Income Tax Slab for FY 2026-27: New vs Old Tax Regime Explained

The income tax slab for FY 2026-27 is one of the most important tax-planning references for Indian taxpayers. It affects monthly TDS, take-home salary, advance tax, regime selection, investment planning, capital gains planning, business income estimates and the final income tax return. The challenge is that most people look at slabs as a simple table, while actual tax payable depends on many moving parts: total income, selected tax regime, standard deduction, eligible deductions, rebate, surcharge, cess and special-rate income.

From 1 April 2026, taxpayers also need to understand the term Tax Year 2026-27. Under the Income-tax Act, 2025 framework, the tax year concept applies for income earned during FY 2026-27 onwards. For practical readers, this means income earned from 1 April 2026 to 31 March 2027 is relevant for FY 2026-27 / Tax Year 2026-27. The return, forms and filing utilities should still be checked on the official Income Tax Department portal before filing.

This WealthSure guide is designed for salaried professionals, freelancers, consultants, investors, NRIs with Indian income, small business owners and first-time taxpayers who want a clear, people-first explanation of the tax slabs. You will understand the current slab structure, how the old and new regimes differ, why rebate is different from exemption, when deductions still matter and how to plan taxes without rushing at the last minute.

Important: This article is for education and planning. Tax law, rules, forms, due dates, rebate treatment and portal processes can change. Verify the latest position on the official Income Tax Department e-Filing portal or consult a qualified tax professional before filing.

Table of Contents

- Income tax slab for FY 2026-27: quick answer

- New tax regime slab for FY 2026-27

- Old tax regime slab for FY 2026-27

- New vs old tax regime: key differences

- Standard deduction for salaried taxpayers

- Rebate, marginal relief and cess

- Income tax calculation examples

- Decision guide: which regime may suit you?

- Planning tips for salaried, freelancers, investors and NRIs

- Common mistakes to avoid

- FAQs on income tax slab for FY 2026-27

Income Tax Slab for FY 2026-27: Quick Answer

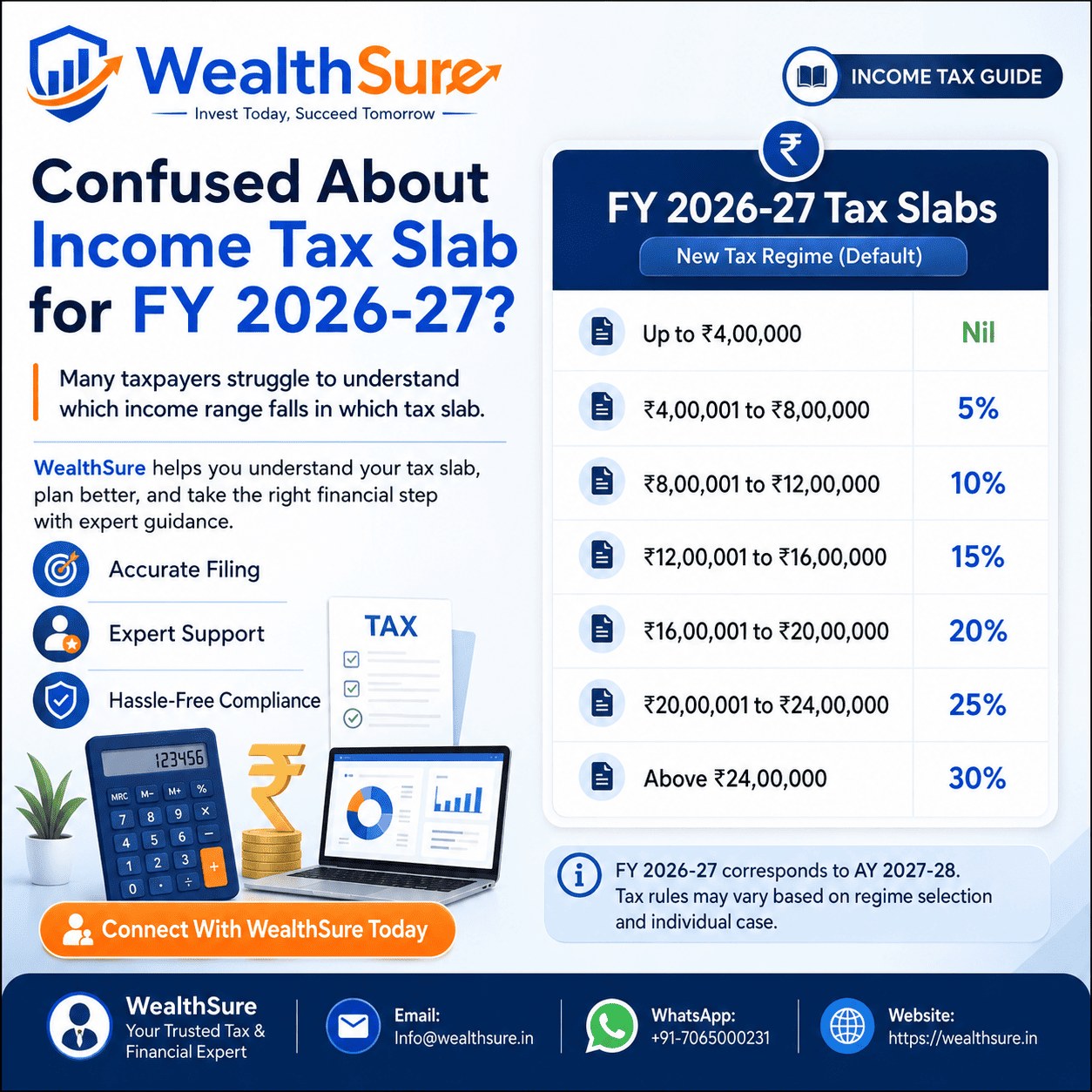

For FY 2026-27, the default new tax regime slab structure for individuals and HUFs is expected to remain the primary reference point unless amended by the government. Under the current structure, regular income is taxed progressively from nil up to ₹4 lakh and then at 5%, 10%, 15%, 20%, 25% and 30% across higher slabs. The highest slab rate applies to income above ₹24 lakh, but only to that portion of income, not the whole income.

The old tax regime also remains relevant because it allows many deductions and exemptions, including common claims such as HRA, Section 80C investments, eligible insurance premiums, certain housing loan benefits and other permitted deductions. For a taxpayer with strong deductions, the old regime can sometimes produce a lower final tax, even when its slab rates look higher.

New Tax Regime Slab for FY 2026-27

The new tax regime is designed around wider income slabs and lower rates. It is often simpler for taxpayers who do not claim many deductions. However, simpler does not always mean cheaper. You should still compare the final tax under both regimes before deciding.

| Total Income Slab | Income Tax Rate | How to Understand It |

|---|---|---|

| Up to ₹4,00,000 | Nil | No tax on this portion of regular income |

| ₹4,00,001 to ₹8,00,000 | 5% | Tax applies only on the income falling in this slab |

| ₹8,00,001 to ₹12,00,000 | 10% | The next portion of taxable income is taxed at 10% |

| ₹12,00,001 to ₹16,00,000 | 15% | Middle-to-higher income band under the new regime |

| ₹16,00,001 to ₹20,00,000 | 20% | Applies progressively on this income portion |

| ₹20,00,001 to ₹24,00,000 | 25% | Applies before the highest slab begins |

| Above ₹24,00,000 | 30% | Highest new-regime slab rate for regular income |

A common mistake is to assume that if your income is ₹25 lakh, the full ₹25 lakh is taxed at 30%. That is incorrect. Slab taxation is progressive. Each slab applies only to the part of income that falls inside that slab. This is why two taxpayers with similar gross income can still have different final tax payable depending on deductions, rebate eligibility, capital gains and other adjustments.

Old Tax Regime Slab for FY 2026-27

The old tax regime is deduction-friendly. It may be attractive if you have HRA, eligible Section 80C investments, health insurance premiums, home loan interest or other allowable deductions. The rates appear higher, but final tax can be lower when deductions are substantial.

| Taxpayer Category | Total Income Slab | Income Tax Rate |

|---|---|---|

| Individuals below 60 years and HUFs | Up to ₹2,50,000 | Nil |

| Individuals below 60 years and HUFs | ₹2,50,001 to ₹5,00,000 | 5% |

| Individuals below 60 years and HUFs | ₹5,00,001 to ₹10,00,000 | 20% |

| Individuals below 60 years and HUFs | Above ₹10,00,000 | 30% |

| Resident senior citizens aged 60 to below 80 years | Up to ₹3,00,000 | Nil |

| Resident senior citizens aged 60 to below 80 years | ₹3,00,001 to ₹5,00,000 | 5% |

| Resident super senior citizens aged 80 years and above | Up to ₹5,00,000 | Nil |

The old regime is not automatically better just because it offers deductions. A taxpayer should compare the tax saved through deductions against the benefit of lower slabs under the new regime. For example, if you invest only for tax benefits but the investment does not fit your goals, liquidity needs or risk profile, tax saving may become poor financial planning.

Not sure which regime works for you? WealthSure can compare your tax under both regimes using your salary, deductions, rent, home loan, capital gains, business income and investment details.

Ask a WealthSure tax expertNew vs Old Tax Regime for FY 2026-27: Key Differences

The old and new regimes are not just two tables. They reflect two different tax-planning styles. The new regime rewards simplicity. The old regime rewards documented deductions and structured financial planning.

Best suited for simpler tax profiles

The new regime may be useful when you have fewer deductions, no major HRA claim, limited eligible investments and prefer a cleaner calculation.

- Wider income slabs.

- Lower rates across more bands.

- Default regime for many taxpayers.

- Fewer deductions and exemptions.

Best suited for deduction-heavy taxpayers

The old regime may be useful if your financial life includes HRA, housing loan interest, insurance premiums, Section 80C investments and other eligible claims.

- Allows many deductions and exemptions.

- Requires stronger documentation.

- Can support disciplined tax-saving investments.

- May benefit families with structured expenses.

| Point | New Tax Regime | Old Tax Regime |

|---|---|---|

| Core approach | Lower slab rates with fewer claims | Higher slab rates but more deductions and exemptions |

| HRA | Generally not available in the same manner | Can be claimed if conditions and documents are met |

| Tax-saving investments | Limited deduction benefit | Common deductions may be available subject to law |

| Ease of filing | Usually simpler | Requires proof-based planning |

| Best decision method | Calculate both regimes using actual income and deductions before choosing | |

Standard Deduction for Salaried Taxpayers in FY 2026-27

Standard deduction is important because it directly reduces taxable salary or pension income without requiring individual expense bills. For eligible salaried taxpayers and pensioners, the standard deduction is generally higher under the new regime than under the old regime.

| Tax Regime | Standard Deduction | Why It Matters |

|---|---|---|

| New tax regime | Up to ₹75,000 | Can reduce taxable income and improve new-regime outcome |

| Old tax regime | Up to ₹50,000 | Works along with other eligible deductions and exemptions |

For example, if an eligible salaried taxpayer has gross salary income of ₹12,75,000 under the new regime, standard deduction may reduce the taxable salary by up to ₹75,000. This can meaningfully affect the final slab calculation. But the taxpayer must still check other income such as interest, dividends, rent, capital gains or freelance receipts before assuming the final tax.

Rebate, Marginal Relief and Cess

Rebate is often confused with the basic exemption slab. They are not the same. A nil slab means a portion of income is not taxed. Rebate is a separate relief that can reduce the final tax for eligible resident individuals when income is within the prescribed threshold and conditions are met.

Health and Education Cess is generally levied at 4% on income tax plus surcharge, wherever surcharge applies. High-income taxpayers also need to account for surcharge and marginal relief. Taxpayers with income above surcharge thresholds, large bonuses, ESOPs, capital gains or business income should calculate tax carefully rather than relying on salary TDS alone.

Planning tip: If your income is close to a rebate or surcharge threshold, small changes in bonus, interest income, capital gains or deductions can affect your final tax payable. Run a full-year estimate before March instead of waiting for ITR filing season.

Income Tax Calculation Examples for FY 2026-27

The examples below are simplified and educational. They are meant to show how slab thinking works. Actual tax may change because of deductions, employer benefits, capital gains, losses, surcharge, cess, professional income, advance tax, foreign income and other factors.

Example 1: Salaried taxpayer with simple income

Assume a salaried taxpayer has limited deductions and no major HRA, home loan or capital gains. The new regime may be easier because the slabs are wider and the standard deduction under the new regime can reduce taxable salary. The taxpayer should still include savings account interest, fixed deposit interest and any other income before checking rebate or final tax.

Example 2: Salaried taxpayer with HRA and investments

Assume a salaried taxpayer pays rent, has a valid HRA claim, invests under Section 80C and pays health insurance premiums. The old regime may still be worth comparing because the deductions can reduce taxable income. The new regime may still win if deductions are not large enough, so actual calculation is necessary.

Example 3: Investor with salary and capital gains

Assume a taxpayer has salary income plus gains from shares or mutual funds. Regular income may follow slab rates, but capital gains can be taxed under special rules. This taxpayer should not estimate tax only from the salary slab table. Capital gains statements, holding period and special-rate tax treatment must be reviewed separately.

Decision Guide: Which Regime May Suit You?

Use this practical decision guide before choosing a regime. It is not a substitute for computation, but it helps you understand where to focus.

List income sources. Include salary, business income, interest, rent, capital gains and freelance receipts.

Check deductions. Review HRA, 80C, insurance, home loan and other eligible claims.

Compare regimes. Calculate both old and new regime tax using actual numbers.

Plan action. Adjust TDS, advance tax, investment proof and filing preparation.

Choose the new regime when:

- You have limited deductions and exemptions.

- You do not claim HRA or large housing-related benefits.

- You prefer a simpler computation and documentation process.

- Your tax-saving investments are made for goals, not only for deductions.

- Your regime comparison shows lower tax under the new regime.

Consider the old regime when:

- You have valid HRA and rent documentation.

- You use Section 80C effectively through EPF, life insurance, ELSS, tuition fees or other eligible items.

- You pay health insurance premiums for yourself, family or parents.

- You have eligible home loan interest benefits.

- Your deductions are substantial enough to offset higher slab rates.

Planning Tips for Different Taxpayer Profiles

For salaried employees

Do not wait until return filing season. Compare regimes at the start of the year, again when salary revisions or bonuses are known, and once more before submitting final investment proofs. If you changed jobs, include income from both employers to avoid under-deduction of TDS.

For freelancers and consultants

Slabs apply after computing taxable income, but freelancers must first calculate professional receipts, allowable expenses, TDS credits and advance tax. If presumptive taxation is relevant, check eligibility carefully. Poor expense records can lead to incorrect tax estimates and avoidable notices.

For investors

Capital gains may not follow ordinary slab treatment. Equity, mutual funds, property, bonds, ESOPs and foreign assets can require separate calculations and disclosures. Investors should maintain annual capital gains statements and review tax impact before major redemptions or asset sales.

For NRIs

NRIs should review residential status, India-sourced income, TDS, DTAA position, rental income, capital gains and bank interest before applying slab assumptions. Rebate, deductions and filing requirements may depend on residence and income type.

For small business owners

Business owners should look beyond slabs. Books of account, GST data, TDS, depreciation, presumptive taxation, advance tax and business deductions can materially affect taxable income. A tax slab table is useful, but business tax planning requires a full compliance view.

Need a full-year FY 2026-27 tax plan? WealthSure can help you estimate tax, compare regimes, review deductions, plan advance tax, handle capital gains reporting and prepare for accurate ITR filing.

Explore WealthSure ITR filing servicesCommon Mistakes to Avoid While Using FY 2026-27 Tax Slabs

- Assuming the highest slab rate applies to the entire income.

- Choosing the new regime without comparing old-regime deductions.

- Choosing the old regime only because deductions are available, without checking final tax.

- Ignoring standard deduction in salary tax estimates.

- Confusing rebate with slab exemption.

- Ignoring interest income, dividends, rent or capital gains.

- Not planning advance tax on non-salary income.

- Ignoring surcharge and cess in high-income cases.

- Not maintaining rent, investment, insurance and home loan proofs.

- Assuming employer TDS means the ITR will automatically be correct.

FY 2026-27 Tax Planning Checklist

| Checklist Item | Action | Why It Matters |

|---|---|---|

| Regime comparison | Calculate tax under old and new regimes | Prevents guess-based tax decisions |

| Salary review | Check HRA, reimbursements, employer NPS and bonus | Helps optimise TDS and take-home pay |

| Investment planning | Align tax-saving investments with financial goals | Avoids buying poor-fit products only for deductions |

| Insurance review | Check term and health insurance adequacy | Supports protection as well as tax planning |

| Capital gains tracking | Collect broker and mutual fund statements | Reduces reporting errors during ITR filing |

| Advance tax | Estimate tax on non-salary income during the year | Helps avoid interest where advance tax applies |

| Documentation | Save rent receipts, proofs, loan certificates and challans | Supports deductions and future tax responses |

FAQs on Income Tax Slab for FY 2026-27

1. What is the income tax slab for FY 2026-27 under the new tax regime?

Under the current new regime structure, income up to ₹4 lakh is nil-rated, followed by progressive slab rates of 5%, 10%, 15%, 20%, 25% and 30% for higher bands. The 30% slab applies to income above ₹24 lakh.

2. Is FY 2026-27 the same as Tax Year 2026-27?

For income earned from 1 April 2026 onwards, the Income-tax Act, 2025 uses the tax year concept. Income earned from 1 April 2026 to 31 March 2027 is referred to as Tax Year 2026-27.

3. Is income up to ₹12 lakh completely tax-free?

Do not confuse rebate with slab exemption. The nil slab and rebate are different concepts. Eligibility for rebate depends on the taxpayer, total income, regime and applicable conditions. Always calculate final tax using actual income.

4. What is the standard deduction for salaried employees in FY 2026-27?

Eligible salaried taxpayers and pensioners should consider the applicable standard deduction based on the selected regime. The current threshold reference is up to ₹75,000 under the new regime and up to ₹50,000 under the old regime.

5. Which is better for FY 2026-27: new regime or old regime?

The better regime depends on actual numbers. If you have limited deductions, the new regime may work better. If you have HRA, housing loan interest, 80C investments and insurance deductions, the old regime may be worth comparing.

6. Do senior citizens get different slabs?

Senior and super senior citizens have higher basic exemption limits under the old regime, subject to conditions. Under the new regime, taxpayers should verify the applicable slab and eligibility rules before filing.

7. Does cess apply after calculating slab tax?

Health and Education Cess is generally added after computing income tax and surcharge, wherever surcharge applies. This means final tax payable is more than base slab tax alone.

8. Do capital gains follow the same slab rates?

Not always. Certain capital gains can be taxed at special rates. Investors should review capital gains statements and applicable rules separately before filing.

9. Should freelancers use these tax slabs?

Freelancers and consultants may use individual slab rates for regular income after computing professional income, expenses and deductions. They should also review TDS and advance tax requirements.

10. Can WealthSure help with FY 2026-27 tax planning?

Yes. WealthSure can help with regime comparison, tax planning, assisted ITR filing, capital gains reporting, freelancer tax filing, NRI taxation, advance tax calculation and notice-response support.

Conclusion

The income tax slab for FY 2026-27 gives you the base structure for tax planning, but it is not the full answer. Your final tax depends on the regime selected, deductions, standard deduction, rebate, special-rate income, surcharge, cess and documentation. The safest approach is to calculate both regimes, understand your income profile and make a decision that supports both compliance and long-term financial planning.

At WealthSure, we believe tax planning should not be a last-minute activity. A smart taxpayer plans early, compares regimes, keeps records ready, reviews investments thoughtfully and files accurately. When the tax slab is understood correctly, it becomes more than a table — it becomes a roadmap for better financial decisions.

Plan your FY 2026-27 taxes with confidence. WealthSure helps individuals, professionals, investors, NRIs and business owners simplify tax filing, tax planning and long-term financial decisions.

Start your tax planning with WealthSureDisclaimer

This article is for general informational and educational purposes only. It does not constitute tax, legal, investment, financial or professional advice. Income tax laws, slabs, deductions, rebates, surcharge, cess, forms, filing utilities and portal processes may change. Please verify the latest rules from the official Income Tax Department website or consult a qualified tax professional before filing your return or making tax decisions.