Income Tax Slabs for FY 2025-26: New vs Old Tax Regime Guide

Understanding the income tax slabs for FY 2025-26 is essential before you plan your salary structure, deductions, investments, advance tax, capital gains reporting or income tax return filing for Assessment Year 2026-27. Many taxpayers search for slab rates only to know “how much tax will I pay?”, but the real answer depends on more than one table. It depends on the tax regime you choose, whether rebate applies, whether your income includes capital gains or other special-rate income, whether you are salaried or self-employed, and whether deductions under the old regime can reduce your taxable income meaningfully.

For FY 2025-26, the new tax regime continues to be the default regime for eligible taxpayers and has revised slab rates with a nil slab up to ₹4 lakh. Eligible resident individuals may also benefit from Section 87A rebate up to the prescribed limit where taxable income does not exceed ₹12 lakh under the new regime. For salaried taxpayers, the standard deduction of ₹75,000 can make the widely discussed ₹12.75 lakh figure relevant, subject to conditions and the nature of income.

At the same time, the old tax regime has not lost relevance. If you claim HRA, use Section 80C, pay health insurance premium under Section 80D, have home loan interest, contribute to NPS or use other eligible deductions, the old regime may still produce a lower final tax liability. This WealthSure guide explains the slab rates, compares the new and old regimes, shows practical examples, highlights common mistakes and gives a decision framework for salaried individuals, freelancers, professionals, investors, senior citizens, NRIs and business owners.

Important: This article explains income tax slabs for FY 2025-26, which generally correspond to AY 2026-27. Tax laws, forms, deductions and return instructions may change. Always verify the latest rules on the official Income Tax Department portal before filing your return.

Table of Contents

- Quick summary of income tax slabs for FY 2025-26

- New tax regime slabs for FY 2025-26

- Old tax regime slabs for FY 2025-26

- Section 87A rebate and zero-tax income limit

- Old vs new tax regime: how to choose

- Practical tax examples for FY 2025-26

- Surcharge and cess explained

- Guidance for different taxpayer profiles

- Common mistakes to avoid

- Tax-planning checklist before filing ITR

- FAQs on income tax slabs for FY 2025-26

Quick Summary of Income Tax Slabs for FY 2025-26

The biggest practical change for taxpayers is that the new regime has become more attractive for many middle-income earners because of wider slab bands and a higher rebate threshold. However, that does not automatically make it the best choice for everyone. A taxpayer with high rent, full 80C investments, health insurance, home loan interest and other eligible deductions may still need to compare the old regime carefully.

India follows a progressive slab system. This means the higher tax rate applies only to the portion of income that falls in that slab, not to the entire income. If your taxable income crosses ₹12 lakh, the higher rate does not apply from the first rupee. Each income layer is taxed at its respective slab rate.

| Point | FY 2025-26 Treatment | Why It Matters |

|---|---|---|

| Default regime | New tax regime under Section 115BAC | You must actively opt for the old regime if it is beneficial and if you satisfy the applicable rules. |

| New regime nil slab | Up to ₹4,00,000 | Useful for taxpayers with simple income and limited deduction requirements. |

| New regime rebate threshold | Taxable income up to ₹12,00,000 for eligible resident individuals | Can reduce tax to nil where conditions are satisfied. |

| Salaried standard deduction | ₹75,000 under the new regime | Can make gross salary up to ₹12.75 lakh effectively tax-free in eligible cases. |

| Old regime relevance | Still useful where deductions and exemptions are high | HRA, 80C, 80D, home loan interest and other claims may change the final comparison. |

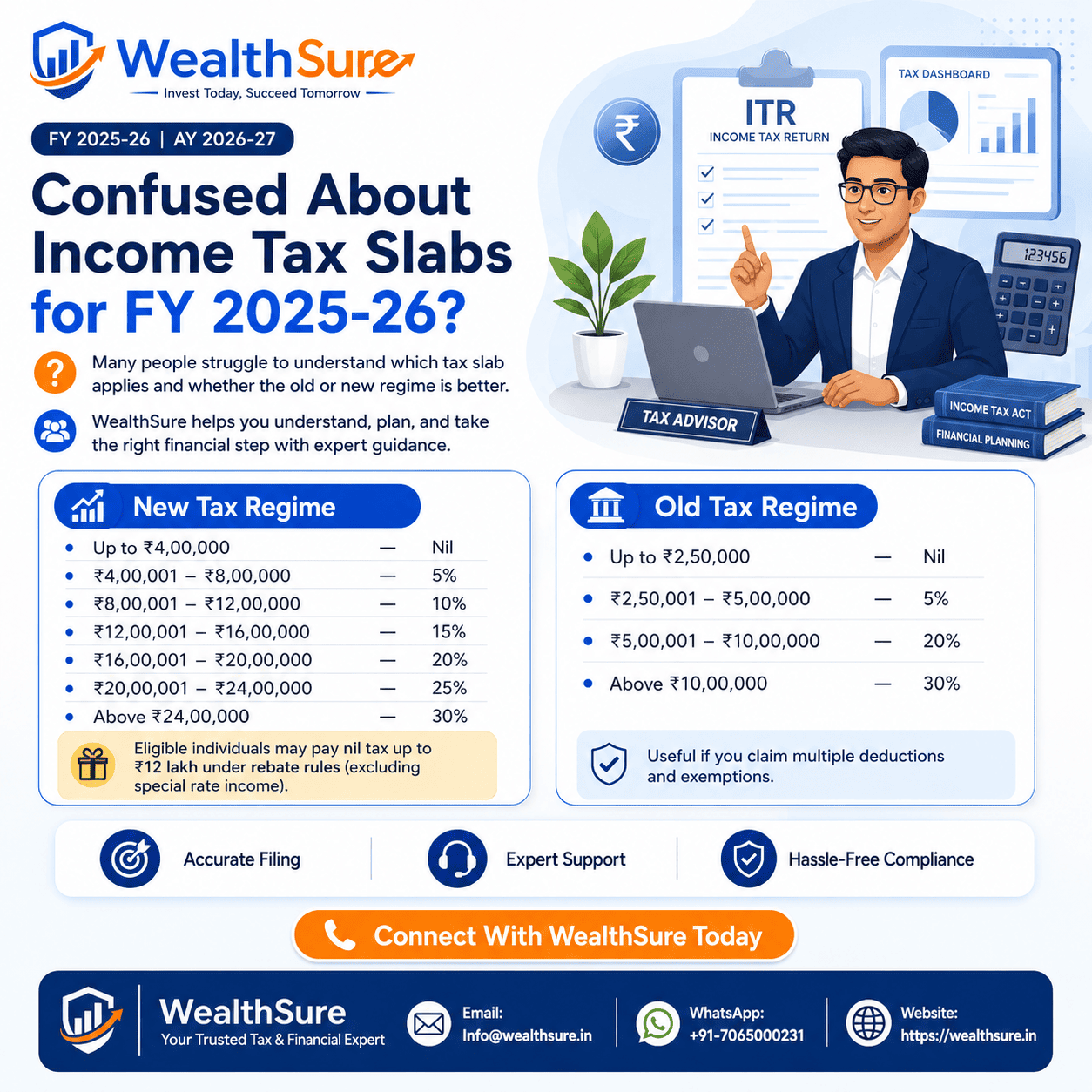

New Tax Regime Slabs for FY 2025-26

The new tax regime is designed to offer lower rates across wider income bands, while allowing fewer deductions and exemptions compared with the old regime. For FY 2025-26, the new regime slabs are easier to read because they move in ₹4 lakh bands up to ₹24 lakh, followed by the 30% slab above ₹24 lakh.

New Tax Regime at a Glance

FY 2025-26 • AY 2026-27| Taxable Income Under New Regime | Income Tax Rate | Practical Meaning |

|---|---|---|

| Up to ₹4,00,000 | Nil | No tax on this first income layer. |

| ₹4,00,001 to ₹8,00,000 | 5% | Only income above ₹4 lakh and up to ₹8 lakh is taxed at 5%. |

| ₹8,00,001 to ₹12,00,000 | 10% | This slab is important for many taxpayers near the rebate threshold. |

| ₹12,00,001 to ₹16,00,000 | 15% | Applies to the portion above ₹12 lakh and up to ₹16 lakh. |

| ₹16,00,001 to ₹20,00,000 | 20% | Applies to the portion above ₹16 lakh and up to ₹20 lakh. |

| ₹20,00,001 to ₹24,00,000 | 25% | Applies to the portion above ₹20 lakh and up to ₹24 lakh. |

| Above ₹24,00,000 | 30% | Applies only to taxable income exceeding ₹24 lakh. |

Health and education cess at 4% applies on income tax plus surcharge, where applicable. Surcharge may also apply for high-income taxpayers. For most salaried taxpayers below ₹50 lakh total income, surcharge is not a concern, but cess should still be included wherever tax is payable.

Who may benefit from the new tax regime?

The new regime may be suitable if you have limited deductions, do not claim HRA, do not have a large home loan interest claim, or prefer a simplified tax structure. It may also be beneficial for many taxpayers whose taxable income falls within the rebate-friendly range.

- You want a simpler tax calculation with fewer deduction proofs.

- Your eligible deductions under the old regime are low or moderate.

- Your taxable income under the new regime is within the rebate threshold.

- You do not claim significant HRA or home loan interest benefit.

- You prefer flexible investing instead of locking money only for tax-saving purposes.

Not sure whether the new tax regime is best for you? WealthSure can compare both regimes using your salary, deductions, rent, insurance, investments, home loan and capital gains details.

Ask a WealthSure tax expertOld Tax Regime Slabs for FY 2025-26

The old tax regime continues to matter because it allows several deductions and exemptions that are either restricted or unavailable in the new regime. If you pay rent and claim HRA, invest under Section 80C, pay health insurance premium under Section 80D, contribute to NPS, pay interest on an education loan, or claim home loan interest, the old regime may still produce a lower tax liability.

Old tax regime slabs for individuals below 60 years

| Taxable Income Under Old Regime | Income Tax Rate | Practical Meaning |

|---|---|---|

| Up to ₹2,50,000 | Nil | No tax on the first ₹2.5 lakh. |

| ₹2,50,001 to ₹5,00,000 | 5% | Resident individuals may evaluate Section 87A rebate if taxable income does not exceed ₹5 lakh. |

| ₹5,00,001 to ₹10,00,000 | 20% | A major slab for salaried taxpayers using deductions to reduce taxable income. |

| Above ₹10,00,000 | 30% | Applies to income exceeding ₹10 lakh. |

Old tax regime slabs for senior citizens and super senior citizens

Under the old regime, senior citizens and super senior citizens receive a higher basic exemption limit. This can matter for pensioners, retired individuals, parents, rental-income taxpayers and people with bank interest income.

| Taxpayer Category | Nil Tax Slab Under Old Regime | Higher Slab Structure |

|---|---|---|

| Below 60 years | Up to ₹2,50,000 | 5%, 20% and 30% slabs apply progressively. |

| Senior citizen: 60 years or more but below 80 years | Up to ₹3,00,000 | 5% from ₹3 lakh to ₹5 lakh, 20% from ₹5 lakh to ₹10 lakh and 30% above ₹10 lakh. |

| Super senior citizen: 80 years or more | Up to ₹5,00,000 | 20% from ₹5 lakh to ₹10 lakh and 30% above ₹10 lakh. |

Common deductions that make the old regime relevant

The old regime is not automatically better because it has deductions. It becomes better only when your deductions and exemptions are large enough to overcome the lower slab rates and higher rebate available under the new regime.

- Section 80C deductions such as EPF, PPF, ELSS, life insurance premium, tuition fees and eligible home loan principal repayment.

- Section 80D deduction for health insurance premium and preventive health check-up, subject to limits.

- House Rent Allowance exemption, where eligible.

- Standard deduction for salaried taxpayers.

- Home loan interest deduction under Section 24(b), subject to conditions.

- Additional NPS deduction under Section 80CCD(1B), where applicable.

- Education loan interest deduction under Section 80E.

- Other eligible deductions such as 80G, 80TTA, 80TTB, 80DD, 80DDB or 80U, depending on facts.

Do not choose the old regime just because you have investments. Compare the final tax payable under both regimes. Sometimes the new regime still wins even when you have some deductions.

Section 87A Rebate and Zero-Tax Income Limit

Section 87A rebate is one of the most important parts of the FY 2025-26 tax discussion. Under the new regime, eligible resident individuals may receive a rebate up to the applicable limit if taxable income does not exceed the prescribed threshold. This is why many taxpayers hear that income up to ₹12 lakh can become tax-free under the new regime.

| Tax Regime | Rebate Limit | Taxable Income Condition | Who Should Pay Attention? |

|---|---|---|---|

| New tax regime | Up to ₹60,000 | Taxable income should not exceed ₹12,00,000, subject to conditions. | Salaried taxpayers, pensioners and individuals near the rebate threshold. |

| Old tax regime | Up to ₹12,500 | Taxable income should not exceed ₹5,00,000, subject to conditions. | Taxpayers using deductions to bring taxable income up to ₹5 lakh. |

Why salaried taxpayers often hear the ₹12.75 lakh figure

The ₹12.75 lakh figure is commonly discussed because salaried taxpayers may get a standard deduction of ₹75,000 under the new regime. If a salaried person has gross salary income of ₹12.75 lakh and the standard deduction reduces taxable income to ₹12 lakh, Section 87A rebate may bring tax to nil, subject to eligibility and the nature of income.

Simple example: salary income of ₹12.75 lakh under the new regime

Assume a salaried resident individual has gross salary income of ₹12,75,000 and no special-rate income. After a standard deduction of ₹75,000, taxable income becomes ₹12,00,000. Under the new regime slabs, tax before rebate can be reduced by Section 87A rebate, resulting in nil tax, subject to applicable conditions.

However, taxpayers should be careful if income includes capital gains, lottery winnings, virtual digital assets or other income taxed at special rates. Rebate treatment can differ depending on the nature of income and applicable law. When income is not purely salary or regular income, review the rules before assuming that the entire tax becomes nil.

Old vs New Tax Regime: How to Choose

The right regime is not a matter of opinion. It is a calculation. The new regime may look attractive because of lower rates and rebate, while the old regime may look attractive because of deductions. The correct decision requires comparing your final tax payable under both options after considering all income, deductions, exemptions, surcharge, cess and special-rate income.

New Regime May Suit You If

- You have limited deductions.

- You do not claim HRA.

- You prefer simple compliance.

- Your income falls within the rebate-friendly range.

- You want flexibility in choosing investments without tax-saving pressure.

Old Regime May Suit You If

- You claim HRA and pay significant rent.

- You fully use Section 80C.

- You pay health insurance premiums.

- You have home loan interest benefits.

- Your total deductions are large enough to offset the higher old-regime slab rates.

A practical decision-tree for FY 2025-26

- Calculate total income from salary, business, profession, rent, interest, dividends, capital gains and other sources.

- Separate regular income from special-rate income such as certain capital gains or virtual digital asset income.

- List all eligible old-regime deductions and exemptions with proof.

- Calculate tax under the new regime after available deductions and rebate.

- Calculate tax under the old regime after deductions, exemptions and rebate.

- Add health and education cess and surcharge, where applicable.

- Choose the regime with lower final tax liability, while also considering compliance comfort and documentation.

Get a regime comparison before filing. WealthSure can help you compare old vs new tax regime, review documents, calculate deductions and avoid wrong regime selection during ITR filing.

Explore WealthSure ITR filing servicesPractical Tax Examples for FY 2025-26

Examples help you understand how slab taxation works. These examples are simplified for educational purposes and do not cover every possible deduction, surcharge, special-rate income or exception. Actual tax calculation may differ depending on salary components, deductions, capital gains, employer contribution, residential status and other facts.

Example 1: Salaried taxpayer with ₹10 lakh gross salary

Under the new regime, a salaried taxpayer may reduce salary income by the available standard deduction. If taxable income falls within the rebate threshold, the final tax may become nil, subject to conditions. Under the old regime, the result depends on HRA, Section 80C, Section 80D and other deductions. For many taxpayers at this income level, the new regime can be easier, but a comparison is still recommended.

Example 2: Salaried taxpayer with ₹15 lakh salary and low deductions

If deductions are low, the new regime may often be attractive because slab rates are lower across wider bands. The taxpayer should still verify whether employer NPS contribution, home loan interest, capital gains or special income changes the calculation.

Example 3: Salaried taxpayer with ₹18 lakh salary, HRA, 80C, 80D and home loan

Here, the old regime may become competitive if HRA exemption, Section 80C, Section 80D and home loan interest significantly reduce taxable income. This is why high-deduction taxpayers should not blindly accept the default new regime without comparison.

Example 4: Freelancer with professional income

A freelancer must first determine net taxable income after eligible expenses or presumptive taxation, where applicable. The regime decision should consider business income, professional expenses, deductions, advance tax, TDS and whether the taxpayer has opted in or out of a regime in earlier years.

Surcharge and Cess Explained

Income tax slabs do not tell the full story for high-income taxpayers. Once slab tax is calculated, surcharge may apply if income crosses specified thresholds. Health and education cess at 4% is then applied on the amount of income tax plus surcharge, where applicable.

| Total Income Range | Surcharge Under New Regime | Surcharge Under Old Regime |

|---|---|---|

| Up to ₹50 lakh | Nil | Nil |

| Above ₹50 lakh to ₹1 crore | 10% | 10% |

| Above ₹1 crore to ₹2 crore | 15% | 15% |

| Above ₹2 crore to ₹5 crore | 25% | 25% |

| Above ₹5 crore | 25% | 37% |

High-income taxpayers should also consider marginal relief, surcharge caps for certain types of income, capital gains, dividend taxation and advance tax implications. For this category, tax planning should ideally happen before the financial year ends, not only during return filing season.

Guidance for Different Taxpayer Profiles

For salaried individuals

Salaried taxpayers should not look only at gross salary. Review salary structure, standard deduction, HRA, employer NPS, reimbursements, perquisites, bonus, previous employer income, interest income and capital gains. If your employer has deducted TDS under one regime, you may still need to evaluate the final choice while filing ITR, subject to applicable rules.

For freelancers and consultants

Freelancers and consultants should calculate professional income carefully. TDS deducted by clients does not mean tax is fully paid. You may need to account for professional expenses, GST records, bank receipts, invoices, advance tax and presumptive taxation eligibility.

For investors with capital gains

If you sold shares, mutual funds, property, bonds, ESOPs or virtual digital assets, your final tax may include special-rate income. Do not assume that slab rebate covers every tax component. Capital gains require correct classification, holding period review, cost calculation and reporting.

For NRIs

NRIs should evaluate residential status first. Indian income such as salary received in India, rent from Indian property, capital gains from Indian assets, interest income or business income may be taxable in India depending on facts. DTAA relief, TDS and correct ITR reporting may require expert support.

For senior citizens

Senior citizens should compare regimes after considering pension, bank interest, medical insurance, Section 80TTB, rental income and capital gains. The old regime offers higher basic exemption limits for senior and super senior citizens, but the new regime may still be useful in some cases because of revised slab bands.

For business owners

Business owners should not make a regime decision casually. If you have business or professional income, opting out of the default regime may involve specific forms and timelines. The decision should consider depreciation, business deductions, presumptive taxation, advance tax, GST records and books of account.

Common Mistakes to Avoid While Using Income Tax Slabs

Many taxpayers know the slab rates but still make errors while estimating tax. These mistakes can lead to excess TDS, wrong tax planning, refund delays, interest liability or incorrect ITR filing.

- Assuming the highest slab rate applies to the entire income instead of only the income portion in that slab.

- Ignoring the difference between gross income and taxable income.

- Forgetting to add savings interest, fixed deposit interest, dividends, rent or capital gains.

- Assuming the new regime is always better because it is the default regime.

- Assuming the old regime is always better because deductions are available.

- Not checking whether Section 87A rebate applies to the specific income mix.

- Ignoring health and education cess while estimating final tax.

- Not considering surcharge for income above ₹50 lakh.

- Choosing investments only for deduction without checking liquidity, risk and goals.

- Waiting until ITR filing season to do tax planning that should have been done during the year.

Tax-Planning Checklist Before Filing ITR for FY 2025-26

Use this checklist before filing your income tax return for AY 2026-27. It can help you avoid wrong regime selection and incomplete income reporting.

| Checklist Item | Why It Matters | Recommended Action |

|---|---|---|

| Calculate total income from all sources | Tax slabs apply to taxable income, not only salary. | Include salary, interest, rent, capital gains, freelance income and other income. |

| Compare old and new tax regimes | Wrong regime selection can increase tax liability. | Calculate final tax under both regimes before filing. |

| Check deduction proofs | Unsupported deductions can create future issues. | Keep investment, insurance, rent, loan and donation proofs ready. |

| Review capital gains | Special-rate income can affect tax and rebate treatment. | Use broker, mutual fund and property transaction records carefully. |

| Check TDS and advance tax | Mismatch can cause demand or refund delay. | Review tax credit information and challans before filing. |

| Validate bank account | Refund can be delayed if bank details are incorrect. | Ensure the correct bank account is pre-validated on the portal. |

| Complete e-verification | Return filing is incomplete without verification. | E-verify within the permitted timeline after submitting the return. |

Plan taxes before filing, not after mistakes happen. WealthSure provides expert-assisted ITR filing, regime comparison, tax planning, capital gains reporting, freelancer filing, NRI tax support and notice-response assistance.

Get started with WealthSureHow WealthSure Helps with FY 2025-26 Tax Planning

At WealthSure, we do not just help users file income tax returns. We help them understand the financial decision behind tax filing. A correct slab calculation is only one part of the process. The larger goal is to file accurately, avoid mismatches, choose the right regime, plan investments sensibly and build a cleaner financial record.

WealthSure can assist with old vs new tax regime comparison, income tax filing for salaried individuals, freelancer and professional ITR filing, capital gains reporting, NRI tax filing, advance tax calculation, revised return guidance, updated return support and tax notice response.

FAQs on Income Tax Slabs for FY 2025-26

1. What are the income tax slabs for FY 2025-26 under the new tax regime?

Under the new tax regime for FY 2025-26, income up to ₹4 lakh is taxed at nil rate, ₹4 lakh to ₹8 lakh at 5%, ₹8 lakh to ₹12 lakh at 10%, ₹12 lakh to ₹16 lakh at 15%, ₹16 lakh to ₹20 lakh at 20%, ₹20 lakh to ₹24 lakh at 25% and income above ₹24 lakh at 30%, subject to cess, surcharge and applicable rules.

2. What is the old tax regime slab for individuals below 60 years?

Under the old tax regime for individuals below 60 years, income up to ₹2.5 lakh is nil, ₹2.5 lakh to ₹5 lakh is taxed at 5%, ₹5 lakh to ₹10 lakh at 20% and income above ₹10 lakh at 30%, subject to rebate, cess, surcharge and applicable rules.

3. Is the new tax regime the default regime for FY 2025-26?

Yes. The new tax regime is the default regime for eligible taxpayers. If you want to use the old regime, you must opt for it as per the applicable rules and timelines.

4. Can salaried taxpayers pay zero tax up to ₹12.75 lakh?

Eligible salaried taxpayers may have nil tax up to ₹12.75 lakh under the new regime because the ₹75,000 standard deduction can reduce taxable income to ₹12 lakh, where Section 87A rebate may apply. This depends on eligibility and the nature of income.

5. Does Section 87A rebate apply to everyone?

No. Section 87A rebate is generally available to eligible resident individuals subject to income limits and other conditions. It may not apply in the same way to certain special-rate incomes. Taxpayers with capital gains or other special income should check carefully.

6. Which regime is better for FY 2025-26?

The better regime depends on your income and deductions. The new regime may be better for taxpayers with limited deductions, while the old regime may be better for taxpayers with high HRA, 80C, 80D, home loan interest and other eligible claims.

7. Are senior citizens taxed differently?

Under the old regime, senior citizens and super senior citizens get higher basic exemption limits. Senior citizens should compare both regimes after considering pension, interest income, medical insurance, 80TTB, rent and capital gains.

8. Is cess included in the slab rates?

No. Slab rates show basic income tax rates. Health and education cess at 4% is applied separately on income tax plus surcharge, if any.

9. When does surcharge apply?

Surcharge generally applies when total income exceeds ₹50 lakh. The rate increases at higher income levels. High-income taxpayers should calculate surcharge and marginal relief carefully.

10. Do freelancers follow the same slab rates?

Individual freelancers generally use the same individual slab system, but they must first calculate business or professional income correctly. They should also consider expenses, presumptive taxation, TDS, advance tax and regime-switching rules.

11. Should I choose investments only to save tax under the old regime?

No. Tax saving should support your financial goals. Do not buy insurance, ELSS, NPS, PPF or other products only for deduction without checking risk, lock-in, liquidity, return expectation and long-term suitability.

12. Can WealthSure help me compare old and new tax regimes?

Yes. WealthSure can help compare both regimes, review deductions, calculate tax liability, check capital gains, guide ITR filing and support tax planning based on your actual income profile.

Conclusion

The income tax slabs for FY 2025-26 make the new tax regime highly relevant for many Indian taxpayers, especially those with simpler income and limited deductions. The revised slab bands, higher rebate threshold and standard deduction benefit can significantly reduce tax for eligible individuals. However, the old regime still deserves attention if you have substantial deductions such as HRA, Section 80C, Section 80D, NPS, home loan interest or other eligible claims.

The smartest approach is simple: do not guess. Calculate both regimes, include all income sources, check deductions with proof, consider capital gains and special-rate income, add cess and surcharge where applicable, and then choose the regime that gives the correct and most beneficial result. A tax slab is only the starting point. Good tax planning connects your income, compliance, investments and long-term financial goals.

File and plan with confidence. WealthSure helps individuals, professionals, freelancers, investors, NRIs and business owners simplify tax filing, tax planning and financial decision-making with expert support and fintech-powered tools.

Talk to a WealthSure expertDisclaimer

This article is for general informational and educational purposes only. It does not constitute tax, legal, investment, financial or professional advice. Income tax laws, slabs, deductions, exemptions, rebate rules, surcharge, cess, forms, due dates and portal processes may change. Please verify the latest information on the official Income Tax Department website or consult a qualified tax professional before filing your return or making tax decisions.