Income Tax Slab for FY 2024-25: Old vs New Tax Regime Guide

Understanding the income tax slab for FY 2024-25 is one of the most important steps before filing your income tax return for Assessment Year 2025-26. Whether you are salaried, self-employed, a freelancer, a consultant, an investor, an NRI with taxable Indian income, or a business owner, your tax outflow depends not only on your income level but also on the tax regime you choose, deductions you can claim, exemptions available to you, rebate eligibility, surcharge, cess and the accuracy of your final tax computation.

For FY 2024-25, taxpayers need to pay close attention to the difference between the new tax regime and the old tax regime. The new tax regime is the default regime for eligible taxpayers, but many taxpayers may still choose the old regime if their deductions, exemptions and tax-saving investments make it more beneficial. This is where many people make mistakes. They look only at slab rates and ignore the actual tax calculation after deductions, standard deduction, rebate, house rent allowance, home loan interest, insurance premium, NPS, education loan interest or other eligible claims.

This WealthSure guide explains the income tax slabs for FY 2024-25 in a practical, people-first manner. You will learn the slab rates under both regimes, who should compare the regimes carefully, how rebate under Section 87A works, how cess and surcharge affect tax payable, and how different taxpayer profiles should approach tax planning before filing ITR. The goal is not just to show a tax slab table. The goal is to help you understand what the slab means for your real financial life.

Tax rules and return filing instructions can change through Finance Acts, notifications, circulars and portal updates. Always verify the latest rules on the official Income Tax Department e-Filing portal before filing your return. If your income includes capital gains, business income, professional receipts, crypto or virtual digital assets, foreign income, foreign assets, NRI taxation, tax notice history or high-value transactions, consider expert review before submitting your ITR.

Quick Summary: Income Tax Slab for FY 2024-25

- The new tax regime is the default tax regime for eligible individual taxpayers.

- Eligible taxpayers can still choose the old tax regime if it gives a lower tax liability.

- Under the new regime, the basic nil-tax slab is up to ₹3 lakh for individuals.

- Under the old regime, slab limits differ for individuals below 60, senior citizens and super senior citizens.

- Resident individuals may get Section 87A rebate if their income is within the applicable threshold.

- Health and education cess at 4% applies on income tax plus surcharge, if any.

- Your best regime depends on your deductions, exemptions, income composition and filing profile.

Table of Contents

- What does income tax slab for FY 2024-25 mean?

- New tax regime slab for FY 2024-25

- Old tax regime slab for FY 2024-25

- Old vs new tax regime: key difference

- Section 87A rebate for FY 2024-25

- Cess and surcharge explained

- Tax calculation examples

- Which regime may suit different taxpayers?

- Common mistakes to avoid

- FY 2024-25 tax planning checklist

- FAQs on income tax slab for FY 2024-25

What does income tax slab for FY 2024-25 mean?

An income tax slab is a range of taxable income on which a particular tax rate applies. India follows a progressive slab system for individual taxpayers, which means that higher income ranges are taxed at higher rates. Importantly, the higher rate does not apply to your entire income. It applies only to the income that falls within that specific slab.

For example, if a slab says income from ₹3 lakh to ₹7 lakh is taxed at 5%, it does not mean the entire income is taxed at 5%. It means only the income portion falling between ₹3 lakh and ₹7 lakh is taxed at 5%, subject to rebate and other applicable rules. This is why many taxpayers misunderstand their actual tax liability when they look at slab tables quickly.

For FY 2024-25, the relevant return filing year is generally Assessment Year 2025-26. This means that income earned from 1 April 2024 to 31 March 2025 is reported in the ITR filed for AY 2025-26. While the slab rates help you estimate tax, the final tax payable depends on taxable income after considering salary components, deductions, exemptions, standard deduction, tax regime choice, rebate, surcharge, cess and tax credits such as TDS, TCS, advance tax and self-assessment tax.

WealthSure tip: Do not choose a tax regime only by looking at the first slab. Always compare the final tax payable under both regimes using your actual income, deductions and exemptions.

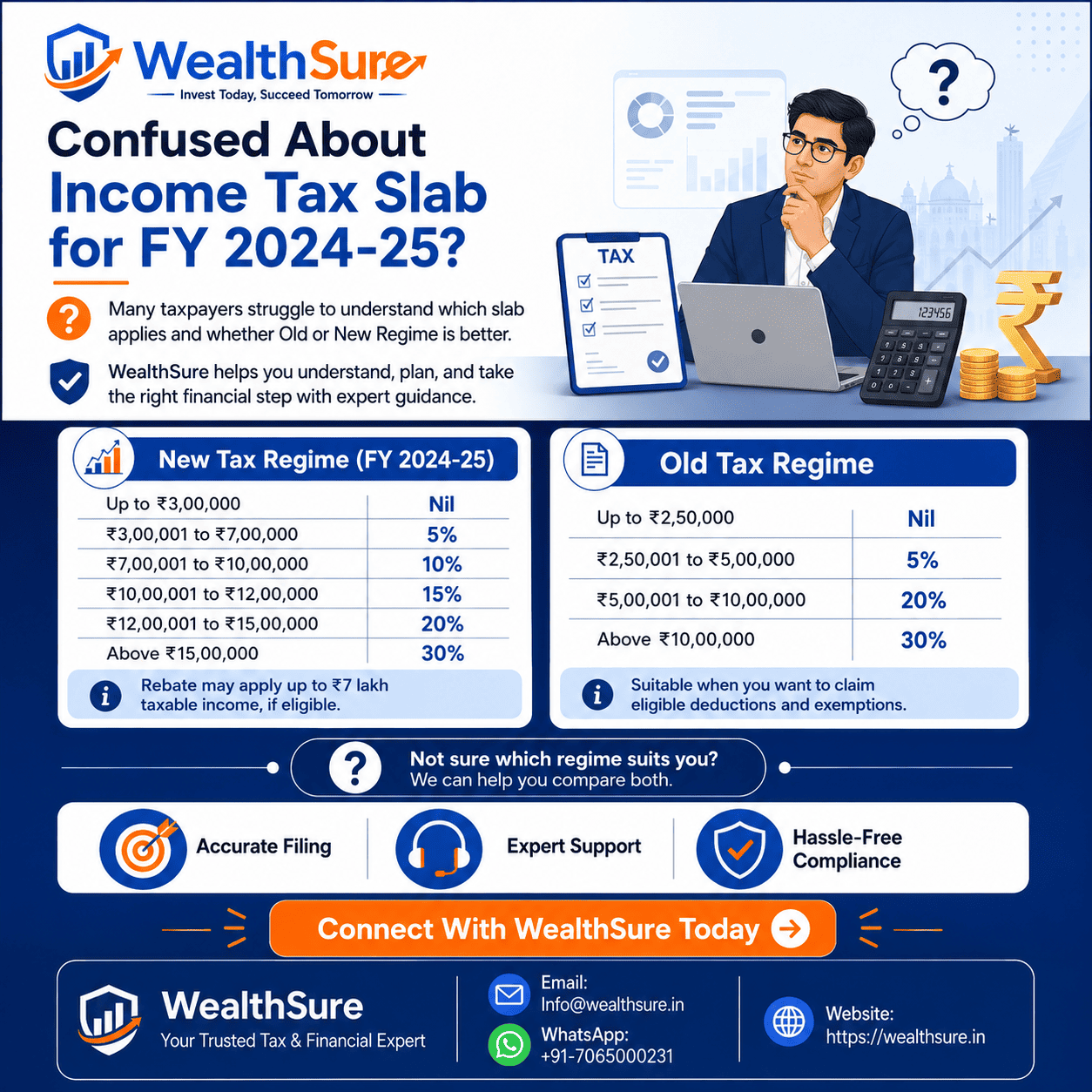

New Tax Regime Slab for FY 2024-25

The new tax regime under Section 115BAC is the default regime for eligible taxpayers. It offers lower and simpler slab rates compared with the old regime, but it generally restricts many deductions and exemptions that are available in the old regime. This makes it attractive for taxpayers who have fewer deductions or prefer a simplified tax structure.

For FY 2024-25, the new tax regime slabs for individuals are broadly as follows:

| Taxable Income Under New Tax Regime | Income Tax Rate | Simple Explanation |

|---|---|---|

| Up to ₹3,00,000 | Nil | No tax on this slab. |

| ₹3,00,001 to ₹7,00,000 | 5% | 5% applies only on income above ₹3 lakh within this range. |

| ₹7,00,001 to ₹10,00,000 | 10% | 10% applies on income above ₹7 lakh within this range. |

| ₹10,00,001 to ₹12,00,000 | 15% | 15% applies on income above ₹10 lakh within this range. |

| ₹12,00,001 to ₹15,00,000 | 20% | 20% applies on income above ₹12 lakh within this range. |

| Above ₹15,00,000 | 30% | 30% applies on income above ₹15 lakh. |

The new regime is often useful for taxpayers who do not claim many deductions under Section 80C, 80D, HRA, LTA, home loan interest, NPS or other old-regime benefits. It can also simplify tax planning because the taxpayer does not need to invest only for tax-saving purposes. However, simplified does not always mean cheaper. A taxpayer with significant eligible deductions may still pay less tax under the old regime.

Who may find the new tax regime useful?

- Salaried employees with limited deductions and exemptions.

- First-time taxpayers who prefer a simpler tax calculation.

- Young professionals who do not yet have large insurance, home loan or investment deductions.

- Taxpayers who want flexibility in investments instead of locking funds only for tax-saving purposes.

- Individuals whose final tax after rebate and standard deduction is lower under the new regime.

Important: The new regime may look easier, but taxpayers with HRA, home loan interest, Section 80C investments, health insurance premium, NPS contribution or education loan interest should still compare both regimes carefully.

Old Tax Regime Slab for FY 2024-25

The old tax regime is the traditional tax system where taxpayers can claim several deductions and exemptions, subject to conditions. Although the slab rates are higher than the new regime in many income ranges, the old regime may still be better if you have enough eligible deductions and exemptions.

The old regime is especially relevant for taxpayers who use tax-saving investments and expenses as part of their financial plan. This may include provident fund, life insurance premium, ELSS, children’s tuition fee, principal repayment on housing loan, health insurance premium, home loan interest, HRA, NPS and other eligible claims.

Old tax regime slab for individuals below 60 years

| Taxable Income Under Old Tax Regime | Income Tax Rate | Simple Explanation |

|---|---|---|

| Up to ₹2,50,000 | Nil | No tax on this slab. |

| ₹2,50,001 to ₹5,00,000 | 5% | 5% applies on income above ₹2.5 lakh within this range. |

| ₹5,00,001 to ₹10,00,000 | 20% | 20% applies on income above ₹5 lakh within this range. |

| Above ₹10,00,000 | 30% | 30% applies on income above ₹10 lakh. |

Old tax regime slab for senior citizens aged 60 years or more but below 80 years

| Taxable Income Under Old Tax Regime | Income Tax Rate | Simple Explanation |

|---|---|---|

| Up to ₹3,00,000 | Nil | No tax on this slab for eligible senior citizens. |

| ₹3,00,001 to ₹5,00,000 | 5% | 5% applies on income above ₹3 lakh within this range. |

| ₹5,00,001 to ₹10,00,000 | 20% | 20% applies on income above ₹5 lakh within this range. |

| Above ₹10,00,000 | 30% | 30% applies on income above ₹10 lakh. |

Old tax regime slab for super senior citizens aged 80 years or more

| Taxable Income Under Old Tax Regime | Income Tax Rate | Simple Explanation |

|---|---|---|

| Up to ₹5,00,000 | Nil | No tax on this slab for eligible super senior citizens. |

| ₹5,00,001 to ₹10,00,000 | 20% | 20% applies on income above ₹5 lakh within this range. |

| Above ₹10,00,000 | 30% | 30% applies on income above ₹10 lakh. |

Who may find the old tax regime useful?

- Taxpayers paying rent and claiming HRA exemption.

- Individuals with large Section 80C investments such as EPF, PPF, ELSS, life insurance premium or home loan principal repayment.

- Taxpayers paying health insurance premium eligible under Section 80D.

- Home loan borrowers claiming interest deduction under Section 24(b).

- Taxpayers contributing to NPS and claiming eligible deductions.

- Families that plan tax-saving investments as part of long-term wealth creation.

Not sure whether old or new regime is better? WealthSure can compare both regimes using your actual income, deductions, exemptions and tax credits before ITR filing.

Ask a WealthSure tax expertOld vs New Tax Regime for FY 2024-25: Key Difference

The biggest difference between the two regimes is not only the slab rate. The real difference is how taxable income is calculated. In the old regime, you may reduce taxable income by claiming eligible deductions and exemptions. In the new regime, rates are lower, but several deductions and exemptions are not available or are restricted.

Lower rates, fewer deductions

The new regime is designed for simplified taxation. It may work well if you have limited deductions, do not claim HRA, do not have large tax-saving investments, or prefer flexibility in your financial planning.

Higher rates, more deductions

The old regime may be better if you actively use deductions and exemptions such as Section 80C, HRA, Section 80D, home loan interest, NPS and other eligible tax-saving options.

| Point of Comparison | New Tax Regime | Old Tax Regime |

|---|---|---|

| Default regime | Yes, it is the default regime for eligible taxpayers. | No, eligible taxpayers need to opt for it. |

| Slab rates | Generally lower and spread across more slabs. | Generally higher after basic exemption limit. |

| Deductions | Many common deductions are restricted or unavailable. | Several deductions and exemptions may be claimed subject to conditions. |

| Best suited for | Taxpayers with fewer deductions and simpler income structure. | Taxpayers with HRA, home loan, insurance, NPS and tax-saving investments. |

| Planning approach | Focus on lower rates and flexible investment choices. | Focus on tax-saving documentation and eligible deductions. |

| Decision method | Calculate final tax after available benefits. | Calculate final tax after deductions and exemptions. |

A smart tax decision starts with a comparison, not a guess. A salaried person with ₹10 lakh gross salary and minimal deductions may prefer the new regime. Another salaried person with the same salary, HRA, EPF, ELSS, health insurance and home loan interest may find the old regime better. The slab table is only the starting point; the final computation decides the answer.

Section 87A Rebate for FY 2024-25

Section 87A rebate can reduce tax liability for eligible resident individuals whose total income does not exceed the applicable threshold. It is one of the most commonly misunderstood parts of tax calculation because taxpayers often confuse slab exemption with rebate.

A nil slab means income up to a certain level is not taxed. A rebate means tax may be calculated first, and then reduced if the taxpayer meets the rebate conditions. This distinction matters because rebate rules can depend on residential status, income type, special-rate income and tax regime.

| Tax Regime | Income Threshold for Resident Individual | Rebate Impact |

|---|---|---|

| Old tax regime | Up to ₹5,00,000 total income | Tax rebate may reduce tax up to the applicable limit, subject to conditions. |

| New tax regime | Up to ₹7,00,000 total income | Tax rebate may reduce tax under the new regime, subject to conditions. |

Important: Rebate under Section 87A is generally for resident individuals and is not available to NRIs. Tax treatment may also differ for special-rate incomes such as certain capital gains. Always verify your exact case before filing.

Health & Education Cess and Surcharge

After calculating income tax based on slabs, you also need to consider health and education cess. For FY 2024-25, health and education cess is generally calculated at 4% on the amount of income tax plus surcharge, if any. This means your final tax payable is not just the slab tax. Cess increases the final liability.

Surcharge may also apply when income exceeds specified high-income thresholds. Surcharge rules can be complex, especially for high-income taxpayers, capital gains, dividends and special-rate income. Marginal relief may apply in certain cases to reduce the impact of surcharge where income marginally crosses a threshold.

Income Tax Calculation Examples for FY 2024-25

The following examples are simplified and meant for understanding slab logic. Actual tax payable may change depending on salary structure, deductions, exemptions, special income, surcharge, cess, rebate, residential status, capital gains, losses, TDS and other factors.

Example 1: Taxable income of ₹6,50,000 under the new tax regime

Assume the taxpayer is a resident individual and taxable income under the new regime is ₹6,50,000. The slab calculation before rebate may look like this:

| Income Portion | Rate | Tax |

|---|---|---|

| Up to ₹3,00,000 | Nil | ₹0 |

| ₹3,00,001 to ₹6,50,000 | 5% | ₹17,500 |

Because the taxable income is within the new-regime rebate threshold for eligible resident individuals, the tax may be reduced through Section 87A rebate, subject to conditions. This is why slab tax and final tax payable may be different.

Example 2: Taxable income of ₹10,00,000 under the new tax regime

Assume the taxpayer has taxable income of ₹10,00,000 under the new regime. The slab-wise calculation before cess may look like this:

| Income Portion | Rate | Tax |

|---|---|---|

| Up to ₹3,00,000 | Nil | ₹0 |

| ₹3,00,001 to ₹7,00,000 | 5% | ₹20,000 |

| ₹7,00,001 to ₹10,00,000 | 10% | ₹30,000 |

| Total tax before cess | — | ₹50,000 |

Health and education cess would generally apply after calculating tax. If the taxpayer has salary income, available standard deduction and other regime-specific rules may affect the final taxable income.

Example 3: Taxable income of ₹10,00,000 under the old tax regime

Assume an individual below 60 years has taxable income of ₹10,00,000 after claiming eligible old-regime deductions and exemptions. The slab-wise calculation before cess may look like this:

| Income Portion | Rate | Tax |

|---|---|---|

| Up to ₹2,50,000 | Nil | ₹0 |

| ₹2,50,001 to ₹5,00,000 | 5% | ₹12,500 |

| ₹5,00,001 to ₹10,00,000 | 20% | ₹1,00,000 |

| Total tax before cess | — | ₹1,12,500 |

This example shows why old-regime deductions matter. If deductions reduce taxable income substantially, the old regime can still become competitive even though the slab rates are higher.

Which Tax Regime May Suit Different Taxpayer Profiles?

There is no universal answer. The right regime depends on your income structure, deductions, family responsibilities, investments, home loan, rent, insurance, retirement contributions and long-term goals.

1. Salaried employees with few deductions

If you are salaried and do not claim HRA, do not have a home loan, do not invest much under Section 80C, and have limited deductions, the new regime may be easier and potentially more beneficial.

2. Salaried employees claiming HRA and 80C

If you pay rent and claim HRA exemption, contribute to EPF, invest in ELSS or PPF, pay life insurance premium, pay children’s tuition fee or repay home loan principal, the old regime may deserve a serious comparison.

3. Home loan borrowers

Home loan borrowers should compare carefully because the old regime may allow eligible deduction for interest on housing loan under Section 24(b), subject to conditions.

4. Freelancers and consultants

Freelancers and consultants should not choose a regime casually. Their tax planning may involve professional receipts, expenses, presumptive taxation, advance tax, GST records, TDS under Form 16A, business bank statements and proper books or summaries.

5. Investors with capital gains

Investors with equity, mutual funds, property, bonds, ESOPs or unlisted shares should evaluate capital gains reporting separately. Some capital gains are taxed at special rates and may not follow normal slab logic in the same way.

6. NRIs with taxable income in India

NRIs should consider residential status, Indian income, TDS, DTAA relief, bank interest, rent, capital gains, property sale and foreign asset implications carefully. Section 87A rebate is generally not available to NRIs.

Documents and Details Required to Calculate Tax Correctly

Tax slab calculation is only accurate when the input data is correct. Before comparing old and new regimes for FY 2024-25, collect the documents and details relevant to your profile.

For salaried taxpayers

- Form 16 from employer.

- Salary slips, especially if you changed jobs.

- HRA and rent proof, if claiming old-regime exemption.

- Investment proofs for eligible deductions.

- Health insurance premium receipts.

- Home loan interest certificate, if applicable.

- Form 26AS, AIS and TIS for tax credit and income review.

For freelancers and professionals

- Invoices raised during FY 2024-25.

- Bank statements showing professional receipts.

- Expense records related to professional work.

- Form 16A and TDS details.

- Advance tax and self-assessment tax challans.

- GST records, if registered.

- Books of account or income-expense summary.

Common Mistakes to Avoid While Using Income Tax Slabs

- Assuming the highest slab rate applies to your entire income.

- Choosing the new regime only because it is the default.

- Choosing the old regime without checking whether deductions are actually available and supported by documents.

- Ignoring Section 87A rebate conditions.

- Forgetting health and education cess while estimating final tax.

- Ignoring surcharge if your income is high.

- Using gross salary instead of taxable income for regime comparison.

- Not considering income from previous employer.

- Ignoring interest, dividend, capital gains, rent or freelance income.

- Not checking AIS, TIS and Form 26AS before filing.

- Missing Form 10-IEA considerations for business or professional income cases.

FY 2024-25 Tax Planning Checklist Before Filing ITR

| Checklist Item | Why It Matters | Action Needed |

|---|---|---|

| Confirm financial year and assessment year | FY 2024-25 income is generally reported in AY 2025-26. | Select the correct AY while filing. |

| Calculate gross income from all sources | Salary alone may not be your total income. | Include interest, dividend, rent, capital gains and freelance income. |

| Check Form 16, AIS, TIS and Form 26AS | Helps identify mismatch and missing income. | Reconcile records before filing. |

| Compare old and new regimes | The default regime may not always be the cheapest. | Prepare both calculations. |

| Verify deduction proofs | Unsupported deductions can create future risk. | Keep receipts, statements and certificates ready. |

| Review capital gains separately | Capital gains may involve special schedules and rates. | Use accurate broker or mutual fund statements. |

| Check tax already paid | TDS, TCS and advance tax reduce final payable amount. | Match tax credits with official records. |

| Check bank account validation | Refund may be delayed if bank details are wrong. | Validate bank account on the e-filing portal. |

| E-verify after filing | ITR filing is incomplete without verification. | Complete e-verification within the applicable timeline. |

How WealthSure Helps with FY 2024-25 Tax Slab and Regime Planning

At WealthSure, we don’t just help you file taxes. We help you understand your tax position and make better financial decisions. The income tax slab for FY 2024-25 is only one part of the larger picture. The real value comes from accurate income classification, proper deduction review, correct regime selection, clean documentation and smart financial planning beyond tax filing.

- Old vs new tax regime comparison.

- Income tax return filing for salaried individuals.

- Freelancer and professional ITR filing.

- Capital gains tax reporting for shares, mutual funds and property.

- NRI tax filing and Indian income reporting.

- Business and professional income tax filing.

- Advance tax calculation and self-assessment tax support.

- Income tax notice response and revised return support.

- Tax planning integrated with SIPs, insurance, retirement and wealth goals.

File your FY 2024-25 ITR with confidence. WealthSure combines fintech convenience, TRP/ERI-enabled filing support and expert advisory to help you reduce errors and make informed tax decisions.

Get started with WealthSureFAQs on Income Tax Slab for FY 2024-25

1. What is the income tax slab for FY 2024-25 under the new tax regime?

For FY 2024-25, the new tax regime broadly has nil tax up to ₹3 lakh, 5% from ₹3 lakh to ₹7 lakh, 10% from ₹7 lakh to ₹10 lakh, 15% from ₹10 lakh to ₹12 lakh, 20% from ₹12 lakh to ₹15 lakh and 30% above ₹15 lakh, subject to applicable rebate, surcharge and cess.

2. What is the income tax slab for FY 2024-25 under the old tax regime?

For individuals below 60 years, the old regime broadly has nil tax up to ₹2.5 lakh, 5% from ₹2.5 lakh to ₹5 lakh, 20% from ₹5 lakh to ₹10 lakh and 30% above ₹10 lakh. Senior citizens and super senior citizens have different basic exemption limits under the old regime.

3. Is FY 2024-25 the same as AY 2025-26?

No. FY 2024-25 is the financial year in which income is earned, from 1 April 2024 to 31 March 2025. AY 2025-26 is the assessment year in which that income is generally reported through the income tax return.

4. Is the new tax regime mandatory for FY 2024-25?

The new tax regime is the default regime for eligible taxpayers, but it is not necessarily mandatory for everyone. Eligible taxpayers can choose the old tax regime if it is more beneficial, subject to applicable conditions and timelines.

5. Which tax regime is better for FY 2024-25?

The better regime depends on your actual taxable income, deductions, exemptions, salary structure, investments, home loan, rent, health insurance, NPS contribution and income type. You should compare final tax payable under both regimes before filing.

6. Can salaried employees choose the old tax regime?

Eligible salaried employees can choose the old regime while filing their ITR if it is more beneficial. They should compare both regimes using Form 16, salary details, deductions, HRA, home loan interest and other eligible claims.

7. Can freelancers choose between old and new tax regimes?

Freelancers and professionals should check the applicable rules carefully, especially if they have business or professional income. Form 10-IEA and regime switching rules may apply in certain cases. Professional guidance can help avoid mistakes.

8. What is Section 87A rebate for FY 2024-25?

Section 87A rebate can reduce tax liability for eligible resident individuals whose total income is within the applicable threshold. Under the old regime, the threshold is generally up to ₹5 lakh. Under the new regime, the threshold is generally up to ₹7 lakh, subject to conditions.

9. Is Section 87A rebate available to NRIs?

Section 87A rebate is generally available to resident individuals and is not available to NRIs. NRIs should review residential status, Indian income, TDS, capital gains and DTAA implications carefully before filing.

10. Does cess apply after income tax slab calculation?

Yes. Health and education cess is generally applicable at 4% on income tax plus surcharge, if any. This means final tax payable is usually higher than the slab tax amount alone.

11. Are deductions available in the new tax regime?

The new tax regime restricts many common deductions and exemptions available under the old regime. Some benefits may still be available depending on law and taxpayer type. Always check current rules before filing.

12. Should I use a tax calculator before filing?

Yes. A tax calculator or expert-assisted comparison can help estimate tax under both regimes. However, the calculator result is only as accurate as the data entered. Complex cases involving capital gains, foreign income, business income or notices should be reviewed by an expert.

Conclusion

The income tax slab for FY 2024-25 is the foundation of your tax calculation, but it is not the full story. The final tax you pay depends on your taxable income, tax regime selection, deductions, exemptions, rebate eligibility, surcharge, cess, TDS and the accuracy of your return filing. The new tax regime may be simpler and beneficial for many taxpayers, while the old tax regime may still help those with significant deductions and exemptions.

The safest approach is to prepare both calculations before filing your ITR for AY 2025-26. Review Form 16, AIS, TIS, Form 26AS, investment proofs, capital gains statements, bank interest and all income records. Do not choose a regime based on assumptions or social media shortcuts. Choose based on numbers, documentation and your overall financial plan.

With WealthSure, taxpayers can move beyond last-minute tax filing and make smarter financial decisions with expert-assisted tax filing, tax planning, compliance support and wealth advisory. Whether you are salaried, self-employed, an investor, an NRI or a business owner, accurate tax planning today can support better financial confidence tomorrow.

Need help calculating your FY 2024-25 tax liability? WealthSure can help you compare tax regimes, file your ITR accurately and plan your finances with confidence.

Talk to a WealthSure expertDisclaimer

This article is for general informational and educational purposes only. It does not constitute tax, legal, financial, investment or professional advice. Income tax slabs, deductions, exemptions, rebate rules, surcharge, cess, filing due dates, ITR forms and portal processes may change based on law, notifications and official guidance. Please verify details on the official Income Tax Department website or consult a qualified tax professional before filing your return or making tax decisions.