPs, capital gains or surcharge exposure? WealthSure can help estimate tax under both regimes, plan advance tax and file accurately.

Explore WealthSure ITR filing servicesHow AY 2026-27 Tax Slabs Affect Different Taxpayer Profiles

Salaried employees

Salaried taxpayers should compare both regimes before filing. If you changed jobs during FY 2025-26, make sure income from both employers is included. Do not rely only on one Form 16 if there were multiple employers.

Freelancers and consultants

Freelancers should consider professional receipts, expenses, TDS, advance tax and presumptive taxation where applicable. Regime selection must be aligned with the way income is reported.

Investors with capital gains

Investors should review capital gains statements carefully. Equity, mutual funds, property, ESOPs and crypto may involve special tax treatment. A headline rebate threshold should not be applied blindly to special-rate income.

Senior citizens and pensioners

Senior citizens should compare pension income, interest income, medical insurance, deductions and age-based old-regime slab benefits before choosing a regime.

NRIs

NRIs should evaluate residential status, Indian income, TDS, DTAA relief, capital gains and rental income before filing. NRI cases often need a more careful tax review.

Business owners and professionals

Business owners and professionals should consider profit computation, audit requirements, advance tax, TDS, GST linkage and regime-switching rules before filing.

Common Mistakes While Applying Income Tax Slabs for AY 2026-27

- Confusing gross salary with taxable income.

- Assuming the full income is taxed at the highest slab rate.

- Ignoring Section 87A rebate conditions.

- Assuming every income up to ₹12 lakh is automatically tax-free.

- Not checking capital gains or other special-rate income.

- Choosing the new regime without comparing old-regime deductions.

- Choosing the old regime only because investments were made, without calculating final tax.

- Forgetting health and education cess.

- Ignoring surcharge when income exceeds ₹50 lakh.

- Using the wrong assessment year slab.

- Not reviewing Form 16, AIS, TIS and Form 26AS before filing ITR.

- Missing Form 10-IEA considerations for business or professional income.

WealthSure Expert Tip

Do not make regime selection a last-minute ITR decision. Estimate your tax early, review it after bonus or income changes, compare both regimes and finalize before filing. This reduces avoidable tax outflow and compliance risk.

AY 2026-27 Tax Planning Checklist Before Filing ITR

| Checklist Item | Why It Matters | Status |

|---|---|---|

| Confirmed FY and AY correctly | Prevents filing for the wrong assessment year | Yes / No |

| Compared old and new tax regimes | Helps choose the lower compliant tax outcome | Yes / No |

| Checked salary from all employers | Avoids under-reporting income after job change | Yes / No |

| Reviewed Form 16, AIS, TIS and Form 26AS | Helps identify income and tax credit mismatches | Yes / No |

| Checked capital gains reports | Ensures special-rate income is reported correctly | Yes / No |

| Validated deductions with proof | Reduces risk of unsupported claims | Yes / No |

| Checked rebate eligibility | Prevents incorrect nil-tax assumptions | Yes / No |

| Added cess and surcharge where applicable | Ensures final tax computation is complete | Yes / No |

| Validated bank account for refund | Helps avoid refund delays | Yes / No |

When Should You Take Expert Help?

You may not need expert help for every simple tax case. But professional review becomes useful when your income has complexity, high value or reporting risk.

- Income from more than one employer.

- Salary plus freelance or consulting receipts.

- Capital gains from shares, mutual funds, ESOPs or property.

- Crypto or virtual digital asset income.

- Rental income or multiple house properties.

- NRI taxation or foreign income.

- Business or professional income.

- Advance tax liability.

- High income with surcharge exposure.

- Confusion between old and new tax regimes.

- Tax notice, mismatch or refund delay.

Need help choosing the right tax regime for AY 2026-27? WealthSure combines fintech-powered tax filing, expert advisory and practical tax planning to help you file accurately and make smarter financial decisions.

Get started with WealthSureFAQs on Income Tax Slab for AY 2026-27

1. What is the income tax slab for AY 2026-27?

The income tax slab for AY 2026-27 depends on whether you choose the new tax regime or the old tax regime. Under the new regime, income up to ₹4 lakh is nil-rated, followed by 5%, 10%, 15%, 20%, 25% and 30% slabs. Under the old regime, slab rates depend on age category.

2. AY 2026-27 is related to which financial year?

AY 2026-27 relates to FY 2025-26. Income earned from 1 April 2025 to 31 March 2026 is generally assessed and filed in Assessment Year 2026-27.

3. Is the new tax regime the default regime for AY 2026-27?

Yes, the new tax regime is the default regime for eligible taxpayers. If you want to use the old regime, you need to choose it as per applicable rules.

4. Is income up to ₹12 lakh fully tax-free for AY 2026-27?

Under the new regime, eligible taxable income up to ₹12 lakh may result in nil tax because of Section 87A rebate, subject to conditions. Special-rate income such as certain capital gains may need separate treatment.

5. Can salaried taxpayers pay zero tax up to ₹12.75 lakh salary?

An eligible salaried taxpayer under the new regime may have nil tax up to ₹12.75 lakh gross salary if the ₹75,000 standard deduction reduces taxable income to ₹12 lakh and the income qualifies for rebate.

6. What is the old tax regime slab for individuals below 60 years?

Under the old regime for individuals below 60 years, income up to ₹2.5 lakh is nil-rated, ₹2.5 lakh to ₹5 lakh is taxed at 5%, ₹5 lakh to ₹10 lakh at 20%, and income above ₹10 lakh at 30%, subject to rebate, cess and surcharge where applicable.

7. Which regime is better for salaried employees?

The better regime depends on salary structure, HRA, investments, deductions, home loan interest, NPS, health insurance and other income. Employees should compare both regimes before filing.

8. Does Section 80C apply under the new tax regime?

Most traditional deductions such as Section 80C are generally not available under the new regime in the same way as under the old regime. If you rely heavily on deductions, compare both regimes carefully.

9. Is cess applicable in AY 2026-27?

Yes. Health and education cess at 4% applies on income tax plus surcharge, where tax is payable.

10. How can WealthSure help?

WealthSure can help with regime comparison, ITR form selection, salary and Form 16 review, AIS/Form 26AS checking, capital gains reporting, freelancer tax filing, NRI taxation, business ITR filing, advance tax calculation, revised returns, updated returns and notice response.

Conclusion

Understanding the income tax slab for AY 2026-27 is the first step toward accurate tax planning, but it is not the full answer. Your final tax depends on regime selection, taxable income, deductions, rebate eligibility, standard deduction, cess, surcharge, special-rate income and compliance rules.

The new tax regime offers lower slab rates and a strong rebate structure for eligible taxpayers. The old regime still matters for taxpayers who can claim substantial deductions and exemptions. The best approach is to calculate both, verify documents, review reported income and choose the regime that is tax-efficient and compliant.

File your AY 2026-27 ITR with confidence. WealthSure helps individuals, salaried professionals, freelancers, investors, NRIs and businesses simplify tax filing, tax planning and financial decisions with expert-led support.

Start your tax filing with WealthSureDisclaimer

This article is for general informational and educational purposes only. It does not constitute tax, legal, financial or investment advice. Income tax slabs, deductions, exemptions, rebate rules, surcharge, cess, filing forms and portal processes may change. Please verify the latest rules on the official Income Tax Department website or consult a qualified tax professional before filing your return or making tax decisions.