Income Tax Slab for FY 2025-26: New Regime, Old Regime, Rebate and Smart Tax Planning Guide

The income tax slab for FY 2025-26 is one of the most important tax-planning topics for Indian taxpayers because it directly affects salary structuring, investment decisions, advance tax, tax-saving declarations and income tax return filing for Assessment Year 2026-27. Whether you are a salaried employee, freelancer, consultant, investor, senior citizen, NRI with Indian income or a first-time taxpayer, understanding the slab rates helps you avoid confusion before filing your return.

For FY 2025-26, taxpayers should pay close attention to the difference between the new tax regime and the old tax regime. The new tax regime is the default regime, but eligible taxpayers may still compare and choose the old regime if deductions, exemptions and long-term tax planning make it more beneficial. This decision should not be made casually. A lower slab rate does not always mean lower final tax, and a deduction-heavy old regime does not always save more tax.

This guide explains the income tax slabs for FY 2025-26 in simple language, with slab tables, examples, regime comparison, rebate explanation, cess, senior citizen considerations and practical tax-planning tips. It is designed to help you understand the numbers before you file your ITR, plan salary declarations, estimate tax payable and decide whether expert tax assistance may help.

Important: FY 2025-26 means income earned from 1 April 2025 to 31 March 2026. The return for this financial year is generally filed in AY 2026-27. Slab rates, deductions, rebates, surcharge, due dates and ITR utilities should always be cross-checked with the official Income Tax Department e-Filing portal before final filing.

Table of Contents

- What does income tax slab for FY 2025-26 mean?

- New tax regime slab for FY 2025-26

- Old tax regime slab for FY 2025-26

- Section 87A rebate and the ₹12 lakh confusion

- Old vs new regime: which one should you choose?

- Tax calculation examples for FY 2025-26

- Tax slab planning for different taxpayer profiles

- Common mistakes taxpayers make while reading slab rates

- FY 2025-26 tax planning checklist

- FAQs on income tax slab for FY 2025-26

What does income tax slab for FY 2025-26 mean?

An income tax slab is a range of taxable income on which a specific tax rate applies. India follows a progressive tax system for individual taxpayers. This means your entire income is not taxed at the highest slab rate. Instead, different portions of taxable income are taxed at different rates.

For example, if your taxable income crosses a higher slab, only the income falling in that higher slab is taxed at that higher rate. This is why slab-based tax calculation is different from simply multiplying total income by one tax rate.

The phrase income tax slab for FY 2025-26 usually refers to the tax rates applicable to income earned during the financial year 2025-26. For income tax return purposes, this generally corresponds to Assessment Year 2026-27.

Financial Year vs Assessment Year

| Term | Meaning | For this article |

|---|---|---|

| Financial Year | The year in which you earn income | FY 2025-26: 1 April 2025 to 31 March 2026 |

| Assessment Year | The year in which that income is assessed and the return is filed | AY 2026-27 |

| Taxable Income | Income after applying eligible deductions, exemptions and adjustments | The amount on which slab rates are applied |

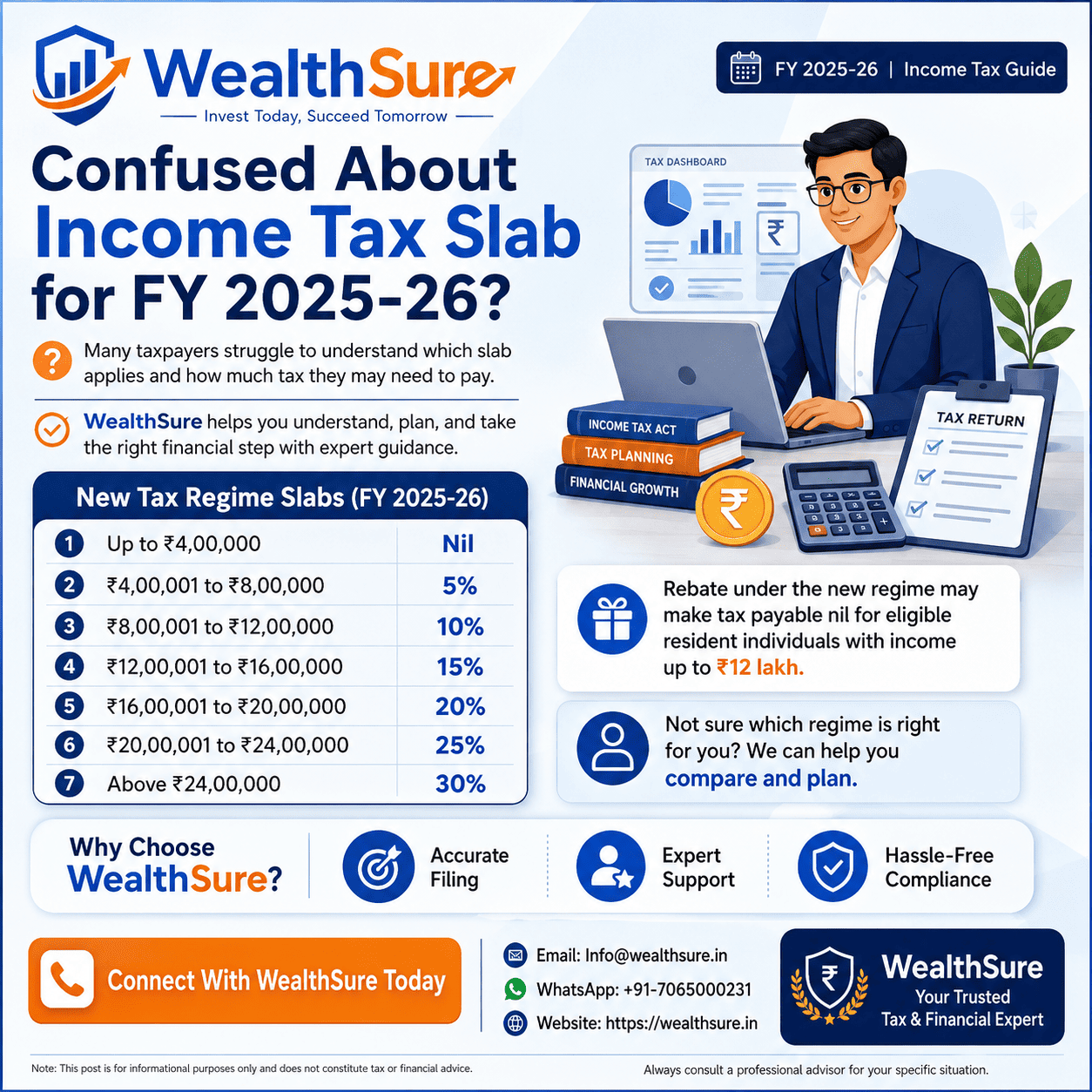

Income Tax Slab for FY 2025-26 under the New Tax Regime

The new tax regime is the default regime for eligible individual taxpayers. It offers wider slab bands and lower rates compared with the old regime, but it allows fewer deductions and exemptions. It is often useful for taxpayers who do not claim many deductions, do not have large HRA benefits, do not have significant Section 80C investments or prefer a simpler tax structure.

| Taxable Income Slab | Income Tax Rate under New Regime | Simple Explanation |

|---|---|---|

| Up to ₹4,00,000 | Nil | No tax on this slab. |

| ₹4,00,001 to ₹8,00,000 | 5% | 5% tax on income above ₹4 lakh in this range. |

| ₹8,00,001 to ₹12,00,000 | 10% | 10% tax on income above ₹8 lakh in this range. |

| ₹12,00,001 to ₹16,00,000 | 15% | 15% tax on income above ₹12 lakh in this range. |

| ₹16,00,001 to ₹20,00,000 | 20% | 20% tax on income above ₹16 lakh in this range. |

| ₹20,00,001 to ₹24,00,000 | 25% | 25% tax on income above ₹20 lakh in this range. |

| Above ₹24,00,000 | 30% | 30% tax on income above ₹24 lakh. |

WealthSure tip: The new regime should be evaluated after considering standard deduction, employer NPS contribution where applicable, eligible new-regime deductions and Section 87A rebate. Do not compare only the slab rates; compare final tax payable.

Income Tax Slab for FY 2025-26 under the Old Tax Regime

The old tax regime continues to matter for taxpayers who claim deductions and exemptions. It may benefit people with significant Section 80C investments, HRA exemption, home loan interest, health insurance deduction, education loan interest, donations, NPS contribution and other eligible deductions.

Old tax regime slab for individuals below 60 years

| Taxable Income Slab | Income Tax Rate under Old Regime | Simple Explanation |

|---|---|---|

| Up to ₹2,50,000 | Nil | No tax on this slab. |

| ₹2,50,001 to ₹5,00,000 | 5% | 5% on income above ₹2.5 lakh. |

| ₹5,00,001 to ₹10,00,000 | 20% | ₹12,500 plus 20% on income above ₹5 lakh. |

| Above ₹10,00,000 | 30% | ₹1,12,500 plus 30% on income above ₹10 lakh. |

Old tax regime slab for senior citizens and super senior citizens

Under the old tax regime, senior citizens and super senior citizens receive higher basic exemption limits. Senior citizens generally refer to resident individuals aged 60 years or more but below 80 years, while super senior citizens are resident individuals aged 80 years or more.

| Taxpayer Category | Basic Exemption Limit under Old Regime | Why It Matters |

|---|---|---|

| Individual below 60 years | ₹2,50,000 | Standard basic exemption under the old regime. |

| Resident senior citizen | ₹3,00,000 | Higher exemption may reduce tax for retirees with pension and interest income. |

| Resident super senior citizen | ₹5,00,000 | Higher exemption may be useful for elderly taxpayers with taxable income. |

Confused between old and new regime? WealthSure can help you compare both regimes using your salary, deductions, investments, home loan, HRA, capital gains and other income details before you file.

Ask a WealthSure tax expertSection 87A Rebate: Does ₹12 Lakh Income Mean Zero Tax?

This is where many taxpayers get confused. Under the new tax regime for FY 2025-26, eligible resident individuals may get rebate under Section 87A if taxable income does not exceed ₹12,00,000. The rebate can reduce tax liability, subject to applicable conditions.

However, this does not mean the slab rate itself is nil up to ₹12 lakh. The slab table still taxes income in layers: nil up to ₹4 lakh, 5% from ₹4 lakh to ₹8 lakh and 10% from ₹8 lakh to ₹12 lakh. The rebate may then reduce the tax payable for eligible resident individuals whose taxable income is within the prescribed threshold.

| Point | New Regime | Old Regime |

|---|---|---|

| Section 87A rebate limit | Up to ₹60,000 | Up to ₹12,500 |

| Taxable income condition | Taxable income should not exceed ₹12,00,000 | Taxable income should not exceed ₹5,00,000 |

| Who should be careful? | Taxpayers near the ₹12 lakh threshold, taxpayers with special-rate income, and taxpayers with multiple income sources | Taxpayers relying on deductions to bring taxable income within ₹5 lakh |

Practical caution: Tax treatment can be different for certain special-rate incomes such as capital gains. If you have equity gains, mutual fund gains, crypto or virtual digital asset income, foreign income or business income, do not assume the rebate outcome without a proper calculation.

Old Tax Regime vs New Tax Regime for FY 2025-26

The correct regime depends on your actual income profile. The new regime may suit taxpayers who want simplicity and have limited deductions. The old regime may suit taxpayers with strong deduction claims and salary exemptions. A careful comparison can prevent unnecessary tax outflow.

New Tax Regime

Best suited for taxpayers who have fewer deductions, simpler income, limited HRA benefit, limited tax-saving investments or prefer a cleaner tax calculation with lower slab rates.

- Lower slab rates across wider income bands.

- Fewer deductions and exemptions.

- Useful for many salaried and first-time taxpayers.

- Needs careful review if income is near rebate thresholds.

Old Tax Regime

Best suited for taxpayers who claim deductions and exemptions such as Section 80C, HRA, home loan interest, health insurance, NPS and education loan interest.

- Higher slab rates but wider deduction opportunities.

- Useful for deduction-heavy taxpayers.

- Requires documentation and proof.

- May be better for planned taxpayers with eligible claims.

Decision-tree style guide: how to choose the regime

- Start with gross income. Include salary, interest, rent, capital gains, freelance receipts, pension and other taxable income.

- Calculate new regime tax. Apply the FY 2025-26 new regime slabs and consider eligible new-regime benefits.

- Calculate old regime tax. Apply eligible deductions and exemptions first, then calculate old regime tax.

- Check rebate eligibility. See whether Section 87A rebate applies under the relevant regime.

- Add cess and surcharge where applicable. Final tax comparison should include Health and Education Cess and surcharge if income crosses applicable limits.

- Choose based on final tax, not assumptions. The better regime is the one that gives lower compliant tax liability with valid supporting documents.

Tax Calculation Examples for FY 2025-26

The examples below are simplified for understanding slab logic. They do not cover every deduction, surcharge, special-rate income or salary component. Use them as educational illustrations, not final tax advice.

Example 1: Taxable income of ₹8,00,000 under the new regime

| Slab Portion | Rate | Tax |

|---|---|---|

| Up to ₹4,00,000 | Nil | ₹0 |

| ₹4,00,001 to ₹8,00,000 | 5% | ₹20,000 |

| Total before rebate and cess | — | ₹20,000 |

If the taxpayer is an eligible resident individual and taxable income is within the prescribed rebate threshold, Section 87A rebate may reduce tax liability. Always confirm eligibility and income composition before final filing.

Example 2: Taxable income of ₹15,00,000 under the new regime

| Slab Portion | Rate | Tax |

|---|---|---|

| Up to ₹4,00,000 | Nil | ₹0 |

| ₹4,00,001 to ₹8,00,000 | 5% | ₹20,000 |

| ₹8,00,001 to ₹12,00,000 | 10% | ₹40,000 |

| ₹12,00,001 to ₹15,00,000 | 15% | ₹45,000 |

| Total before cess | — | ₹1,05,000 |

| Health and Education Cess | 4% | ₹4,200 |

| Total tax payable | — | ₹1,09,200 |

Example 3: Why a deduction-heavy taxpayer may still compare the old regime

Assume a salaried taxpayer has gross income of ₹14,50,000 and valid old-regime deductions and exemptions through HRA, Section 80C, health insurance and home loan interest. If these deductions bring taxable income down meaningfully, the old regime may compete with or outperform the new regime. But if the taxpayer has limited deductions, the new regime may be simpler and more tax-efficient.

This is why WealthSure recommends a calculation-first approach instead of choosing based on social media posts, office assumptions or a quick salary-declaration guess.

Tax Slab Planning for Different Taxpayer Profiles

For salaried employees

Salaried taxpayers should compare regimes during salary declaration and again before ITR filing. Your employer may deduct TDS based on the declaration you provide, but the final responsibility to file correctly remains with you. Check salary, perquisites, HRA, standard deduction, professional tax, Form 16, AIS and Form 26AS before filing.

For freelancers and consultants

Freelancers should not look only at slab rates. They should calculate business or professional income after allowable expenses, TDS, advance tax and presumptive taxation eligibility where applicable. If your income is uneven through the year, advance tax planning becomes important.

For investors with capital gains

Capital gains may be taxed under special provisions depending on asset type, holding period and applicable rules. Equity shares, mutual funds, property, bonds, ESOPs and foreign assets can have different tax treatment. Slab rates may not apply to every component of income in the same way.

For senior citizens

Senior citizens should compare both regimes carefully, especially if income includes pension, interest, rent, capital gains and medical insurance payments. Under the old regime, senior citizens may benefit from higher basic exemption and certain deductions, but the new regime can still be useful depending on the final calculation.

For NRIs with Indian income

NRIs with Indian salary, rent, capital gains, interest or business income should evaluate residential status, taxable Indian income, TDS, DTAA relevance and reporting requirements. Do not assume the same treatment as a resident taxpayer without checking the facts.

Have salary, capital gains, freelance income or NRI tax questions? WealthSure provides assisted ITR filing and expert tax planning support so you can choose the right regime and file with confidence.

Explore WealthSure ITR filing servicesCommon Mistakes While Reading the Income Tax Slab for FY 2025-26

- Assuming the highest slab applies to full income: Slab taxation is progressive. Only income in a slab is taxed at that slab rate.

- Thinking ₹12 lakh is a nil-tax slab: It is linked to rebate eligibility under the new regime, not a nil slab up to ₹12 lakh.

- Ignoring cess: Health and Education Cess is added after computing tax and surcharge, where applicable.

- Choosing the new regime only because it is default: Default does not always mean best. Compare both regimes.

- Choosing the old regime without proof: Old-regime deductions require documentation and eligibility.

- Ignoring special-rate income: Capital gains, crypto income and certain other income categories may need separate treatment.

- Not planning advance tax: Freelancers, consultants, investors and business owners may need advance tax planning if tax liability exceeds applicable limits.

- Waiting until the last filing week: Last-minute filing increases the risk of missed income, wrong regime choice and tax credit mismatch.

FY 2025-26 Tax Planning Checklist

| Checklist Item | Why It Matters | Action |

|---|---|---|

| Estimate total income | Slab choice depends on taxable income, not only salary | Include salary, interest, rent, capital gains and other income |

| Compare old vs new regime | Final tax can differ significantly | Calculate both before filing |

| Check deductions | Old regime depends heavily on valid deductions | Keep proof for 80C, 80D, HRA, home loan and other claims |

| Review rebate eligibility | Section 87A can materially affect tax payable | Check taxable income and income composition |

| Check TDS and advance tax | Mismatch can lead to demand or refund delay | Reconcile Form 16, AIS, Form 26AS and challans |

| Plan investments | Tax planning should support financial goals | Do not invest only to save tax; align with risk and goals |

How WealthSure Helps with FY 2025-26 Tax Planning

At WealthSure, we do more than prepare returns. We help taxpayers understand the impact of the slab system, choose the right regime, avoid reporting errors and align tax planning with broader financial goals. For many taxpayers, the real question is not simply “What is my tax slab?” but “How do I structure income, deductions, investments and compliance correctly?”

WealthSure can help with:

- Old vs new tax regime comparison.

- Assisted income tax return filing.

- ITR form selection based on income profile.

- Capital gains reporting support.

- Freelancer and professional tax filing.

- NRI tax filing and Indian income review.

- Advance tax calculation.

- Income tax notice response.

- Tax planning and investment-aligned advisory.

Want to know which tax regime saves more for you? Share your income sources, deductions and tax documents with WealthSure experts for a guided review.

Start your tax reviewFAQs on Income Tax Slab for FY 2025-26

1. What is the income tax slab for FY 2025-26 under the new tax regime?

Under the new tax regime, tax is nil up to ₹4 lakh, 5% from ₹4 lakh to ₹8 lakh, 10% from ₹8 lakh to ₹12 lakh, 15% from ₹12 lakh to ₹16 lakh, 20% from ₹16 lakh to ₹20 lakh, 25% from ₹20 lakh to ₹24 lakh and 30% above ₹24 lakh, subject to rebate, cess and surcharge where applicable.

2. Is the new tax regime mandatory for FY 2025-26?

The new tax regime is the default regime, but eligible taxpayers may choose the old regime if it is more beneficial. The process and restrictions can differ for taxpayers with business or professional income, so check the applicable rules before filing.

3. Is income up to ₹12 lakh tax-free in FY 2025-26?

Eligible resident individuals may get rebate under Section 87A under the new regime if taxable income does not exceed ₹12 lakh. This should not be confused with a nil slab up to ₹12 lakh. The slab calculation and rebate mechanism are different.

4. What is the old tax regime slab for individuals below 60 years?

Under the old regime, tax is nil up to ₹2.5 lakh, 5% from ₹2.5 lakh to ₹5 lakh, 20% from ₹5 lakh to ₹10 lakh and 30% above ₹10 lakh, subject to rebate, cess and surcharge where applicable.

5. Which regime is better for salaried employees?

It depends on income, deductions and exemptions. Salaried employees with fewer deductions may find the new regime useful, while employees with HRA, 80C investments, home loan interest, NPS and health insurance deductions should compare both regimes before choosing.

6. Does Health and Education Cess apply in FY 2025-26?

Yes. Health and Education Cess is generally charged at 4% on income tax plus surcharge, if any, in both regimes.

7. Do senior citizens get different slabs in the new regime?

The new regime slab structure is generally common for individuals. Under the old regime, resident senior citizens and resident super senior citizens have higher basic exemption limits.

8. Should freelancers choose the old or new tax regime?

Freelancers should compare regimes after calculating professional income, eligible expenses, TDS, advance tax and deduction eligibility. Taxpayers with business or professional income should also check regime-switching rules carefully.

9. Are capital gains taxed according to normal slab rates?

Not always. Some capital gains are taxed at special rates depending on the asset, holding period and applicable provisions. Investors should not rely only on normal slab tables for capital gains taxation.

10. Can WealthSure help me compare both tax regimes?

Yes. WealthSure can help you compare old and new regime tax liability, review documents, plan deductions, calculate advance tax and file your ITR accurately based on your income profile.

Conclusion

Understanding the income tax slab for FY 2025-26 is not just about memorising rates. It is about knowing how the slab system works, how rebate affects tax payable, how the old and new regimes differ, and how your salary, deductions, investments, capital gains and other income sources change the final result.

The new tax regime may be simpler and beneficial for many taxpayers, but the old regime can still be valuable for those with valid deductions and exemptions. The smartest approach is to calculate both regimes, review your documents and make a compliant decision before filing your return for AY 2026-27.

Tax planning should also connect with financial planning. A good regime choice should not only reduce tax legally but also support your wealth creation, insurance, retirement, emergency fund and long-term financial goals.

File and plan smarter with WealthSure. Get expert-led tax filing, tax planning and financial advisory support for FY 2025-26.

Get started with WealthSureDisclaimer

This article is for general informational and educational purposes only. It does not constitute tax, legal, investment, financial or professional advice. Income tax rules, slab rates, rebates, deductions, surcharge, cess, ITR forms, due dates and portal processes may change. Please verify the latest information on the official Income Tax Department portal or consult a qualified tax professional before filing your return or making tax decisions.